Can You Claim Lost Wages After a Motorcycle Accident in Texas?

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- Texas law lets injured riders recover past lost wages and future lost earning capacity after a crash.

- Self-employed riders must document income loss with tax returns, invoices, and canceled contracts.

- Texas's 51% fault rule can reduce or eliminate your recovery if you share blame for the crash.

You were heading home from a job site on Fredericksburg Road near I-10 when a driver ran a red light and took you off your bike. Now you’re weeks into recovery, your medical bills are stacking up, and the paycheck you count on to cover rent and groceries has stopped coming in. The crash wasn’t your fault, and the financial pressure is just as real as the physical pain.

Texas law gives injured motorcycle riders the right to recover income they’ve lost because of someone else’s negligence. Knowing what you can claim, and how to prove it, determines whether you walk away with fair compensation or settle for less than you’re owed.

Lost Wages Are Recoverable After a Motorcycle Crash

Texas allows you to recover compensation for income you could not earn while recovering from motorcycle crash injuries. This recovery falls under economic damages, which the law defines as compensation for actual financial loss you’ve already suffered.

Two categories cover income loss in a Texas motorcycle accident claim: past lost wages and future lost earning capacity. Both categories are recognized under the Texas Civil Practice and Remedies Code (CPRC) Chapter 41, which defines economic damages as compensatory damages for actual pecuniary loss.

You have two years from the crash date to file a personal injury claim under CPRC § 16.003. Miss that deadline and your right to recover lost wages is gone, regardless of how strong your documentation is.

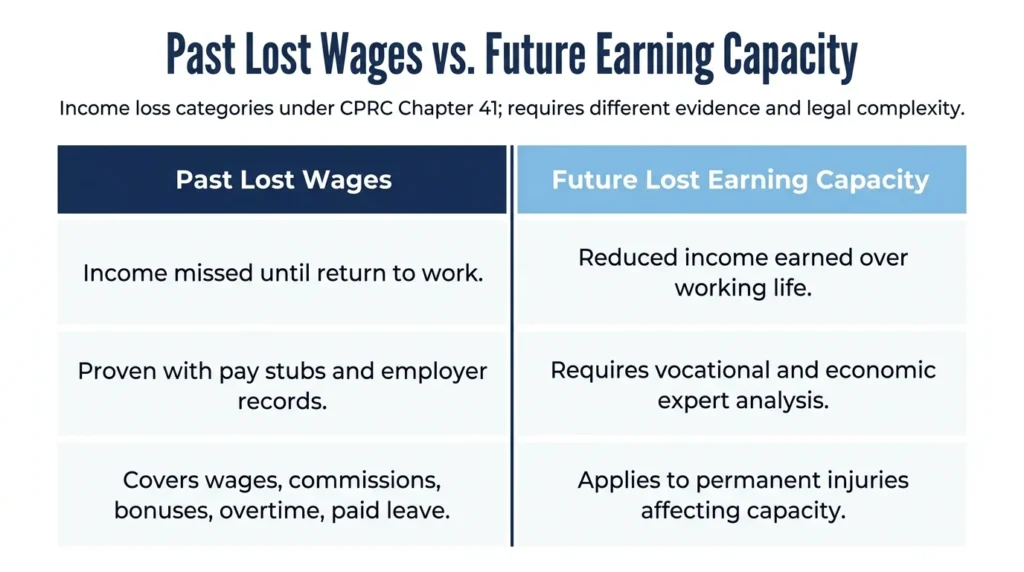

Past Lost Wages vs. Future Lost Earning Capacity

These two damage categories look related, but they require different types of evidence and carry different levels of legal complexity.

Past Lost Wages After a Motorcycle Injury

Past lost wages cover income you’ve already missed because your injuries kept you out of work. The calculation starts on the day of the crash and runs through the date you return to work or your claim resolves.

The income types covered are broader than you might realize:

- Hourly wages

- Salary

- Commissions

- Bonuses

- Overtime

- Vacation or sick time

If you had to draw down paid leave to cover your absence, that is income you had to spend early due to someone else’s actions.

If you’re employed, the documentation package is straightforward: pay stubs from before the crash, an employer verification letter confirming your pay rate and the days you missed, and a physician’s note confirming that your injuries prevented you from working during that period. The letter from your employer does the most work. It ties your daily rate to your missed days in a format insurers can’t easily dispute.

