How to Prove Diminished Value Claims in Texas

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- Diminished value is most commonly recovered through third-party claims against the at-fault driver's insurer. First-party diminished value under your own collision coverage is often disputed.

- Strong diminished value claims require credible evidence, including a professional appraisal, repair documentation, and local market comparisons showing how accident history reduces your vehicle's value.

- Texas proportionate responsibility rules can reduce or restrict diminished value recovery if you share fault, and signing a release too early can waive your claim entirely.

You were rear-ended in rush hour traffic while driving home from work on I-35E near the Design District. The other driver admitted fault at the scene. Your car spent three weeks at the body shop, and the repairs look flawless, but when you checked your trade-in value at a Plano dealership, the offer came in thousands lower than expected because your vehicle now has an accident on its history report.

This gap between what your car was worth before the crash and what it’s worth after quality repairs is called “diminished value.” Texas law allows you to recover this loss in many situations. The challenge is knowing how to prove it, and the evidence that insurers will actually respond to.

Types of Diminished Value

Diminished value (DV) is the reduction in your vehicle’s market value caused by its accident history, even after complete repairs. Buyers pay less for cars with reported collisions. That stigma creates a real financial loss that you may be able to get compensation for.

There are three different types of diminished value:

- Inherent diminished value is most commonly pursued in Texas claims. It reflects that people don’t want to pay full price for a previously wrecked vehicle, even if the repairs are high quality.

- Repair-related diminished value applies when repairs didn’t restore the car to its original condition.

- Immediate diminished value describes the drop in value right after the crash, before any repairs.

Diminished value is separate from your repair costs. It’s also different from normal depreciation or cases in which a car is totaled. Repair costs pay to fix the damage. Diminished value covers the reduced resale value even after the car was repaired. If you’ve been in a car accident and your vehicle was repaired, you may be able to make both types of claims.

Third-Party vs First-Party Claims

Texas recognizes diminished value as a recoverable property damage. However, your path to recovery depends on whether you’re filing a third-party claim or a first-party claim:

- Third-party diminished value claims are filed against the at-fault driver’s liability insurance. This is the most common and successful route for diminished value recovery in Texas. In this case, you’re seeking compensation from the person who caused the crash, not your own insurer. Texas law treats diminished value as part of the property damages that the at-fault party owes you.

- First-party diminished value claims are filed under your own collision coverage. These are much harder to win. The Texas Department of Insurance has noted that many auto policies do not promise diminished value under collision coverage. Insurers frequently cite this guidance when denying first-party diminished value claims. Whether or not you can recover damages depends on your specific policy language.

In a third-party claim, you must prove three things:

- That the other driver was at fault

- That your vehicle lost value due to the accident

- The amount of your loss

In this case, your leverage comes from the at-fault driver’s legal liability, not a contract.

First-party claims depend entirely on what your policy promises. When insurers deny these claims, disputes sometimes shift to valuation disagreements, rather than coverage questions. For policies issued or renewed on or after January 1, 2026, new appraisal provisions may affect how valuation disputes are handled.

