Collision vs Comprehensive vs Liability: A Practical Guide for Texas

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- Liability is the only coverage Texas requires, but 30/60/25 minimums may not be enough.

- Collision and comprehensive are optional unless your lender requires them for financing.

- Compare your car’s value to annual premiums to decide if optional coverage is worth it.

Collision vs Comprehensive vs Liability: A Practical Guide for Texas Drivers

If you were involved in an accident on I-35 or any other major roadway throughout the Lone Star State, you might be wondering how your insurance policy actually covers the damage. Insurance policies usually carry a few different kinds of insurance to cover different expenses.

Texas law requires liability insurance, but collision and comprehensive are optional unless your lender says otherwise. That distinction matters when you’re staring at a crumpled bumper or a hail-damaged hood. If you’re juggling work, family, and a damaged car, knowing which coverage applies saves you hours on the phone with adjusters.

Understanding the Core Coverages

Each type of auto insurance serves a different purpose. Knowing the basics helps you spot gaps before an accident forces you to find them.

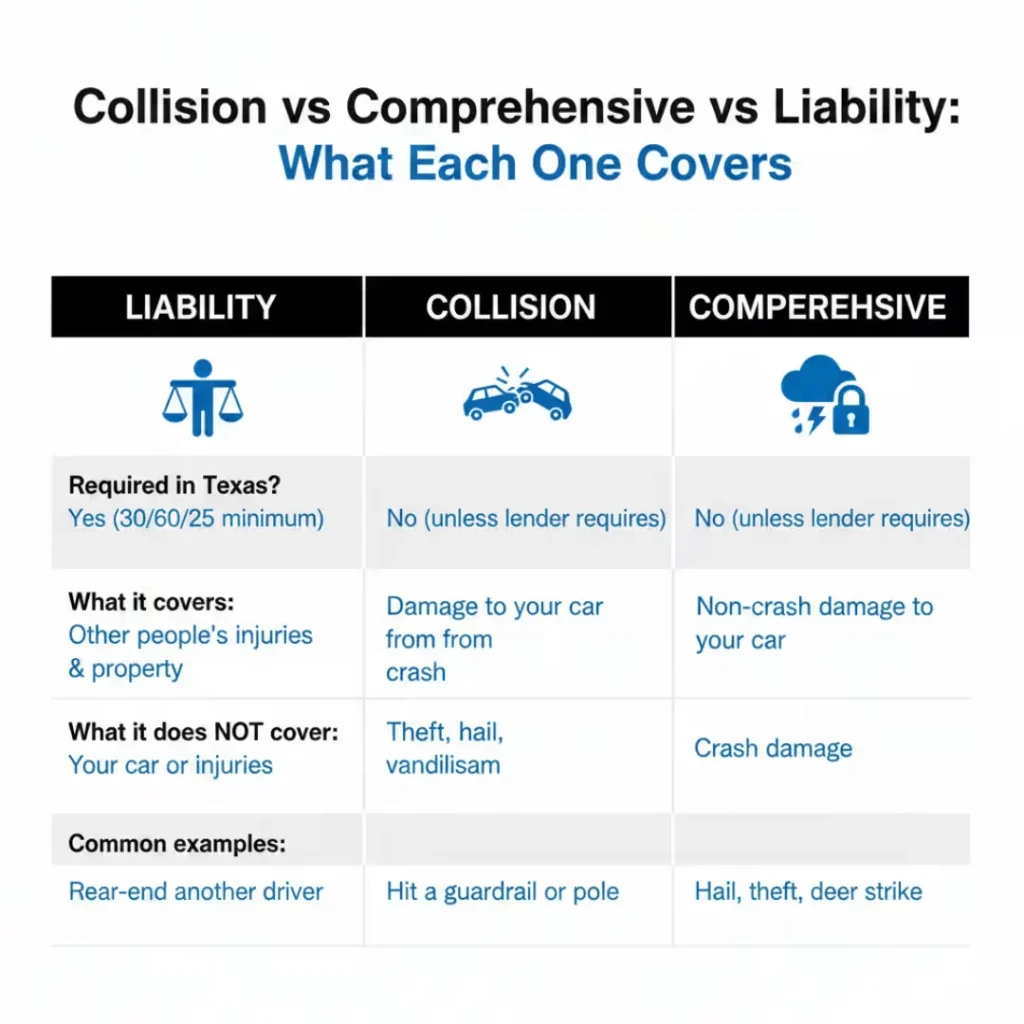

Liability coverage is the only auto insurance Texas requires. It pays for other people’s injuries and property damage when you’re at fault. Texas mandates minimum limits of 30/60/25. That means $30,000 per person for bodily injury, $60,000 total per accident, and $25,000 for property damage. Liability does not cover your own vehicle or injuries.

Collision coverage is optional unless your lender requires it. It pays to repair or replace your car after a crash, whether you hit another vehicle, a guardrail on 635, or a light pole in a parking lot.

Comprehensive coverage handles non-crash damage, such as hailstorms rolling through DFW, a stolen catalytic converter, a garage being broken into in San Antonio, or a deer strike on a rural highway in Bastrop County.

When & Why People Choose Each Coverage

“Adequate” coverage depends on your vehicle’s value, your loan terms, and how much risk you’re comfortable carrying.

Liability: How Much Is Enough?