Future Lost Earning Capacity

Future lost earning capacity applies when your injuries are permanent or long-lasting enough to reduce what you can earn over the rest of your working life.

This applies if you cannot return to your prior occupation, if you can only work reduced hours, or if you are limited to lower-paying work because of physical or cognitive impairment from the crash. The gap between what you earned before and what you can earn now is the damage you’re claiming.

These claims require expert support that goes beyond a physician’s note. A vocational rehabilitation specialist evaluates what work you can physically and cognitively perform. An economic expert then projects the present value of that income difference over your remaining working years.

Courts need a credible analysis that translates your medical restrictions into specific dollar figures. Understanding how motorcycle accident settlements work in Texas can help you know what to expect from negotiations, including how insurers assess future earnings claims.

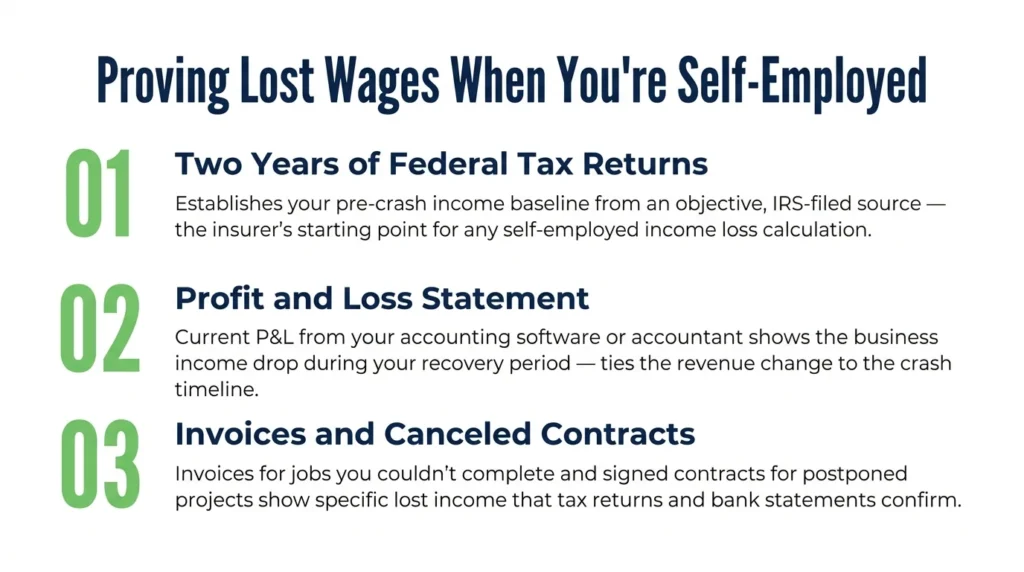

How Self-Employed Riders Document Income Loss

If you’re a self-employed motorcycle rider, you’ll face a challenge that employed workers don’t: there is no pay stub and no employer to write a verification letter. Building a credible income loss case requires a different set of records, but it is absolutely doable.

The starting point is your tax return history. Two years of federal tax returns establish your income baseline and show the insurer what you normally earned before the crash. Combined with a profit and loss statement from your accounting software or your accountant, those returns give adjusters a clear picture of what your business was generating.

The records proving the specific loss matter just as much. Invoices for jobs you couldn’t complete show scheduled work you were forced to turn down. Signed contracts for postponed or canceled projects show anticipated income that didn’t materialize.

Bank statements confirm the pattern of regular deposits before the crash and the drop in income during your recovery.

One document self-employed riders often overlook is the physician’s statement. Your doctor should confirm the specific period your injuries prevented you from performing the essential tasks of your work.

That medical record is the link that connects your business documents to the crash. Without it, the insurer can argue the income drop had other causes.

