Full Coverage Car Insurance in Texas: What It Actually Means

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- "Full coverage" is not a legal term—it's shorthand for liability plus collision and comprehensive coverage.

- Lenders require collision and comprehensive because they protect the financed vehicle, not just you.

- Check your declarations page for gaps in PIP and UM/UIM before assuming you're fully protected.

Full Coverage Car Insurance in Texas: What It Actually Means

You just financed a truck from a dealer in Arlington who mentioned you need “full coverage” insurance before driving off the lot. Texas law does not define “full coverage” as an official policy type. The term is industry shorthand for a combination of coverages that go beyond the state’s minimum liability requirements.

If you’re juggling the paperwork between the dealer and your insurer, this breakdown saves time and helps you understand exactly what you’re paying for.

What “Full Coverage” Usually Includes

Most Texas drivers and lenders use “full coverage” to describe a policy that bundles three main protections. Insurance terms can feel overwhelming when you’re trying to close a deal, but the core structure is straightforward.

Liability insurance pays for injuries and property damage you cause to others. Texas requires minimum limits of 30/60/25: $30,000 per person for bodily injury, $60,000 per accident for bodily injury, and $25,000 for property damage.

Collision coverage pays to repair or replace your vehicle after a crash, regardless of fault. If you hit a guardrail on I-35 or another driver rear-ends you in a parking lot, collision applies.

Comprehensive coverage handles non-collision damage. This includes hail storms, theft, flooding, vandalism, and hitting a deer on a rural highway.

Lenders and lease companies almost always require collision and comprehensive. They protect the vehicle securing your loan.

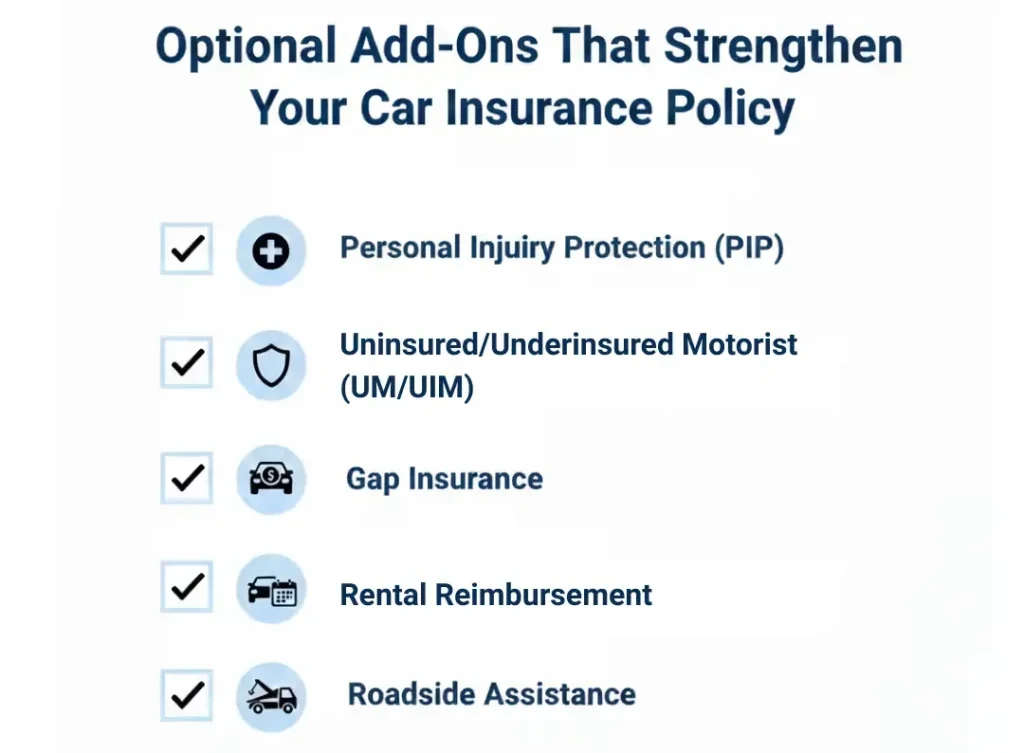

Optional Add-Ons That Strengthen Your Policy

Liability, collision, and comprehensive form the core. But several optional coverages can close gaps that matter after a serious crash.

