What Happens When Multiple UM/UIM Policies Apply in Texas?

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- Texas allows inter-policy stacking but bars intra-policy stacking when anti-stacking clauses apply.

- Texas law lets each UIM insurer offset recoveries already paid by prior coverage layers.

- Settling with the at-fault driver without written consent can void your UM/UIM coverage entirely.

You were rear-ended on I-35 heading home from a late client meeting, and the driver who hit you carried only the state minimum liability limits. Your medical bills already exceed what their insurer will pay. Then you remember you’re also listed on your spouse’s auto policy, and the car you were driving belongs to your employer. Suddenly the question isn’t whether you have coverage. It’s how many policies you can actually use.

How Multiple UM/UIM Policies Arise in Texas

A single Texas crash victim can be named on several uninsured/underinsured motorist policies at once. Your own auto policy, a resident family member’s policy, the vehicle owner’s policy, and an employer-provided policy can each carry independent UM/UIM limits. Many drivers discover this only after an at-fault driver’s liability coverage falls short of their actual losses.

The Texas Insurance Code § 1952.101 requires every insurer to offer UM/UIM coverage on a personal auto policy. Unless a named insured on each policy rejected that coverage in writing, you likely carry it on every one.

Resident-relative clauses extend a named insured’s UM/UIM coverage to family members living in the same household. You don’t need to be a listed driver on the policy to access this coverage. A son living at home or a spouse who drives their own car may each tap the household’s policies.

The triggering condition is the same in every scenario. The at-fault driver either carried no insurance or carried limits below your total damages. Confirm that fact first, then map out every UM/UIM policy that names you, your household, or the vehicle you occupied. A starting point is our guide on what to do when an uninsured driver hits you.

Stacking vs Layering: What Texas Law Actually Allows

Texas treats two types of stacking very differently. Combining limits inside a single policy is generally barred. Claiming under two separate policies is generally allowed. Readers often blur these together, and the legal outcome depends on which one applies to your situation.

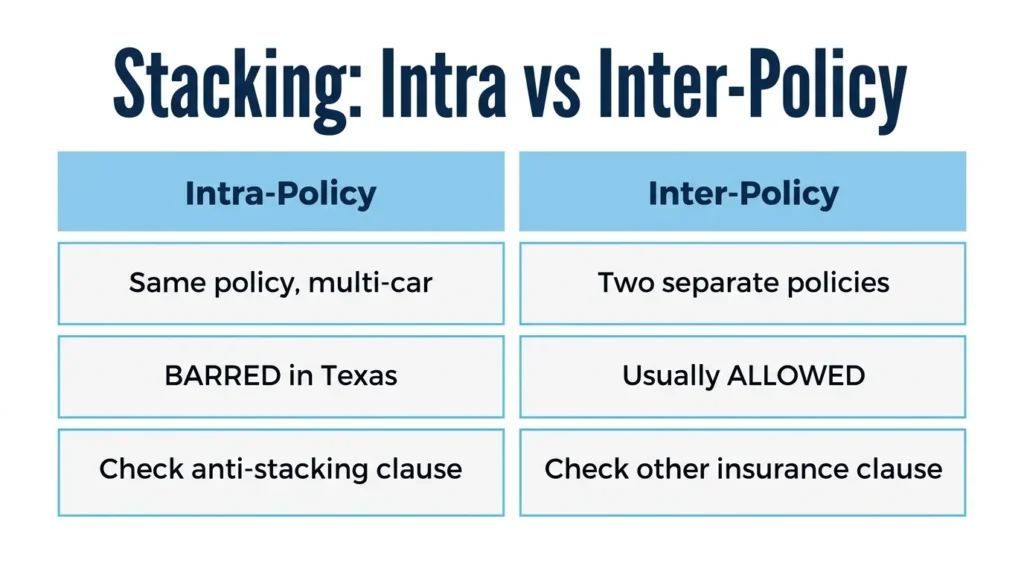

Intra-Policy Stacking

Intra-policy stacking means adding the UM/UIM limits of multiple vehicles insured under one policy. If you insure three cars on a single policy with $50,000 in UM/UIM limits per vehicle, you cannot combine those into a $150,000 recovery pool.

Texas courts enforce anti-stacking clauses written into auto policies. The insurer limits your recovery to the single highest applicable limit, not the sum of all per-vehicle limits. Case law has consistently upheld this approach when the policy language is clear.

