UM/UIM & PIP Coverage When You’re Hurt Driving a Borrowed Car in Texas

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- The vehicle owner's insurance typically responds first in borrowed-car crashes, but your own UM/UIM policy may provide additional coverage depending on policy definitions and exclusions.

- Unlisted household driver exclusions, permissive use disputes, and proof issues are the most common reasons UM/UIM claims get denied in borrowed-car situations.

- Anti-stacking clauses and "other insurance" provisions can limit recovery even when both the owner and driver have UM/UIM coverage.

You borrowed your coworker’s truck to help a friend move last Saturday. On your way back through Arlington, someone ran a red light and hit you. Now you’re dealing with a shoulder injury, missed work, and a confusing insurance situation. The at-fault driver had minimum coverage that won’t come close to covering your medical bills.

Your coworker’s insurance is asking questions. Your own insurance says they need to investigate. And you’re wondering whether anyone’s uninsured/underinsured motorist (UM/UIM) coverage will actually help you.

Borrowed-car crashes create some of the most complicated insurance situations in Texas. Understanding how the vehicle owner’s policy interacts with your own policy can make the difference between a fair recovery and a frustrating denial.

What Coverage May Apply When You Crash a Borrowed Car in Texas

Most borrowed-car claims turn on three questions:

- Did you have permission to drive the car?

- Which insurance policy applies first?

- Is UM/UIM (and PIP) available under the owner’s policy, your policy, or both?

Permission matters, but it’s not a guarantee of coverage. Policy language still takes precedence. Even if the owner handed you the keys and said, “Take your time,” exclusions in their policy might still apply to you.

In Texas, these situations come up constantly. Multiple vehicles in households, rides to work along I-35, borrowing a friend’s car to run errands in Round Rock. The more people share vehicles, the more opportunities for coverage disputes.

Here’s the general rule: the vehicle owner’s insurance typically responds first in borrowed-car situations. Your own policy may provide secondary coverage depending on the coverage type and policy terms.

Three pitfalls cause most borrowed-car UM/UIM problems:

- Excluded or unlisted household drivers

- UM/UIM definitions that limit who qualifies as an “insured”

- Policy limits and anti-stacking language that cap recovery

How Texas Auto Insurance “Follows the Car” vs. “Follows the Person”

Many people assume their own insurance automatically covers them in any car. Others assume the car owner’s insurance covers anyone who borrows it. Both assumptions can break down, especially for UM/UIM and PIP.

Understanding a few key terms helps clarify the confusion.

- A “named insured” is the person listed on the policy.

- A “family member” or “household member” typically means someone related to the named insured who lives in the same home.

- A “permissive user” is someone who has the owner’s permission to drive.

- “Occupying” generally means in, upon, getting in, on, out, or off a vehicle.

UM/UIM coverage works differently from liability coverage. You may be covered because of who you are (your status as an insured) or where you were (occupying a covered car). Standard Texas personal auto policy forms define these terms specifically, and the definitions vary between insurers.

One policy may be primary while another is excess. The answer to which one covers you can change depending on which coverage you’re claiming and how each policy is worded.

Permission Helps, But It Doesn’t Override Exclusions

Having permission to drive the borrowed car is often necessary but not always sufficient. Many denials happen because exclusions apply even when the owner clearly said yes.

Common misunderstandings include thinking “I had the keys” equals coverage, or “they let me borrow it before” means you’re automatically covered now. Living together doesn’t guarantee coverage either.

Insurers ask about your relationship to the owner and whether you have regular access to the vehicle for good reason. If you regularly drive a household member’s car, you may need to be listed on their policy to avoid disputes. This depends on the policy and the insurer, but understanding how multi-car policies work can help you spot potential problems before they become claim denials.

Texas UM/UIM Basics & the Written Rejection Rule

Before figuring out how two policies might layer together, you need to understand what UM/UIM actually covers.

UM/UIM can pay for bodily injury damages when you’re hurt by an uninsured driver or a driver whose insurance isn’t enough to cover your losses. The Texas Department of Insurance UM/UIM and PIP explains that UM coverage may also include property damage in some situations, subject to policy terms.

Texas Insurance Code § 1952.101 requires insurers to offer UM/UIM coverage. If you want to reject it, that rejection must be in writing. If you or the person you borrowed the car from rejected UM/UIM on a policy, there may be no UM/UIM benefits available under that policy to access.