Personal Injury Protection (PIP)

Texas insurers must offer PIP, and it applies regardless of who caused the accident. PIP covers medical expenses, lost wages, and certain other costs for you and your passengers. You can reject it in writing, but many Texans keep at least $2,500 in PIP for immediate medical bills.

For more on how PIP works alongside other protections, see UM, UIM, and PIP Insurance Coverage Explained.

Uninsured/Underinsured Motorist Coverage (UM/UIM)

UM coverage protects you if the at-fault driver has no insurance. UIM kicks in when their policy limits fall short of your actual damages.

Texas does not require UM/UIM, but you must reject it in writing if you do not want it. Given that a significant number of Texas drivers carry no insurance or only state minimums, UM/UIM can be critical after a serious wreck.

Learn why many attorneys recommend this coverage in Why You Need UM/UIM & PIP Insurance Coverage.

Protecting Your Finances if the Vehicle Is a Loss

Those coverages protect people. The next two protect your finances if the vehicle itself is totaled or temporarily unavailable.

Gap Insurance

If your vehicle is totaled and you owe more than its current value, gap insurance covers the difference. This is common with new cars that depreciate quickly or loans with low down payments.

Rental Reimbursement and Roadside Assistance

These add-ons cover a rental car while yours is being repaired and help with towing or lockouts. They are relatively inexpensive and can reduce stress after an accident.

When Full Coverage Makes Sense

Full coverage is not legally required in Texas. But several situations make it a practical choice.

Financed or leased vehicles. Your lender or lease company will almost certainly require collision and comprehensive. Failing to maintain coverage can trigger forced-place insurance at a much higher cost.

Newer or higher-value cars. If your vehicle would be expensive to repair or replace, collision and comprehensive protect your investment.

Limited savings for repairs. If paying out of pocket for a totaled car or major repairs would strain your budget, full coverage transfers that risk to your insurer.

High-risk commutes. Drivers who spend hours on congested highways like 635 in Dallas or the 610 Loop in Houston face more exposure to collisions and road debris.

For a broader look at factors that affect your policy decision, see Your Comprehensive Guide to Buying Car Insurance.

