UM/UIM Claims in Texas When the At-Fault Driver Dies

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- The death of an at-fault driver does not eliminate your right to pursue compensation through their insurance, their estate, or your own UM/UIM coverage.

- Texas has a two-year statute of limitations for most injury claims, but UM/UIM policies may have separate notice requirements that apply earlier.

- Whether UM/UIM limits can be "stacked" across multiple policies depends on specific policy language, not general assumptions.

You were driving home on I-10 in San Antonio when another vehicle struck your car. You later learned the other driver died at the scene. Now you’re dealing with injuries, medical bills, and a question that feels impossible to answer: how do you pursue compensation when the person responsible for the accident is gone?

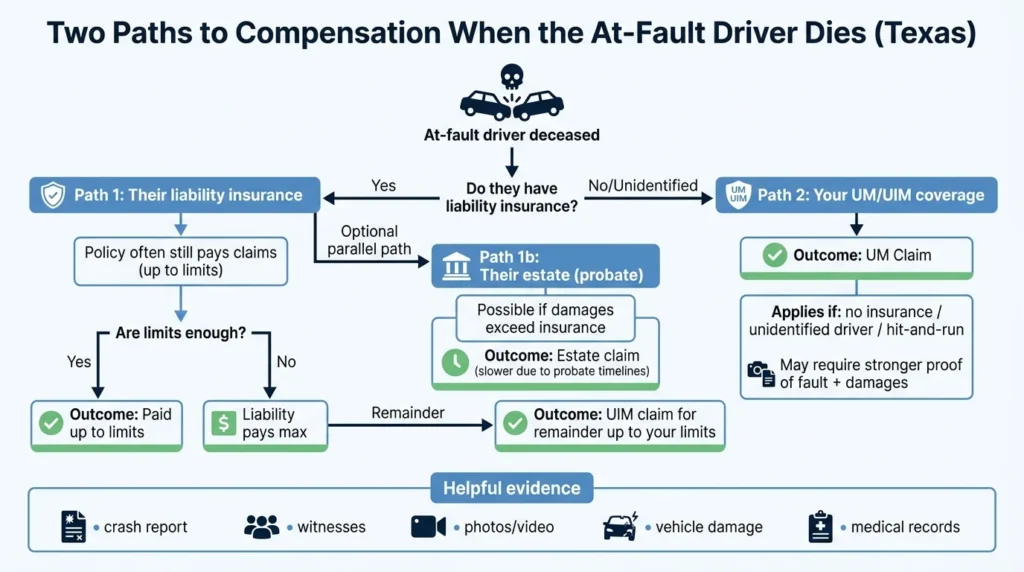

The death of an at-fault driver does not end your right to recover damages. Texas law provides pathways for crash victims in this situation. Your own uninsured or underinsured motorist coverage may become your primary source of compensation.

Can You Still Get Compensation if the At-Fault Driver Died?

A fatality does not automatically close a valid injury claim. If the at-fault driver dies, they are still liable for the damage that they cause, and you can still pursue recovery from them.

Two main recovery paths exist in Texas: pursuing the deceased driver through their liability insurance or their estate, and filing a claim under your own UM/UIM coverage.

Pursuing the Deceased Driver’s Estate

If the other driver lacked adequate liability to cover the damages they caused, you may be able to pursue their estate for the remainder of what you are owed.

Estate claims may have more resources available, but they will almost always take more time. The driver’s assets and insurance payouts may be handled through probate. The probate process allows any entity which may have a claim to some of the deceased’s assets to lodge this claim before their assets are distributed to their next of kin.

If you’re facing mounting financial pressure and a growing pile of bills, waiting months for the probate process to finish may not be ideal. If this is the case, you may still be able to pursue compensation by filing a claim with your own uninsured motorist coverage.

Pursuing a UM/UIM Claim

The deceased driver’s auto insurance policy typically remains in effect, and their insurer can still pay claims up to policy limits. If the driver had assets, their estate may also be a potential source of recovery.

Your own UM/UIM coverage becomes the primary path when:

- The at-fault driver had no liability insurance

- The driver cannot be identified (such as in hit-and-run scenarios)

- The driver’s liability limits are too low compared to your damages

When the other driver cannot give a statement or participate in the investigation, your insurer may require stronger proof of fault and damages. The police crash report, witness statements, and physical evidence become more important. Scene photographs, vehicle damage documentation, and surveillance footage can help establish what happened.

Coordination between a liability carrier and your own UM/UIM insurer may be necessary. If the deceased driver’s estate enters probate, communications and negotiations can slow down. An attorney familiar with car accidents can help navigate these complications.