The practical result is simple. Insuring more vehicles on the same policy does not multiply your UM/UIM protection.

Inter-Policy Stacking

Inter-policy stacking means recovering under two separate policies. Each policy is issued to a different named insured or on a different vehicle. Texas allows this unless the policy language expressly prohibits it.

Whether stacking actually works depends on the “other insurance” clause in each policy. Some clauses make a policy excess when another policy applies. Others bar contribution entirely. You need to read both policies before filing any claim.

Comparing this language is important because an insurer may try to deny primary responsibility by pointing to another policy that should pay first. Our breakdown of UM, UIM, and PIP coverage in Texas walks through how these layers interact in practice.

Which UM/UIM Policy Pays First?

When several policies apply, the order they pay in shapes your total recovery. The first-paying policy reduces what the second one owes through offset rules. Your own policy is generally primary, with a household member’s policy or a vehicle owner’s policy applying as excess, but the controlling language sits in each policy’s “other insurance” clause.

If you were driving your own car and you’re also a resident relative on a parent’s or spouse’s policy, your own coverage usually responds first. The family member’s policy then becomes a secondary or excess layer. Exact outcomes depend on what each policy says.

The picture flips when you’re driving someone else’s car. In an employer-provided or borrowed vehicle, the vehicle owner’s policy is often primary. Your personal policy may apply in excess on top of that. Readers in this scenario should review both policies before filing anything.

Sorting out which policy responds first in a multi-policy claim is one area where a review of your UM/UIM coverage options can pay off before you commit to a filing order.

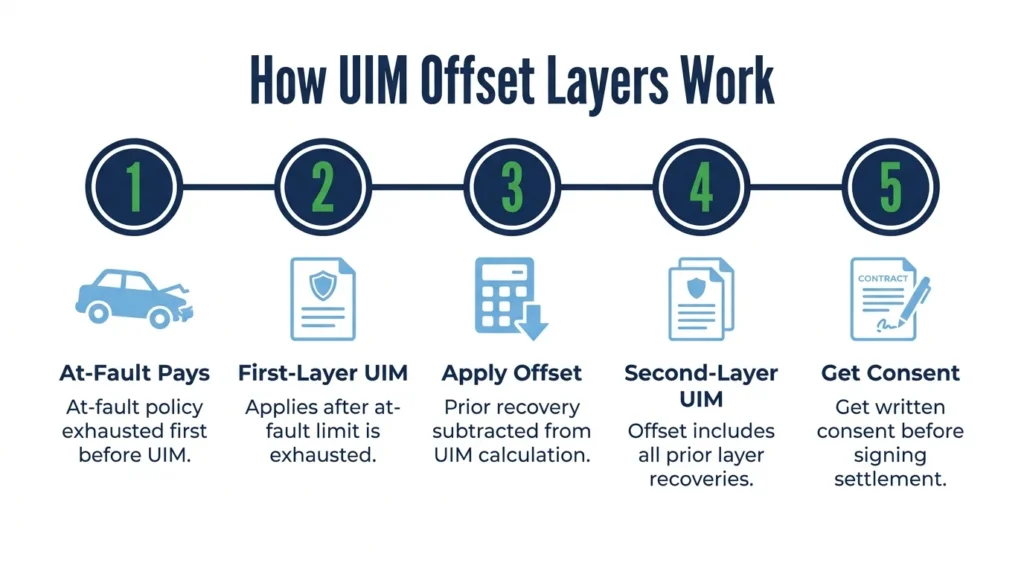

UIM Offsets & How Each Layer Is Reduced

Under Texas law, a UIM insurer subtracts the amount you already recovered from the at-fault driver’s liability carrier before calculating what it owes. That offset applies at every UIM layer, not just the first one. The mechanics are why a careful sequence is so important.

Take a simple example. The at-fault driver pays their $30,000 liability limit. Your first-layer UIM policy has a $100,000 limit, so it owes up to $70,000 after the offset. If a second-layer UIM policy then applies, it calculates its offset against the combined $100,000 you’ve already collected, not against zero.