Where PIP Fits In

Personal injury protection (PIP) is often discussed alongside UM/UIM because both can help after a crash, but they work differently. PIP generally pays medical expenses and lost income up to policy limits, regardless of who caused the crash.

PIP availability and priority may differ from UM/UIM. It depends on the policy and who qualifies as an insured person. If you’re dealing with mounting medical bills after a car accident, you may be able to pursue PIP early for treatment while larger UM/UIM damages are still being evaluated.

How the Owner’s Policy & Your Policy May Layer

This is where borrowed-car claims get complicated. Which policy pays first? When might a second policy contribute? What language changes the outcome?

In general, the owner’s policy typically pays first for many coverages. Your policy may apply if the owner lacks adequate coverage. But UM/UIM has its own rules.

UM/UIM coverage often depends on whether you qualify as an “insured” under the owner’s UM/UIM coverage and whether you qualify as an “insured” under your own UM/UIM while occupying a non-owned vehicle. Both questions are policy-specific.

What to Look for in the Policy

The fastest way to reduce denial risk is to identify the clauses the adjuster will rely on. Check the UM/UIM definitions section, exclusions, “other insurance” provisions, limits, and conditions.

“Occupying” issues can matter in some disputes. Whether you were in the vehicle, getting in, or getting out can affect coverage. Document your position and timing at the crash.

Policy conditions can also trip up claims. Prompt notice requirements, cooperation clauses, medical authorizations, proof of loss deadlines, and settlement consent provisions all vary by policy. Missing one can jeopardize an otherwise valid claim.

The Unlisted Household Driver Problem

If you live with the vehicle owner or regularly drive their car, you’re in the zone where “permissive use” disputes often happen.

Insurers treat household drivers differently from occasional borrowers. Risk rating and underwriting rules assume that people who live together and share vehicles will be listed on the policy. When they’re not, exclusions may apply.

Common fact patterns include a spouse or partner not listed on the policy, an adult child home from college, a roommate who uses the car “sometimes,” or a long-term borrower. The Office of Public Insurance Counsel warns that even with permission, borrowed-car situations might not be covered depending on policy terms.

The practical prevention step is simple: confirm coverage with the insurer or agent before regular borrowing begins.

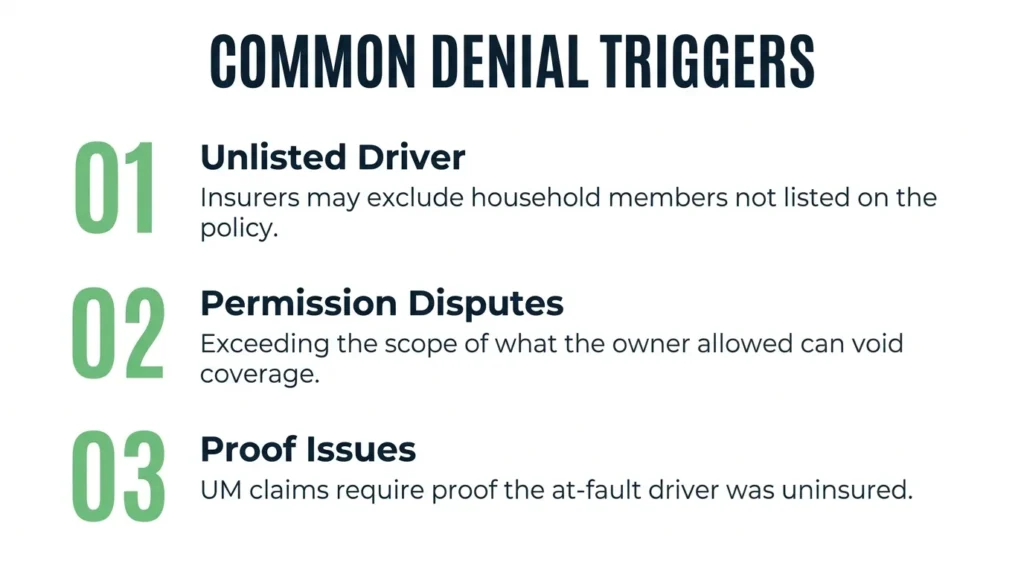

Common UM/UIM Denial Triggers in Borrowed-Car Cases

Understanding what adjusters look for helps you avoid common pitfalls.

