Texas UM/UIM Claims When the At-Fault Driver Is Under 18

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- Your UM/UIM coverage can pay for injuries caused by an uninsured or underinsured teen driver, even though you're filing against your own policy.

- Texas law may hold parents liable through license application signature requirements or negligent entrustment when they knew the teen was an unsafe driver.

- The two-year statute of limitations applies to most claims, but UM/UIM policies require prompt notice, so delays can hurt your case even when legal deadlines seem far away.

A teenager ran a red light at the intersection of Preston Rd. and Belt Line in Addison. Your car took the impact on the driver’s side. Now you’re dealing with injuries, medical bills, and the discovery that the teen who hit you has no insurance at all. The at-fault driver’s parents aren’t returning your calls, and you’re wondering who is going to pay for this.

Young drivers in Texas are more likely to carry minimum coverage or no coverage at all. When that happens, your own uninsured/underinsured motorist (UM/UIM) coverage often becomes the primary path to compensation. But it’s not always your only option.

Why Teen-Driver Crashes Create Coverage Gaps

Teen drivers in Texas frequently carry inadequate insurance. Some are listed on a parent’s policy with minimum limits. Others are excluded from household coverage entirely. In hit-and-run situations, the driver may never be identified.

These scenarios create what’s called a “coverage gap.” The at-fault driver caused your injuries, but there’s no insurance to pay your claim. This is where your own UM/UIM coverage steps in.

A UM/UIM claim is a “first-party” claim. You’re filing against your own insurance policy, not the other driver’s. Your insurer pays you directly for losses caused by someone else’s negligence when that person lacks adequate coverage.

The goal after any teen driver accident is to identify every applicable policy and liability theory early. That means looking at your UM/UIM coverage, any policy the teen might have, household policies covering the teen, and claims against adults who may share responsibility.

Texas UM/UIM Basics for Minor-At-Fault Crashes

Understanding how UM/UIM works in Texas helps you know what to expect from your claim.

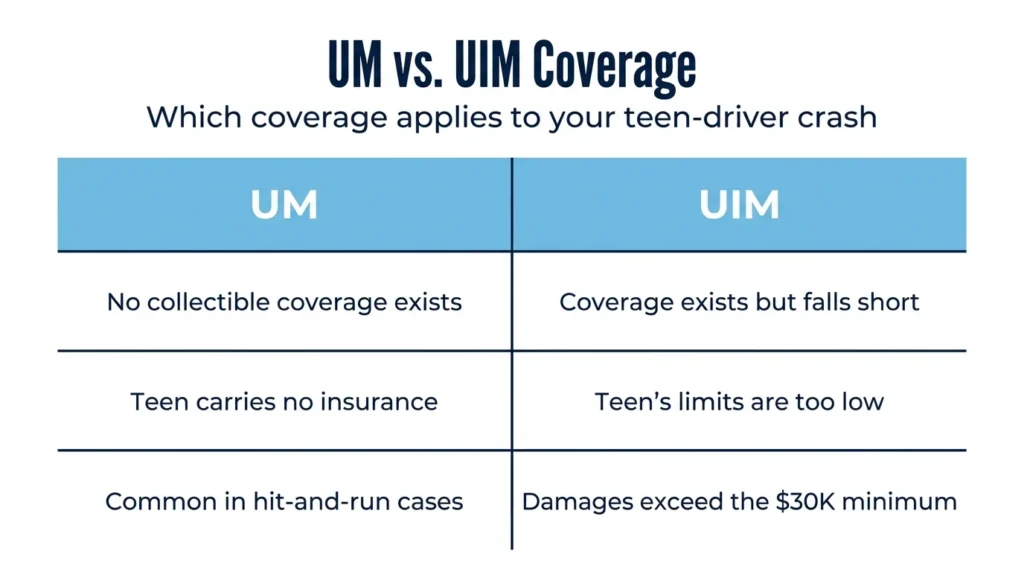

UM coverage applies when the at-fault driver has no collectible liability insurance. This includes situations where the driver is truly uninsured, flees the scene, or has coverage that’s been denied or excluded.

UIM coverage applies when the at-fault driver has insurance, but the limits aren’t enough to cover your damages. Texas requires only $30,000 per person in minimum liability coverage. Serious injuries can easily exceed that amount.