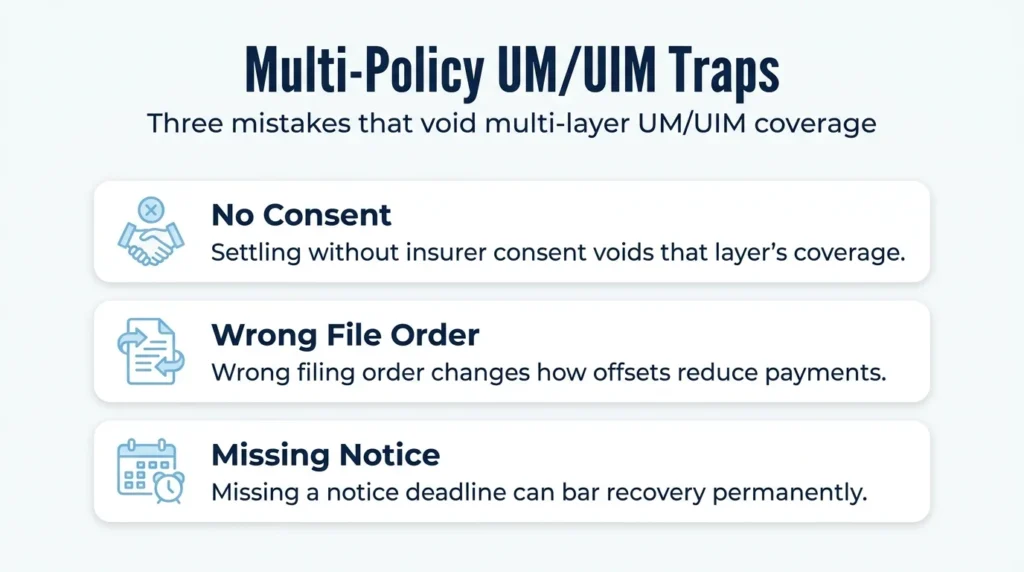

Insurers rarely volunteer information about secondary layers. If you settle with the at-fault driver’s carrier without preserving your rights under each UIM policy, you can lose access to those layers entirely.

Consent-to-settle clauses are the bigger trap. Most Texas UM/UIM policies require the insurer’s written consent before you accept a settlement from the at-fault driver. Settling without consent can void coverage under that policy. When a second-layer insurer is in play, you may need consent from two separate carriers before signing anything. The Texas Department of Insurance consumer guide on auto coverage explains the basic structure of these requirements.

Layered offsets are easier to map out before a settlement than after one. Our overview of going above the minimums with UM/UIM and PIP explains why higher limits at each layer matter so much.

Get Help Recovering Under Every Available Policy

You may have access to more coverage than any single insurer has been willing to disclose. Angel Reyes & Associates handles complex UM/UIM claims involving multiple policy layers across Texas, and our team can identify and activate every policy that names you, your household, or the vehicle you were in.

We work on contingency, meaning no fee unless we win, and we have more than $1 billion recovered for clients. You can review our verdicts and settlements or contact us today to discuss your coverage layers.

Past results do not guarantee future outcomes.

Frequently Asked Questions

Can an insurer deny my UM/UIM claim if I waited too long to file it?

Yes. Texas UM/UIM policies include a statute of limitations, and most courts apply a four-year deadline for contract claims, though some policies set shorter notice deadlines that can cut off your right to claim even sooner. Missing either deadline can bar recovery under that policy entirely.

What happens to my UM/UIM claim if the at-fault driver had insurance but their policy was later voided or rescinded?

If the at-fault driver’s insurer rescinds the policy after your crash, that driver may be treated as uninsured for purposes of your UM claim. Texas courts have addressed this scenario, and the outcome depends on whether the rescission was valid and whether your insurer received proper notice.

Does a UM/UIM policy cover my passengers, or only me as the driver?

Passengers in your vehicle may be covered under your UM/UIM policy if they are resident relatives, but non-household passengers typically need to look to their own auto policies for UM/UIM protection. Coverage for passengers depends on each policy’s definitions of “covered person” and the specific facts of who was in the vehicle.

Can I make a UM claim even if the other driver fled and was never identified?

Texas UM policies do cover hit-and-run crashes, but most require some physical contact between the vehicles as proof that another car was actually involved. Without physical contact, an unwitnessed hit-and-run claim is generally not covered under standard Texas UM policy language.

If I reject UM/UIM coverage on my own policy, can I still access it through a household family member's policy?

Yes. Rejecting UM/UIM on your own policy removes it from that policy only. If a resident family member’s policy includes a resident-relative provision and that coverage was not rejected on their policy, you may still qualify as a covered person under theirs.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 70,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...