Unlisted or household driver exclusions are the first major trigger. Insurers may allege misrepresentation if someone who should have been listed wasn’t. Evidence of where you live, how often you drove the vehicle, and whether you had regular access all becomes relevant.

Permissive use disputes are the second trigger. Was the permission broad or limited? Did you exceed the scope of what the owner allowed? “Borrow it for the afternoon” might not cover a week-long trip.

Proof issues are the third trigger, especially for UM claims. You may need to prove the at-fault driver was actually uninsured. Hit-and-run claims require specific proof. Early documentation of the crash, the other driver’s information, and your damages matters enormously.

Proof Checklist for the First Week

UM/UIM claims are document-driven. Lock down evidence early.

For crash documentation, gather:

- Police report information

- Witness contacts

- Scene photos

- Vehicle positions

- Any video sources from nearby businesses or dashcams

For insurance documentation, request:

- Declaration pages for both policies (owner and driver)

- Any rejection or selection forms

- Claim numbers

- Adjuster contact information

For medical and damages documentation, keep:

- ER and urgent care records

- Follow-up treatment plans

- Wage loss proof

- Receipts for out-of-pocket costs

Policy Limits, Offsets, & Anti-Stacking

Many people assume they can add UM/UIM limits across policies or vehicles. Policy language often prevents this.

Limits are ceilings. Insurers look at per-person and per-accident limits, plus credits and offsets. The specific formula depends on the policy and the facts.

“Stacking” means combining UM/UIM limits from multiple policies or multiple vehicles on the same policy. Anti-stacking clauses and “other insurance” provisions can restrict this. Even if both the owner and you have UM/UIM, the policy language may still limit your recovery.

Having two policies with UM/UIM doesn’t automatically mean double recovery. A review of both policies is essential to understand what’s actually available. Understanding what “full coverage” really means in Texas can help set realistic expectations.

Talk to a Texas Car Accident Attorney About Your Claim

Some borrowed-car UM/UIM claims resolve smoothly. Others become technical coverage fights that require legal help.

Red flags that justify a legal review include any denial citing “unlisted household driver,” “not an insured,” “no permission,” or “other insurance.” Requests for extensive recorded statements or broad medical authorizations are also warning signs.

When damages are significant (surgeries, long-term care, lost earning capacity), limits, stacking, and offset issues become outcome-determinative. Getting the coverage analysis right matters.

Angel Reyes & Associates has helped injured Texans navigate complex insurance situations for over 30 years. We’ve recovered more than $1 billion for our clients, and we offer free consultations with no fee unless we win.

We can review your policies, identify all available coverage, and help you understand your options.

Contact us to schedule a free consultation. Bring your policies, any denial letters, declaration pages, and medical records. We’ll help you understand where you stand.

Past results do not guarantee future outcomes.

Texas UM & UIM Coverage FAQs

Is there a deductible for uninsured motorist property damage in Texas?

Texas UM property damage coverage usually has a $250 deductible, but that deductible does not apply to bodily injury claims. Whether UM property damage is part of the claim depends on the policy and the type of loss involved.

Can I use UM/UIM if the crash was a hit-and-run in a borrowed car?

Possibly, but hit-and-run claims often depend on proving the other driver caused the crash and that the event qualifies under the policy. Photos, witness information, video, and a prompt police report can be especially important.

What if the borrowed car was being used for work or delivery when the crash happened?

Personal auto policies sometimes limit coverage when a vehicle is used for business purposes, especially for delivery or commercial driving. That can affect whether the owner’s policy, your policy, or neither one applies the way you expected.

Can a passenger in a borrowed car make a UM/UIM or PIP claim too?

Sometimes, yes, because some policies cover people occupying the insured vehicle, not just the driver. The answer depends on the policy language and whether the passenger fits the policy’s definition of an insured person.

What happens if I settle with the at-fault driver's insurer before checking UIM coverage?

Settling too early can create problems because some UIM policies require notice or consent before you release the other driver. If you skip that step, the insurer may argue that UIM benefits should be reduced or denied.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 55,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Graham Griffin

Editor

Graham Griffin is the Web & Content Manager at Angel Reyes & Associates, where he oversees content strategy, AI-powered workflows, a...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...