Examples of Fatal-At-Fault Scenarios

Scenario 1: The at-fault driver dies and had no insurance. Your UM bodily injury coverage may apply. If you have UM property damage coverage, it may help with vehicle repairs (though it may be subject to a deductible under Texas law).

Scenario 2: The at-fault driver dies and carried only minimum liability limits ($30,000 per person). After the liability claim pays its maximum, your UIM coverage may cover the remaining damages up to your policy limits.

Scenario 3: Fault is disputed because there are no eyewitnesses. Your UM/UIM claim may depend on crash reconstruction analysis, the police report, and medical documentation linking your injuries to the collision.

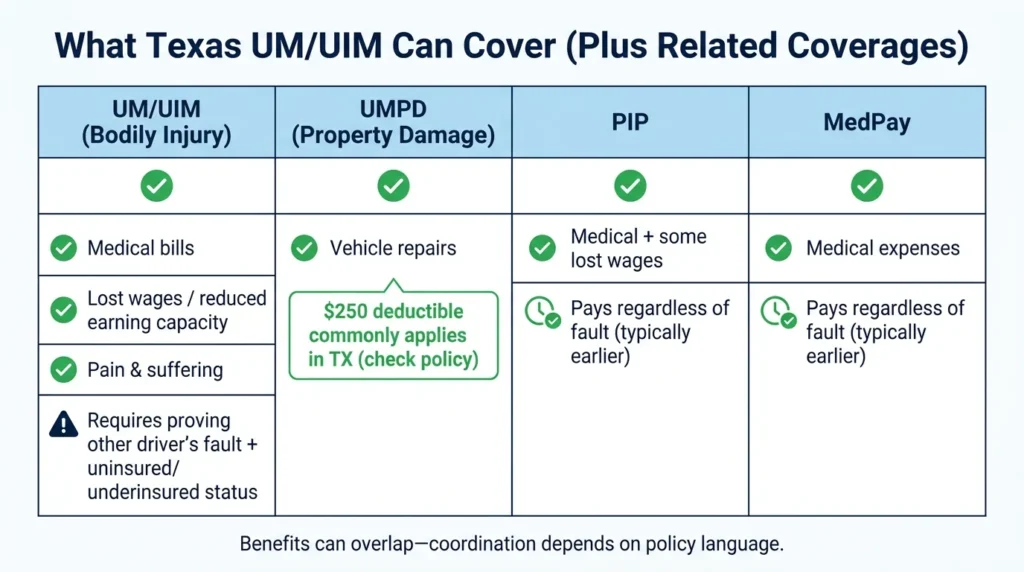

What UM/UIM Can Pay for in Texas

UM/UIM coverage can compensate for losses similar to what you could recover in a liability claim against the at-fault driver. The Texas Department of Insurance explains that UM/UIM can help pay for medical bills and car repairs when the other driver lacks adequate coverage.

Other common covered losses include:

- Lost wages and reduced earning capacity

- Pain and suffering

- Vehicle repairs (under UMPD, subject to the $250 deductible)

If you also carry PIP or MedPay coverage, those benefits may pay earlier regardless of fault while your UM/UIM claim is being investigated. Understanding how these coverages coordinate helps you access funds when you need them.

Steps to Protect Your Texas UM/UIM Claim

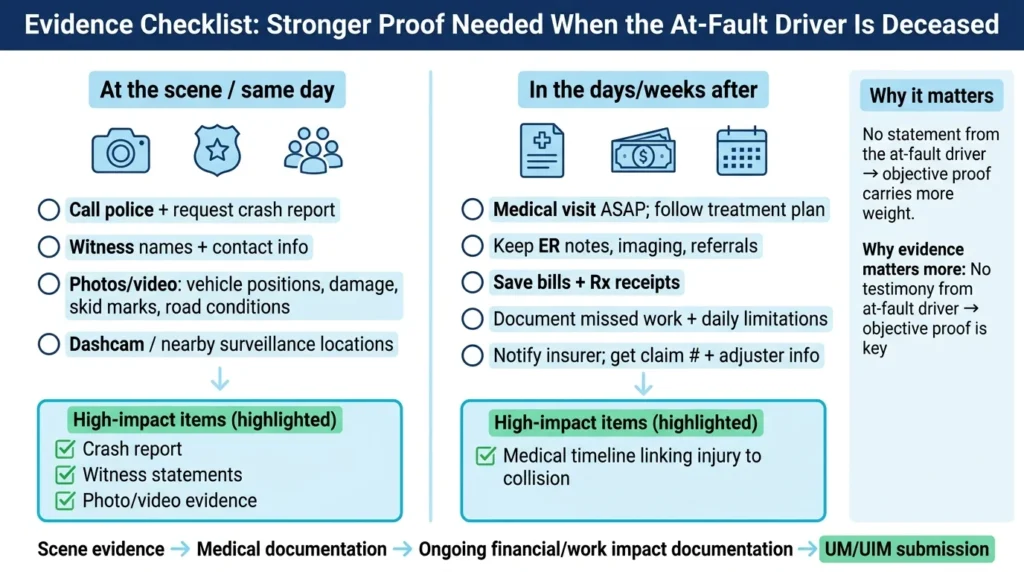

When the at-fault driver is deceased, preserving evidence and meeting policy requirements becomes even more critical. The Texas Department of Insurance auto guide emphasizes documenting everything and getting witness information before people leave the scene.