According to the Texas Department of Insurance, UM/UIM coverage can pay for medical expenses, lost wages, pain and suffering, and other damages resulting from a crash with an uninsured or underinsured driver.

Texas law requires insurers to offer UM/UIM coverage. Under Texas Insurance Code Chapter 1952, you have this coverage unless you reject it in writing. If you never signed a rejection form, you likely have UM/UIM protection on your policy. Check your declarations page to confirm your limits.

UM vs UIM: Which One Applies?

UM applies when there’s no collectible coverage at all. Examples include a teen who was driving without any insurance, a hit-and-run where the driver is never identified, or situations where the teen was excluded from the family policy.

UIM applies when coverage exists but falls short. If the teen carried minimum limits of $30,000 but your medical bills alone exceed $75,000, UIM covers the gap between what their insurance pays and your actual damages.

You can pursue the teen’s liability coverage first and still preserve your UIM claim for the shortfall. Be careful about the sequence—accepting a settlement from the at-fault driver’s insurer without your own insurer’s consent can jeopardize your UIM rights.

Who Can Be Responsible Beyond the Teen

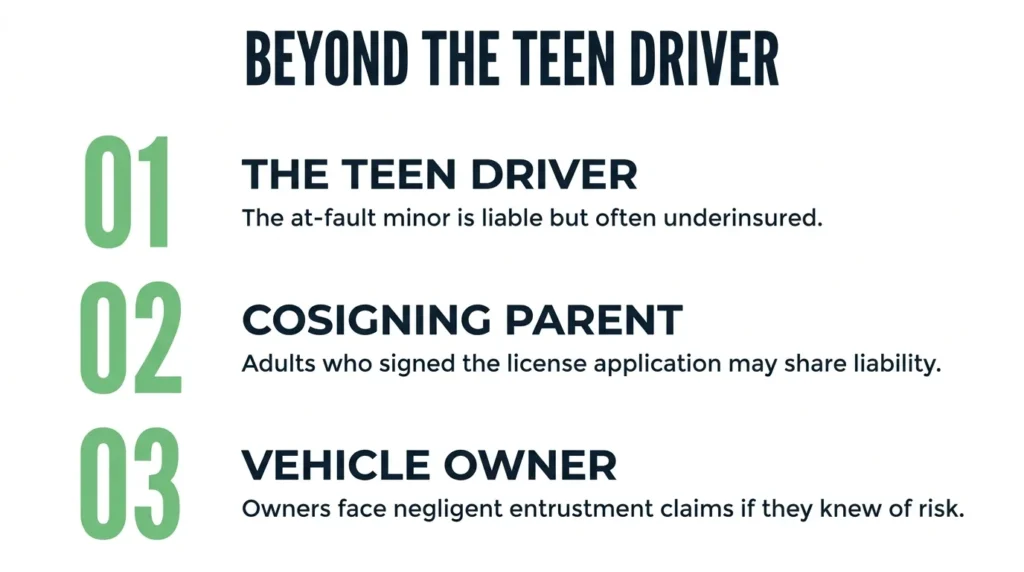

Your UM/UIM coverage provides one path to compensation. But when a minor causes a crash, liability can extend to adults in ways that expand your recovery options.

Signature Liability Under Texas Law

When a minor under 18 applies for a Texas driver’s license, an adult must sign the application. Under Texas Transportation Code Chapter 521, that signature creates potential liability for the adult if the minor causes a crash.

This is sometimes called “cosigner liability.” The adult who signed the license application may be held responsible for damages caused by the teen’s negligent driving. Identifying who signed that application is an important early step in minor car accident cases.

Negligent Entrustment Claims

Negligent entrustment is a separate theory of liability. It applies when someone gives a vehicle to a driver they knew (or should have known) was unsafe or incompetent.

For teen drivers, relevant facts include:

- Prior crashes or traffic tickets

- Known history of reckless driving or speeding

- Previous texting-and-driving incidents

- Alcohol or drug issues

- Violations of graduated driver’s license (GDL) restrictions

If a parent knew their teen had multiple speeding tickets and a prior at-fault crash, then handed over the keys anyway, that parent may face direct liability for negligent entrustment.