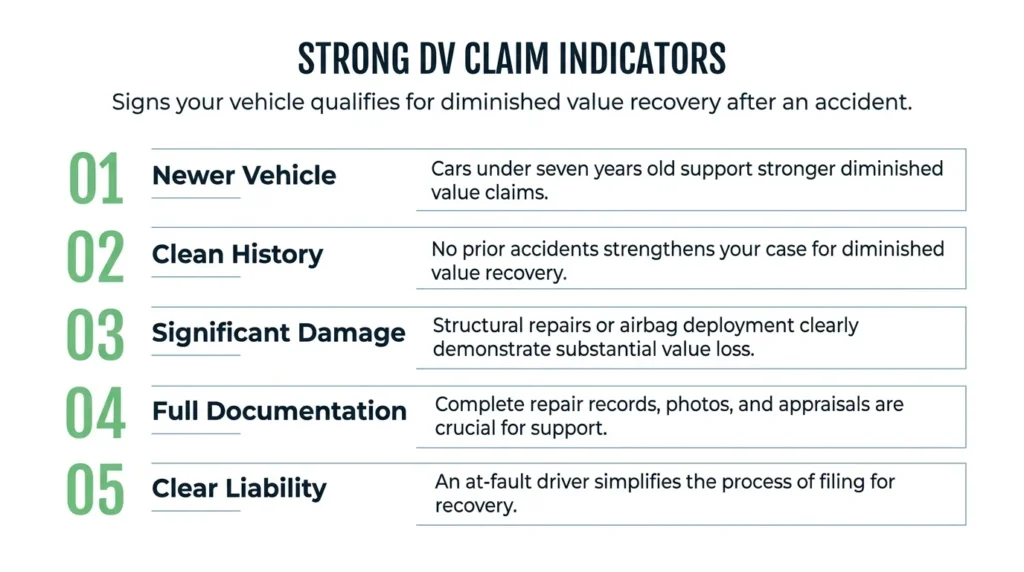

Diminished Value Eligibility Checklist

Not every accident creates a strong diminished value claim. Before investing in an appraisal, consider whether your situation has the right ingredients first.

Strong diminished value indicators include:

- Newer vehicle (typically under seven years old)

- Clean title and no prior accident history

- Significant damage (i.e., to structural repairs, airbag deployment, framework, etc.)

- Complete repair documentation with photos

- Clear third-party liability (meaning the other driver was at fault)

Weak diminished value indicators include:

- Older or high-mileage vehicles

- Preexisting damage or prior accidents on the vehicle history report

- Minor cosmetic repairs only

- Disputed liability or shared fault

- Missing repair records or photos

Additionally, local market data is important evidence for diminished value claims. Local dealer trade-in offers and comparable listings are more accurate than more general national pricing formulas. An adjuster reviewing your claim will want to see what buyers in your market actually pay for similar vehicles, both with and without accidents on their history report.

Some drivers explore diminished value through uninsured or underinsured motorist (UM/UIM) property damage coverage. This route is policy-dependent and requires a careful review of your coverage terms. If you’re unsure whether your situation warrants legal help, a consultation can clarify your options.

How Diminished Value Affects Your Total Settlement Value

Diminished value is one component of your property damage claim. When it’s put together the right way, it can significantly increase your overall recovery amount.

A complete property damage claim may include:

- Repair costs

- Rental car or loss of use

- Towing and storage fees

- Diminished value

Adjusters evaluate all these costs together. Presenting diminished value alongside documented repair costs and rental expenses can help illustrate your total losses more clearly. Understanding average car accident settlements in Texas can help you understand whether an offer includes all your damages.

Remember, Texas proportionate responsibility rules affect diminished value recovery. Under Texas Civil Practice and Remedies Code Chapter 33, your recovery is reduced by your percentage of fault. If you’re found more than 50% responsible for the accident, you cannot recover any damages, including diminished value. This makes understanding Texas comparative negligence rules essential when fault is disputed.

Also, timing is everything. Property damage claims (including diminished value) generally must follow a two-year statute of limitations under Texas Civil Practice and Remedies Code Chapter 16. This is why you should raise the issue of diminished value as soon as repairs are complete and you can document the loss.

How Insurance Release Forms Affect Your Diminished Value Claim

Many drivers accidentally waive their diminished value claim by signing a release too early. Property damage release forms often contain language that states you must give up “all claims,” which can restrict your right to pursue diminished value if it’s not specifically excluded.

The safest approach is to address diminished value after repairs are complete (when you know the full scope of damage and what’s on your vehicle history report) but before signing any final release forms. If the insurer asks you to sign paperwork, confirm whether diminished value is included in the payment or reserved for separate negotiation.

Property damage and bodily injury settlements are typically separate. Make sure you understand which part of the claim the insurer is asking you to close.

