Pedestrian Accidents and UM/UIM Coverage in Texas

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- Texas UM/UIM coverage follows you as a person, so it can pay even when you were on foot.

- UM covers uninsured or hit-and-run drivers; UIM fills the gap when liability limits are too low.

- Texas gives most injury victims two years under CPRC § 16.003 to file the underlying tort claim.

You were crossing Greenville Avenue near Lower Greenville one evening when a driver ran the light and clipped you in the crosswalk. The car kept going. Now you’re dealing with hospital bills, missed shifts at work, and a police report that lists the driver as unknown. Can your own auto insurance help when you weren’t even in a car?

Your Auto Policy Covers You on Foot

In Texas, uninsured and underinsured motorist (UM/UIM) coverage follows you as a person, not as a passenger in a car. If you have UM/UIM on your own auto policy, it can pay for your injuries if you’re struck while walking. Pedestrian status does not disqualify you from filing a claim.

That surprises most people. The protection sits inside your auto policy, but it travels with you on the sidewalk, in a crosswalk, or anywhere a driver hits you. Resident household members on the same policy get the same benefit.

Under Texas Insurance Code § 1952.101, auto insurers must include UM/UIM coverage in every automobile liability policy issued in Texas. The only way to remove it is a signed written rejection by the named insured. Most Texas drivers carry at least some UM/UIM without realizing how far the coverage reaches. The Texas Department of Insurance overview of uninsured motorist coverage explains the basics in plain terms.

If you don’t own a car yourself, you may still be covered through a spouse, parent, or other resident household member’s policy. Texas uninsured driver rates have hovered around 14 percent in recent years, according to Insurance Research Council data, meaning roughly one in seven drivers on Texas roads may lack coverage. That makes this coverage important for anyone who walks near traffic, not just drivers.

UM vs. UIM: Which Coverage Applies to Your Claim?

UM and UIM sound similar but have key differences. UM responds when the at-fault driver had no insurance or was never identified. UIM responds when the driver has insurance, but the limits are too low to cover your damages. Knowing which one applies controls how your claim is built and when payment becomes available.

Uninsured Motorist Coverage

UM coverage steps in when the driver who hit you carried no liability insurance, had a lapsed policy, or fled the scene unidentified. Your own insurer essentially stands in the at-fault driver’s shoes for damages.

Texas Insurance Code § 1952.102 defines what counts as an uninsured motor vehicle for coverage purposes. For hit-and-run pedestrian crashes, most policies require a police report filed promptly. Without that report, the insurer can deny the claim.

You still have to prove the driver was negligent, even when no one knows who the driver was. Physical evidence, witnesses, and traffic camera footage become central.

Underinsured Motorist Coverage

UIM kicks in after the at-fault driver’s liability policy is exhausted. It fills the gap between those limits and your actual damages, up to your own UIM limit. You have to use up the driver’s coverage first before UIM becomes available.

Timing matters here. The Texas Supreme Court’s Brainard decision held that UIM benefits don’t become legally due until a judgment establishes the at-fault driver’s liability and underinsured status. That changes how and when you can collect.

Texas Insurance Code § 1952.104 governs what conditions you must satisfy before the insurer is obligated to pay. Read your policy carefully or have a lawyer read it for you.

Steps to File a Pedestrian UM/UIM Claim in Texas

The process moves on two tracks at once: the claim against the at-fault driver and the claim against your own insurer. Both have notice requirements, documentation demands, and timing rules. Missing a step on either track can shrink or kill your recovery. The earlier you start, the more options you have.

Call the police from the scene and get the incident report number. For hit-and-run pedestrian crashes, this report is usually required before UM coverage will activate.

Get medical care quickly, even if you feel mostly okay. Insurers use treatment gaps to argue your injuries weren’t really caused by the crash. Keep every record, every bill, and every prescription.

Notify your own insurer in writing as soon as you can. Texas UM/UIM policies impose prompt-notice requirements. Late notice can give the insurer a clean defense to coverage, even if your claim is otherwise valid.