Evidence that supports these claims includes the police report narrative, witness statements, dashcam footage, social media posts, and the teen’s driving history. Preserving this evidence early strengthens your position whether you’re pursuing a UM/UIM claim, a third-party claim, or both.

Step-by-Step: Filing a Texas UM/UIM Claim After a Teen Crash

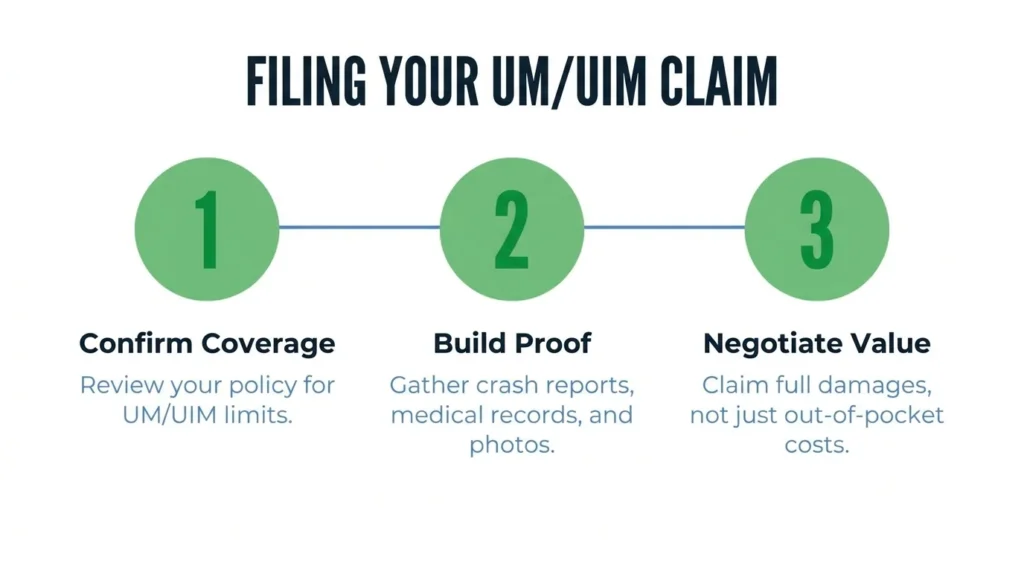

After an accident with an uninsured or underinsured teen driver, knowing what steps to take helps you avoid common mistakes that could jeopardize your claim.

Step 1: Confirm all applicable coverages. Review your own policy for UM/UIM limits, PIP, and MedPay. Request the teen’s insurance information from the police report. If the teen claims to have coverage, get written confirmation of limits or a denial letter.

Step 2: Build your proof package. Your UM/UIM claim requires evidence of both fault and damages. Gather the crash report, photos of the scene and vehicles, witness contact information, all medical records and bills, proof of lost wages, and a written narrative of your injuries and recovery.

Step 3: Handle any liability claim carefully. If the teen has some coverage, you may receive a settlement offer from their insurer. Before signing any release, understand how it affects your UIM rights. Many policies require your insurer’s consent before you settle with the at-fault driver. Signing without that consent can eliminate your UIM claim entirely.

Step 4: Negotiate UM/UIM value like an injury claim. UM/UIM isn’t just reimbursement for out-of-pocket costs. You can claim non-economic damages like pain and suffering, loss of enjoyment of life, and compensation for future medical needs. Document everything that supports the full value of your claim.

What If It’s a Hit-and-Run?

Hit-and-run crashes are common UM triggers. If the driver who hit you on I-635 fled the scene and was never identified, your UM coverage may be your only recovery option.

Evidence matters even more in hit-and-run cases. File a police report immediately. Canvass the area for surveillance cameras at nearby businesses. Get contact information from any witnesses. Note the exact time and location with as much precision as possible.

If the driver is later identified as a teen, that opens potential third-party claims against parents or vehicle owners while your UM claim continues.

Coordinating Multiple Policies

Teen crashes often involve layered coverage situations. The teen might be driving a parent’s car, covered under a household policy, or specifically excluded from coverage.