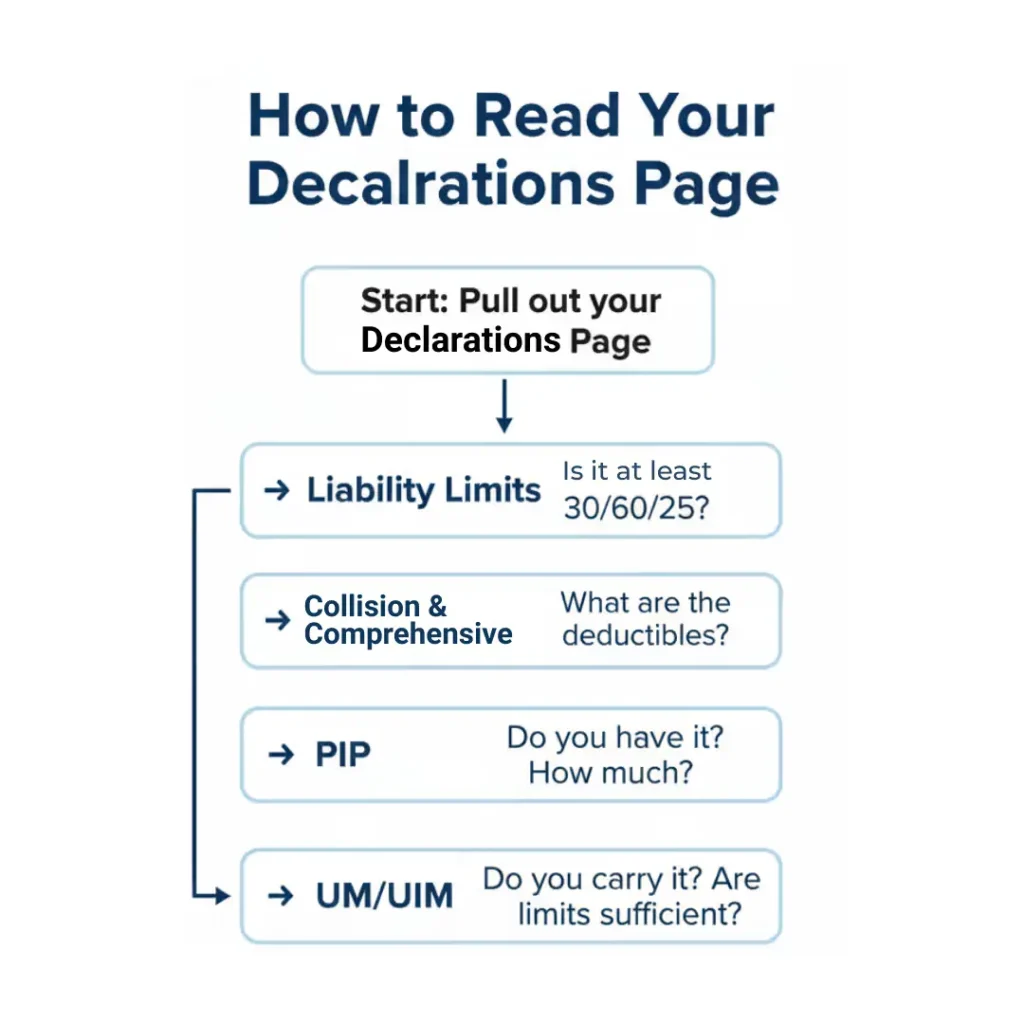

How to Evaluate Your Current Policy

Before shopping for new coverage, check what you already carry. You may have more protection than you realize—or gaps you didn’t know existed.

Pull out your declarations page. Look for these items:

- Liability limits. Are they at or above 30/60/25? Many drivers choose higher limits for better protection.

- Collision and comprehensive. Note your deductibles. A $500 deductible means lower out-of-pocket costs after a claim but higher premiums.

- PIP. Check whether you have it and at what amount.

- UM/UIM. Confirm whether you carry it and whether limits match your liability coverage.

If any section is missing or unclear, call your insurer and ask for a plain-language explanation.

If your claim becomes complicated or you face a coverage dispute, Angel Reyes & Associates has guided Texans through situations like this for over 30 years. Call us for a free consultation to review your options. Every case is different; past results do not guarantee future outcomes.

Full Coverage Insurance FAQs

Is full coverage required by Texas law?

Full coverage is not required by Texas law. The state only mandates liability insurance at the 30/60/25 minimums. “Full coverage” is a term used by consumers and lenders, not a legal requirement.

Will full coverage pay for my medical bills after a crash?

Full coverage will not pay for your medical bills directly. Collision and comprehensive cover vehicle damage, not medical expenses. PIP and health insurance handle medical bills. UM/UIM can help if the at-fault driver lacks adequate coverage.

How much does full coverage cost in Texas?

The cost of full coverage in Texas varies based on your driving record, vehicle, location, and chosen deductibles. Get quotes from multiple insurers and compare coverage limits, not just price.

Can I drop collision and comprehensive after I pay off my car?

You can drop collision and comprehensive after you pay off your car. Once you own the vehicle outright, the choice is yours. See “When Full Coverage Makes Sense” above for factors to weigh when deciding whether to keep or drop these coverages.

What should I do if I am in an accident and unsure about my coverage?

If you are in an accident and unsure about your coverage, start by gathering the police report, photos of damage, and the other driver’s insurance information. Review your policy or call your insurer.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 70,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...