Top Reasons Insurance Companies Underpay Injury Claims in Texas

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- Insurers often start with low offers that overlook future care, lost wages, and pain and suffering because they pay based on proof and pressure.

- Texas comparative fault rules and the two-year lawsuit deadline can reduce leverage, so delays and blame shifting are pressure tactics that work in their favor.

- Strong documentation and a detailed demand package can increase your settlement, and legal help may be needed if underpayment continues.

Top Reasons Insurance Companies Underpay Injury Claims in Texas

You just opened a settlement offer after weeks of waiting, and the number barely covers your ER visit. This can be one of the most disheartening and frustrating moments of an injury claim, especially when medical bills keep arriving and you keep missing shifts at work due to residual, debilitating pain.

Texas insurers pay injury claims based on what you can prove, not what you deserve. They aren’t in the business of paying full value on the first try; they’re counting on you to accept less because you need money now.

Why Insurance Underpayment Happens

Insurers make money by collecting premiums from their policyholders and paying out as little as possible on claims. Your claim is a line item they want to close as quickly and cheaply as possible. As such, adjusters are trained to settle fast, and a quick offer might tempt you to accept before you know the full extent (and cost) of your injuries.

Adjusters also undervalue what they can’t easily measure. Pain, lost sleep, anxiety behind the wheel on I-35 don’t come with receipts, so they’re easy to undercut.

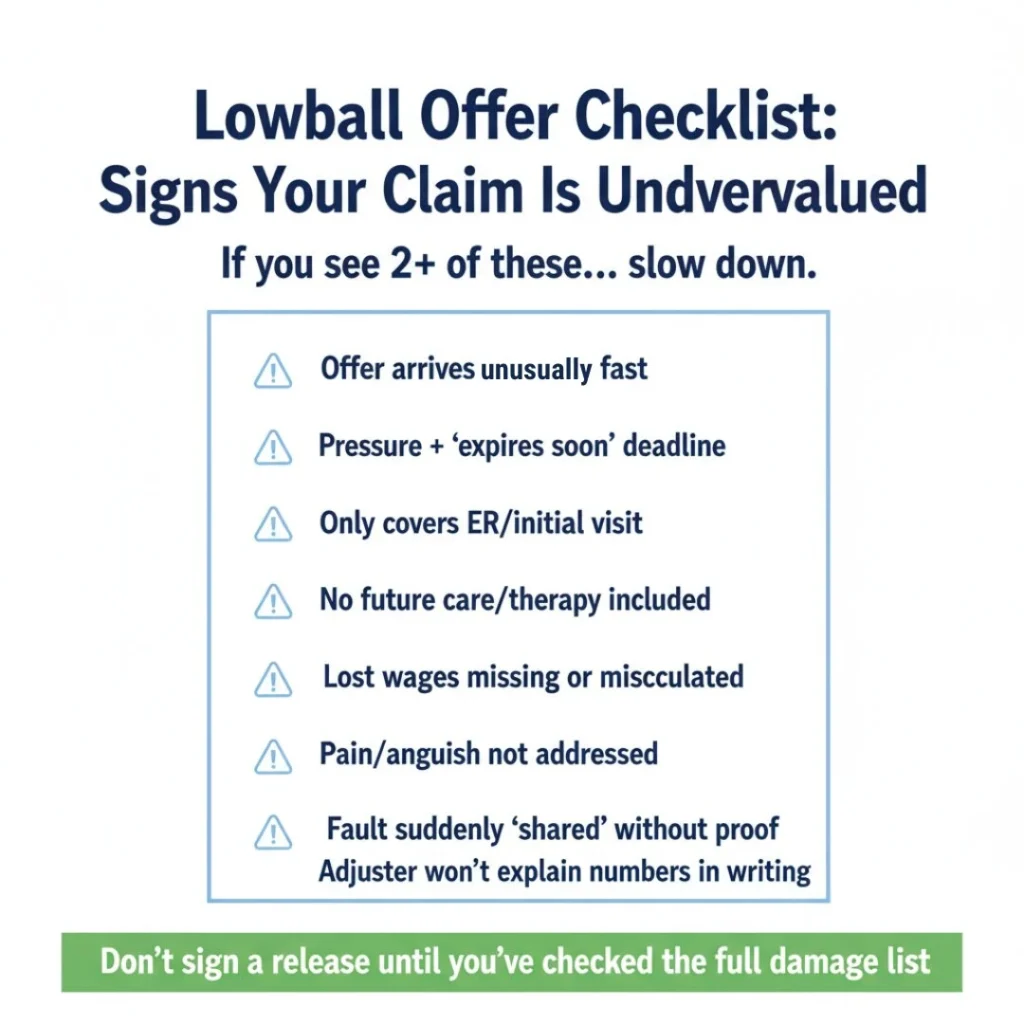

Signs Your Offer Is Undervalued

The first offer is almost never the best offer. It’s a starting point designed to test whether you’ll push back. A lowball offer often arrives within days of your accident. That speed is a red flag. If the adjuster then pressures you to sign that offer quickly or says it expires soon, they’re hoping you won’t have time to calculate what you’re owed.