What Evidence Do Insurers Actually Respond To?

Adjusters pay diminished value claims when the proof is credible, specific, and litigation-ready. Generic estimates or online calculator results rarely make a difference.

Highest-impact evidence:

- An independent diminished value appraisal that clearly explains how it was calculated and uses local market examples for comparison

- A final repair invoice with itemized parts and labor

- Pre-repair and post-repair photos

- Documentation of structural repairs, frame measurements, or airbag deployment

Market proof that strengthens your claim:

- Written dealer trade-in statements showing reduced offers due to accident history

- Comparable vehicle listings from your local area (same year, make, model, and mileage), both with and without accident history

- Carfax or AutoCheck reports showing how the accident appears to buyers

Remember, vehicle history reports don’t always update immediately after repairs. The time between repair completion and report updates can affect your documentation strategy.

Valuation Methods

The most persuasive diminished value valuations use a market-based approach. This means an appraiser determines your vehicle’s pre-loss value, then compares it to its post-repair value using actual sales data and local comparisons. This method makes sense to both adjusters and juries.

Some insurers reference formula-based approaches (sometimes called “17c”). These formulas often produce lower values than what is supported by market data. However, Texas does not require any specific diminished value formula. You can counter formula-based offers with documented market comparisons showing what local buyers actually pay.

Online diminished value calculators and percentage-based estimates rarely succeed without supporting documentation. Adjusters dismiss claims that lack methodology and proof.

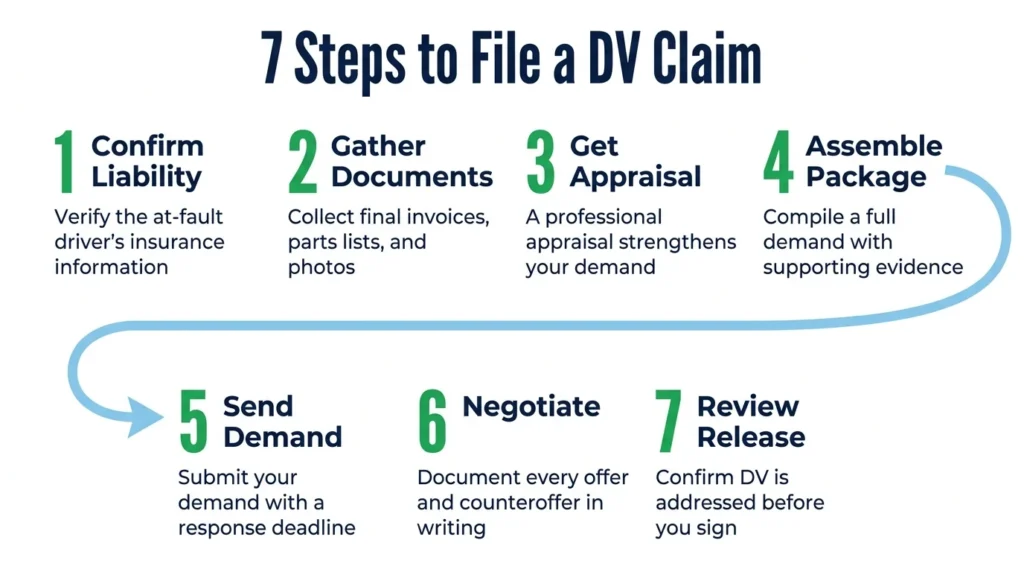

How to File a Diminished Value Claim in Texas

For third-party claims, follow this process after your repairs are complete:

- Confirm liability and coverage. Verify the at-fault driver’s insurance information and confirm that the property damage claim is open.

- Complete repairs and gather documentation. Collect final invoices, parts lists, photos, and any structural repair records.

- Obtain a diminished value appraisal. For vehicles with significant damage or previously high value, a professional appraisal can strengthen your claim.