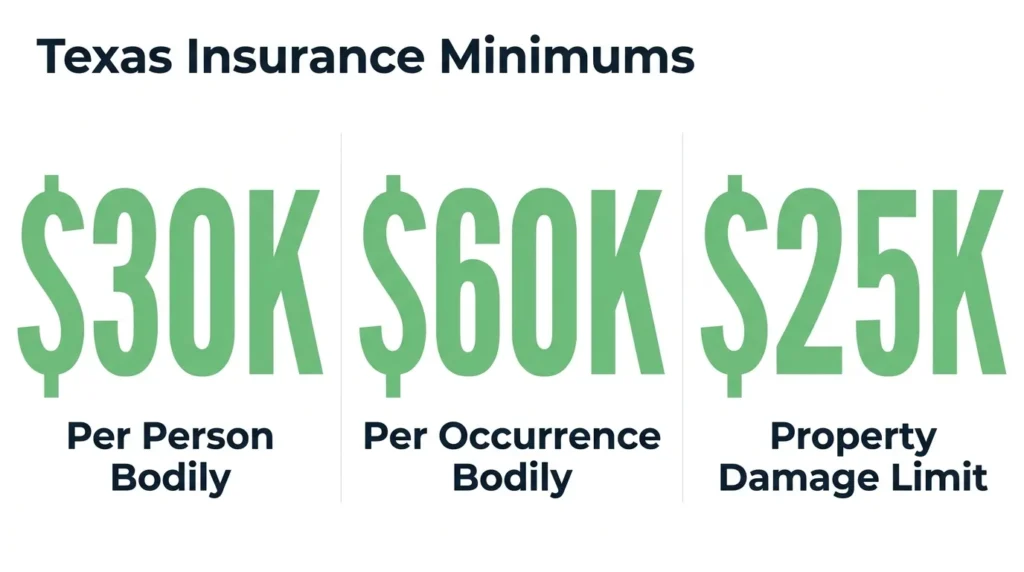

Find out what insurance the at-fault driver carried. Texas Transportation Code § 601.072 sets minimum financial responsibility limits at $30,000 per person and $60,000 per occurrence for bodily injury, plus $25,000 for property damage. Those minimums explain why even an insured driver can leave a seriously injured pedestrian undercompensated.

Document everything. Photos of injuries, the scene, your shoes, and the damaged car if it stayed at the scene. Also hold onto pay stubs and employer letters for lost wages, and receipts for out-of-pocket costs. The UM/UIM claim gets evaluated against the same damages framework as a regular injury claim.

Insurer notice rules and the UIM exhaustion sequence are where claims often fall apart without help.

Deadlines & Limits That Can Cut Off Your Recovery

Two clocks run at once after a pedestrian crash. The tort clock controls your claim against the at-fault driver. The contract clock controls your claim against your own insurer. Missing either can end the case. Most people don’t realize they’re tracking separate deadlines.

The underlying personal injury claim against the at-fault driver must generally be filed within two years under the Texas Civil Practice and Remedies Code (CPRC) § 16.003. The clock runs from the date of the crash.

The UM/UIM contract claim against your own insurer is governed by your policy’s limitations provision and Texas insurance law. That period can differ from the two-year tort deadline, and Texas courts have not settled every question about how the two interact.

Preserving the tort claim against an identified driver protects your UIM position, since your UIM insurer can contest both liability and damages. If your tort claim against the driver expires, the insurer can still raise those defenses without the same evidentiary backstop you would have had in the underlying suit.

For unidentified hit-and-run drivers, no third-party suit is possible. The UM limitations period in your policy controls, and prompt notice is the main protective step.

Personal Injury Protection (PIP) coverage, which Texas insurers must offer alongside UM/UIM, pays medical expenses and a portion of lost wages without regard to fault. It pays out faster than UM/UIM and does not offset it.

Understanding this process and reviewing injured pedestrian claim deadlines in Texas helps avoid issues.

Talk to a Texas Pedestrian Injury Attorney

Pedestrian crashes with uninsured or underinsured drivers create layered claims that move on tight timelines. Angel Reyes & Associates has decades of experience handling pedestrian accident and UM/UIM claims across Texas, with more than $1 billion recovered for clients.

You can review our verdicts and settlements to see the range of cases we’ve handled. We work on contingency, so there’s no fee unless we win, and consultations are free. Reach out to us today to talk through your options.

Past results do not guarantee future outcomes.

Pedestrian Accident/UM/UIM Coverage FAQs

Can my UM/UIM coverage pay for pain and suffering after a pedestrian accident, or only medical bills?

Texas UM/UIM coverage can compensate for the full range of damages a negligent driver would owe you, including pain and suffering, not just medical expenses. The damages recoverable mirror what you could claim in a tort lawsuit against the at-fault driver.

What happens to my UM/UIM claim if I was partly at fault for the pedestrian accident?

Texas follows a modified comparative fault rule, which means your recovery is reduced by your percentage of fault, and you cannot recover at all if you are found more than 50 percent responsible. Your UM/UIM insurer can raise your comparative fault as a defense when evaluating the claim.

Does Texas require insurers to offer stacked UM/UIM coverage if I have more than one vehicle on my policy?

Texas does not mandate stacking, and most standard Texas auto policies include anti-stacking language that limits recovery to the highest single-vehicle limit, even if multiple vehicles are insured under the same policy. Reviewing your policy’s stacking provisions before a loss occurs can reveal gaps worth addressing.

Will filing a UM/UIM claim raise my auto insurance rates in Texas?

Texas law does not prohibit insurers from considering a UM/UIM claim when setting future premiums, and some insurers do factor such claims into renewal pricing. Checking your insurer’s surcharge schedule before filing can help you understand the potential cost.

Can a Texas pedestrian pursue both a UM/UIM claim and a separate lawsuit against the at-fault driver at the same time?

Yes, you can pursue both simultaneously, but you cannot collect more than your total proven damages across both. Most Texas UM/UIM policies also give your insurer a right of subrogation, meaning the insurer may seek reimbursement from any recovery you obtain against the at-fault driver.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 55,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...