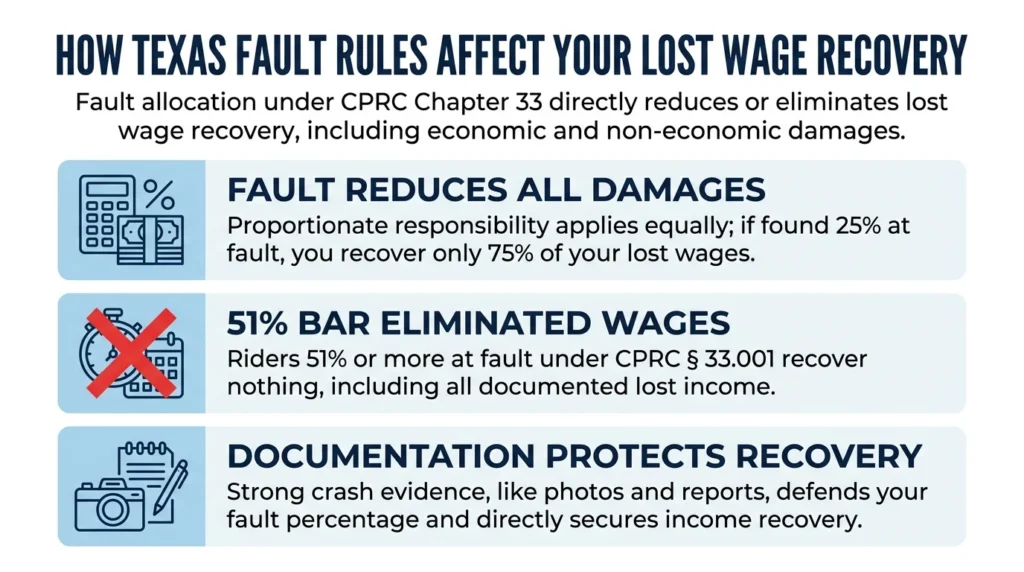

How Fault Affects Your Lost Wage Recovery

Texas uses a modified comparative fault system that can reduce or eliminate your recovery depending on your percentage of responsibility for the crash.

Under CPRC Chapter 33, if a jury finds you more than 50% responsible for the crash, you recover nothing. If your fault is 50% or below, your recovery is reduced by your percentage of responsibility. If you’re found 25% at fault for a crash that caused $80,000 in lost wages, you would receive $60,000.

Insurers know this, and they use it. Adjusters investigate whether you violated any traffic laws, were speeding, failed to use headlights, or made lane choices that contributed to the crash. Each factor can push your fault percentage higher.

The crash scene evidence, witness statements, and police report all feed directly into that fault calculation.

Texas motorcycle crash data shows that riders are often assigned fault at higher rates than other vehicle operators. Insurers also sometimes argue that not wearing a helmet contributed to injury severity, which can affect how damages are apportioned.

Your documentation of the crash itself matters as much as your income records. Both feed into the final settlement amount you recover.

Work with Angel Reyes & Associates on Your Claim

Proving lost wages after a motorcycle crash involves more moving parts than most riders expect. Documentation requirements differ between employed and self-employed riders. Future earning capacity claims require expert witnesses, and fault allocation can reduce your recovery if the insurer builds a stronger case.

Angel Reyes & Associates has aided Texas motorcycle accident victims for over 30 years, including motorcycle crash cases with complex income loss issues. We work on contingency, meaning you pay nothing unless we win. Our experienced attorneys can help you build the documentation needed for past wages and future earning capacity, and we stand with you through every step.

Reach out for a free consultation about your case.

Lost Wages FAQs

Does PIP insurance cover lost wages after a motorcycle accident in Texas?

Personal Injury Protection (PIP) can cover up to 80% of lost wages in Texas, but many motorcycle insurance policies do not include it automatically. If you did not add PIP to your motorcycle policy in writing, you may need to pursue lost wage recovery through the at-fault driver’s liability insurance instead.

Can I claim lost wages if the driver who hit me had no insurance?

Yes, if your own motorcycle insurance policy includes uninsured motorist (UM) coverage, that coverage can pay for lost wages when the at-fault driver has no liability insurance. UM/UIM coverage steps in as a substitute for the coverage the at-fault driver should have carried.

What if my employer won't provide a verification letter for my lost wages claim?

You can still document your lost wages without an employer letter by using pay stubs, W-2 forms, HR records, and bank statements that show your pre-crash income. An attorney can also send a formal written request or take other legal steps to compel your employer to cooperate.

Can I recover lost wages if I only work part-time or on a seasonal schedule?

Yes. Your lost wages calculation is based on the income you actually earned before the crash, not a full-time standard. Part-time and seasonal workers can use pay stubs, prior-year tax returns, and employer records to show their typical earnings and the income missed during recovery.

How soon after a motorcycle accident should I start documenting lost wages?

Start as soon as possible. Keep a log of every day you miss work, ask your employer for a written statement early in your recovery, and save all pay stubs and medical paperwork from the start. Early documentation creates a clear, dated record that is harder for an insurer to challenge later.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 55,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...