- Assemble your demand package. Include a cover letter summarizing the crash, liability, vehicle details, repair summary, and your requested diminished value amount.

- Send the demand with a response deadline. Keep copies of everything.

- Negotiate in writing. Document all offers and counteroffers.

- Review any release forms carefully before signing. Confirm that diminished value is addressed in the release forms.

A strong demand package includes your appraisal, repair invoices, damage photos, market comparisons, and any dealer statements. Request that payment must explicitly include diminished value or that diminished value should be reserved and handled separately later.

Common Adjuster Objections & Practical Counter-Arguments

“We don’t pay diminished value in Texas.”

This objection confuses first-party claims with third-party claims. In a third-party claim, you’re pursuing damages from the at-fault driver, not policy benefits. Diminished value is a recognized component of property damages under Texas law.

“Your car is repaired, so there’s no loss.”

Quality repairs don’t erase accident history. Market data consistently shows that buyers pay less for vehicles with reported collisions. Counter this argument with dealer trade-in statements and comparable listings.

“Your appraiser’s number is too high.”

Ask the adjuster to provide their reasoning for a lower figure. Point to your appraiser’s credentials, methodology, and local market comparisons. Offer to accept a joint inspection if appropriate.

What to Do If the Insurer Delays or Refuses to Negotiate

Build a clean paper trail. Send written follow-ups with specific deadlines. Keep copies of all communications and document the adjuster’s responses (or lack thereof).

If the insurer’s conduct appears unreasonable, you may consider filing a complaint with the Texas Department of Insurance. TDI guidance on unfair settlement practices outlines expectations for claims handling. A complaint won’t force payment, but it will create a record.

When negotiations fail, you can still file a lawsuit. Diminished value can be pursued as property damages against the at-fault driver within the two-year limitations period. An attorney can evaluate whether your evidence supports a lawsuit and how fault disputes might affect your recovery.

When It Makes Sense to Get Legal Help

Some diminished value claims are straightforward enough to handle yourself. Others benefit from professional support.

Consider consulting an attorney when:

- Fault is disputed or you’re being blamed for the crash

- The accident involved a commercial vehicle or truck

- Your vehicle had significant value prior to the crash

- The insurer denied your claim or made an unreasonably low offer

- You are also pursuing injury claims

Consider consulting a professional appraiser when:

- The insurer is demanding a documented explanation of how the claim was calculated

- Your vehicle is newer, a luxury vehicle, or had substantial pre-loss value

- You need credible market comparisons for your local area

When choosing legal representation, look for attorneys who have experience with Texas property damage claims, documented results, and accessibility.

Angel Reyes & Associates has offices across Texas, and we have helped clients recover more than $1 billion in damages for more than 30 years. You can review our case results and client testimonials to see how we’ve helped clients in situations like yours.

If you’re dealing with a diminished value dispute after a car accident in Texas, we offer free consultations and work on contingency, which means you pay no fee unless we win. Contact us today to discuss your options.

Past results do not guarantee future outcomes.

Diminished Value Claim FAQs

Can a leased or financed car have a diminished value claim in Texas?

Yes. A vehicle can lose market value even if you do not own it outright, but the lender or leasing company may have a say in how property-damage payments are handled.

Will a clean title prevent a diminished value claim?

No. A clean title does not erase an accident history, and buyers or dealers may still offer less once a crash appears on Carfax or similar reports.

Do minor repairs automatically mean there is no diminished value?

Not always. Smaller cosmetic repairs often lead to weaker claims, but the vehicle’s age, mileage, brand, and buyer market can still affect whether any measurable value was lost.

Can you ask for diminished value if you plan on keeping the car instead of selling it?

Usually, yes. Diminished value is based on reduced market value after the accident, not on whether you sell the vehicle right away.

Does an aftermarket parts repair affect a diminished value claim?

Sometimes. If the repair used non-OEM parts, or there are documented quality concerns, that may support an argument that the vehicle is worth less on the market.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 55,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...