The number may cover your current medical bills, but it likely ignores future treatment, physical therapy, or surgery you might need. Because you don’t necessarily know what will be needed or the value of those damages, it’s easy to overlook them.

Check whether the offer accounts for lost wages. If you’ve missed two weeks at work and the math doesn’t add up, something’s wrong.

Non-economic damages (pain, mental anguish, loss of enjoyment) are frequently left out entirely. Texas law allows recovery for these, but insurers won’t volunteer them.

Texas-Specific Factors That Impact Claim Value

Texas uses modified comparative fault. If you’re found partially at fault, your recovery is reduced by your percentage of responsibility. If you’re 51% or more at fault, you become ineligible to recover under Texas law.

Insurers know this and may try to shift blame onto you to reduce what they owe. The adjuster might point to your speed, your lane change, or whether you were looking at your phone. Every detail matters when fault is contested.

How Deadlines Influence Negotiation

Texas has a two-year statute of limitations for most personal injury claims. If you miss that deadline, you lose the right to sue, no matter how strong your case. Insurers track this deadline, and they may stall, hoping you’ll run out of time and accept whatever’s on the table.

Sending a demand letter months before the deadline gives you room to negotiate; waiting until the last minute limits your options.

Filing a lawsuit before the deadline preserves your claim and signals you’re serious. That shift in leverage often changes the conversation. Filing a lawsuit does not guarantee that your claim will be dragged into court—you can continue to negotiate throughout the discovery process and settle privately before litigation begins.

How to Counter Underpayment and Maximize Recovery

If you suspect the insurance company is underpaying you or acting in bad faith, take action right away. Start by documenting everything: medical records, bills, pharmacy receipts, mileage to appointments, or anything else pertaining to your case. Keep everything organized in a running file.

Take photos of your injuries as they heal. Bruises fade, but pictures don’t.

Track your lost wages with pay stubs and a letter from your employer. If you’re self-employed, gather invoices or contracts showing what you would have earned.

Write down how the injury affects your daily life. Can you pick up your kids? Sleep through the night? Drive without anxiety? These details support non-economic damages.

Finally, get copies of the police report and any witness statements. These establish what happened before the insurer tries to rewrite the story.

Elements of a Strong Demand Package

A demand letter is a formal request to the insurer detailing a financial valuation of the losses you have sustained. A good demand letter should itemize every category of damages: medical expenses (past and future), lost income, out-of-pocket costs, and pain and suffering. Include a specific dollar amount. Adjusters expect negotiation, so your initial demand should leave room to come down while still reaching fair value.

This letter should explain in detail how the injury has changed your life, crafting a clear narrative connecting the crash to your current situation strengthens your position.

When sending this letter, attach supporting documents like medical records, bills, proof of income loss, and photos make your demand harder to dismiss.

When to Seek Litigation and How a Lawyer Helps

If the insurer won’t move, filing a lawsuit may be the next step. An experienced attorney handles negotiations, paperwork, and deadlines, as well as collecting further evidence that supports your claim. A filed case opens discovery, where your attorney can demand internal documents and depositions.

Trial preparation changes the math for insurers. When they see you’re willing to go to a jury, settlement offers often increase. Texas juries have awarded significantly more than initial offers in cases where claimants refused to accept undervaluation. In one Dallas County case, a jury awarded over $1 million after the insurer’s pre-trial offer fell far short of covering the plaintiff’s damages.

Our team at Angel Reyes & Associates has guided Texans through situations like this for over 30 years. Reach out to us for a free consultation to learn more about your options and what your claim may be worth.

Insurance Underpayment FAQs

How do I know if my settlement offer is too low?

Compare the offer to your actual costs: medical bills (current and projected), lost wages, and the impact on your daily life. If the number doesn’t cover these, it’s likely undervalued.

Can I still negotiate after receiving an initial offer?

Yes. The first offer is a starting point. A documented demand letter with itemized damages often leads to a higher counteroffer.

Should I hire a lawyer for a lowball offer?

An attorney can evaluate whether the offer reflects fair value, handle negotiations, and prepare for litigation if needed. At Angel Reyes & Associates, our attorneys work on contingency, so there’s no upfront cost to you.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 70,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Graham Griffin

Editor

Graham Griffin is the Web & Content Manager at Angel Reyes & Associates, where he oversees content strategy, AI-powered workflows, a...

Spencer Browne

Reviewer

Spencer Browne is a partner at Angel Reyes & Associates and a Board Certified personal injury trial lawyer with nearly 100 jury trials a...