Here are some immediate actions you should take after an accident:

- Call the police and request a crash report

- Collect witness contact information

- Take photos of vehicle positions, damage, skid marks, and road conditions

- Seek medical care as soon as possible, even if symptoms seem minor

- Notify your insurer and ask what they require for a UM/UIM claim

- Get a claim number and adjuster contact details

- Keep medical records and follow recommended treatment

- Save bills and document missed work and how injuries affect your daily life

Evidence That Matters More When the At-Fault Driver Is Deceased

Without the other driver’s testimony, objective evidence carries more weight:

- Police crash report with officer observations and citations

- Scene photographs and video (including dashcam or nearby surveillance)

- Written witness statements

- Vehicle damage documentation showing impact severity

- Medical records establishing injury causation and treatment timeline

Your medical care timeline should show a clear connection between the crash and your injuries. Emergency room notes, imaging studies, specialist referrals, and consistent symptom reporting all support your claim.

UM/UIM Stacking in Texas

“Stacking” refers to combining UM/UIM limits across multiple vehicles or policies to increase available coverage. This is legal in some cases, but your own policy language will determine whether this is even an option in your situation.

Common Stacking Scenarios

- Separate policies in the household: If you and your spouse each have auto policies with UM/UIM coverage, you may be able to file a claim against both policies, depending on the nature of the incident.

- Multiple vehicles on one policy: Some policies allow stacking coverage across both vehicles, though this varies with policy language.

- Employer or commercial policies: If you were working at the time of the crash, some commercial policies allow stacking as well.

If you want to pursue stacking your UM/UIM policies for more available compensation, it’s important to collect additional evidence to support your claim. Insurers scrutinize these actions heavily, so it’s important to make sure story and evidence leave nothing up to doubt.

This includes:

- Declarations pages for all household auto policies showing UM/UIM limits

- Any umbrella policies or employer auto coverage

- Information about every potential “insured” (named insureds, resident relatives, permissive occupants)

A thorough review of your UM/UIM coverage options requires examining actual policy documents. It’s usually a good idea to have your attorney review them to see if this is an option in your specific situation.

When to Talk to a Texas Car Accident Lawyer

Certain situations signal that legal help may benefit your claim:

- The at-fault driver died, complicating evidence and negotiations

- You have serious injuries requiring ongoing treatment

- The fault is disputed or unclear

- Multiple insurance policies may apply (stacking questions)

- Your UM/UIM claim has been denied or undervalued

- The insurance company is delaying the investigation or payment

At Angel Reyes & Associates, we have helped Texas crash victims recover compensation for over 30 years. We have recovered more than $1 billion for our clients. We offer free consultations and work on a contingency basis, meaning no fee unless we win. We have more than 20 locations across Texas and handle cases across the state remotely.

If you were injured in a crash where the at-fault driver died, you still have options. Contact us to discuss your UM/UIM claim and learn how we can help protect your right to compensation.

UM/UIM Claim FAQs

Does Texas UM/UIM cover a hit-and-run if the other driver dies or is never identified?

It may, depending on your policy and the details of the crash. Strong documentation helps, including a police report, photos, witness information, and any available video footage.

Do I have to pay my UM/UIM deductible for injury claims in Texas?

Usually not for bodily injury claims. The deductible often applies to uninsured motorist property damage, which is commonly $250 in Texas. Check your policy to confirm.

Can a passenger make a UM/UIM claim after a Texas crash if the at-fault driver died?

In some cases, yes. Passengers may be covered under the vehicle’s policy or their own policy, depending on how coverage is defined.

Will my health insurance or PIP affect what I can recover under UM/UIM?

They may affect how bills are paid at first, but they do not automatically prevent a UM/UIM claim. Coverage can overlap depending on the situation.

What documents should I gather before asking whether UM/UIM stacking might apply in Texas?

Start with the declarations pages for every auto policy that may apply, including any employer-vehicle policies. It also helps to gather the full policy forms, the crash report, and basic information showing who lived in the household and who owned each vehicle.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 70,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...