First, identify and pursue liability coverage, then evaluate UIM for any remaining gap. Policy language controls priority, and every policy is different.

Common teen coverage setups include:

- Teen listed on parent’s policy (coverage likely applies)

- Teen with separate policy (may have lower limits)

- Teen excluded from household policy (enables you to file a UM claim)

- Permissive use of someone else’s vehicle (owner’s policy may apply)

Questions about stacking UM/UIM limits or coverage priority require careful policy review. Don’t assume anything based on general rules.

Deadlines & Timing When a Minor Is Involved

The baseline statute of limitations for personal injury claims in Texas is two years from the date of the crash under Texas Civil Practice & Remedies Code § 16.003.

When a minor is at fault, some timing rules can be affected. But don’t assume you have extra time across the board. UM/UIM policies have their own requirements for prompt notice and cooperation. Delays hurt your ability to gather evidence even when legal deadlines seem distant.

Mark your dates on a calendar immediately. Missing a deadline can eliminate your claim entirely, regardless of how strong your case might be.

When to Involve a Lawyer

Many UM/UIM claims resolve through negotiation. But teen-at-fault crashes more often involve complications that benefit from legal guidance.

Common friction points in UM/UIM claims include proving the other driver’s fault, documenting your damages thoroughly, and meeting policy conditions like timely notice. Your insurer will want a police report, medical records, and evidence supporting your claimed losses.

Consider consulting an attorney if you’re facing:

- Serious injuries requiring ongoing treatment

- Disputed fault or conflicting accounts

- An uninsured or unidentified driver

- Coverage denial or exclusion issues

- Pressure to sign releases quickly

- Multiple potential defendants or policies

A lawyer can investigate coverage options, build a comprehensive proof package, sequence settlements to protect your rights, and pursue liability theories like negligent entrustment when the facts support them.

At Angel Reyes & Associates, we’ve spent over 30 years helping Texas families recover after car accidents. We offer free consultations and work on contingency, meaning you pay no fee unless we win. Our attorneys have recovered more than $1 billion for clients across the state.

If a teen driver’s crash left you with injuries and questions about coverage, contact us to discuss your options. We’re available 24/7 to review your policies, identify all potential sources of recovery, and help you understand the deadlines that apply to your situation.

Past results do not guarantee future outcomes.

Underage Driver UM/UIM Claim FAQs

Does UM/UIM cover vehicle damage in Texas, or just injuries?

In Texas, UM coverage can also pay for damage to your car, but a deductible often applies to property-damage claims. Coverage details depend on your policy and the type of UM/UIM benefits you purchased.

Can I use UM/UIM if the teen was borrowing someone else's car?

Possibly, but the answer often depends on whose policy covered the vehicle, whether the teen had permission to drive, and whether any exclusion applies. That is why it’s important to identify both the driver’s insurance and the vehicle owner’s insurance early.

What if the teen driver got a ticket—does that prove my UM/UIM claim?

Not by itself. A citation can help support your case, but insurers usually still look at the full evidence, including the crash report, witness statements, photos, and medical records.

Can a passenger in my car make a UM/UIM claim too?

In many cases, yes, if the passenger qualifies as an insured under the policy or is covered under the UM/UIM terms. Whether they can recover usually depends on the policy language and the facts of the crash.

What should I bring when I open a UM/UIM claim after a teen-driver crash?

It helps to have the police report number, photos, witness names, the other driver’s information, your declarations page, and basic medical and wage-loss records. Starting with a complete file can reduce delays and make it easier to show both fault and damages.

About the Authors

Spencer Browne

Writer

Spencer Browne is a partner at Angel Reyes & Associates and a Board Certified personal injury trial lawyer with nearly 100 jury trials across Texas. He focuses on car, truck, and wrongful death cases, with notable verdicts including a landmark win in the Choctaw Casino bus crash case. A recognized speaker and legal educator, Spencer is a member of the American Board of Trial Advocates and has been honored as a Texas Super Lawyer and one of D Magazine’s Best Lawyers in Dallas. He brings deep trial experience and relentless advocacy to every client he represents.

Graham Griffin

Editor

Graham Griffin is the Web & Content Manager at Angel Reyes & Associates, where he oversees content strategy, AI-powered workflows, a...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...