The state minimum protects you legally, but it may not protect you financially. If you cause a serious accident, 30/60/25 limits can run out fast. That leaves you personally responsible for the rest. Many Texans carry 100/300/100 or higher, especially if they have assets to protect. The premium difference between minimum and higher limits is often smaller than people expect.

Collision & Comprehensive Coverage

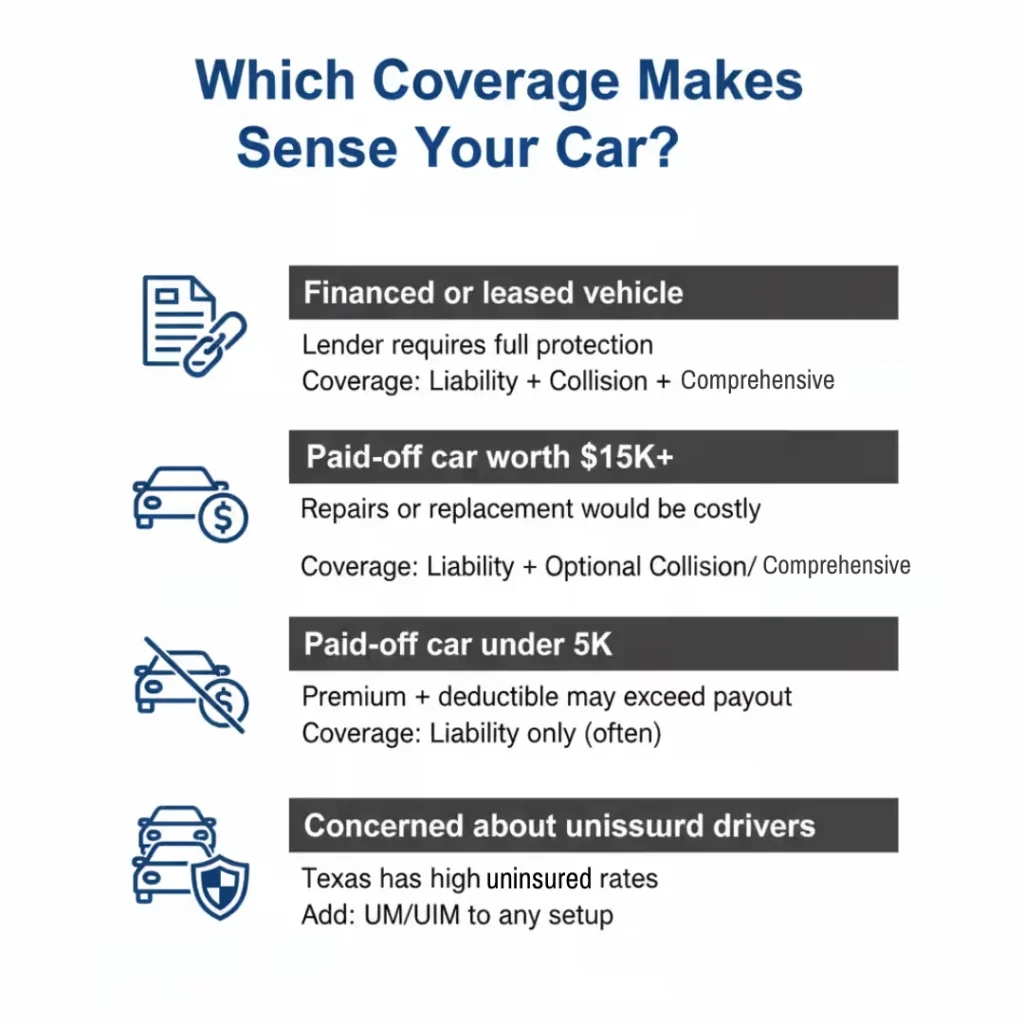

If you finance or lease your car, your lender almost certainly requires both collision and comprehensive coverage. Check your loan agreement to confirm.

If you own your car outright, the choice is yours. An older vehicle with low market value may not justify the premium. A newer car or one you depend on for work might be worth protecting.

Cost vs. Benefit: Weighing Premiums and Deductibles

Adding collision and comprehensive coverage will raise your premium. The amount depends on your vehicle, driving history, and chosen deductible.

A higher deductible lowers your monthly cost but increases what you pay out of pocket after a claim. A $1,000 deductible means you must cover the first $1,000 of repairs before insurance pays the rest.

For paid-off cars, compare your vehicle’s current value to the annual cost of coverage. If the premium plus your deductible approaches the car’s worth, you may want to drop collision and comprehensive coverage.

Choosing the Right Coverage for Your Situation

The right combination of coverage depends on what you’re driving and what you can afford to lose.

| Your Situation | Coverage You Need |

|---|---|

| Financed or leased vehicle | Liability + Collision + Comprehensive (lender requires it) |

| Paid-off car worth $15K+ | Liability required; collision/comprehensive often worth it |

| Paid-off car worth under $5K | Liability required; collision/comprehensive may cost more than payout |

| Concerned about uninsured drivers | Add UM/UIM to any of the above |

Questions to ask your insurer:

- What are my current deductibles for collision and comprehensive?

- Does my policy include gap coverage if my car is totaled?

- Am I carrying the state minimum liability, or higher limits?

Example Scenarios

Here are some example scenarios that show you when the right coverage is important.

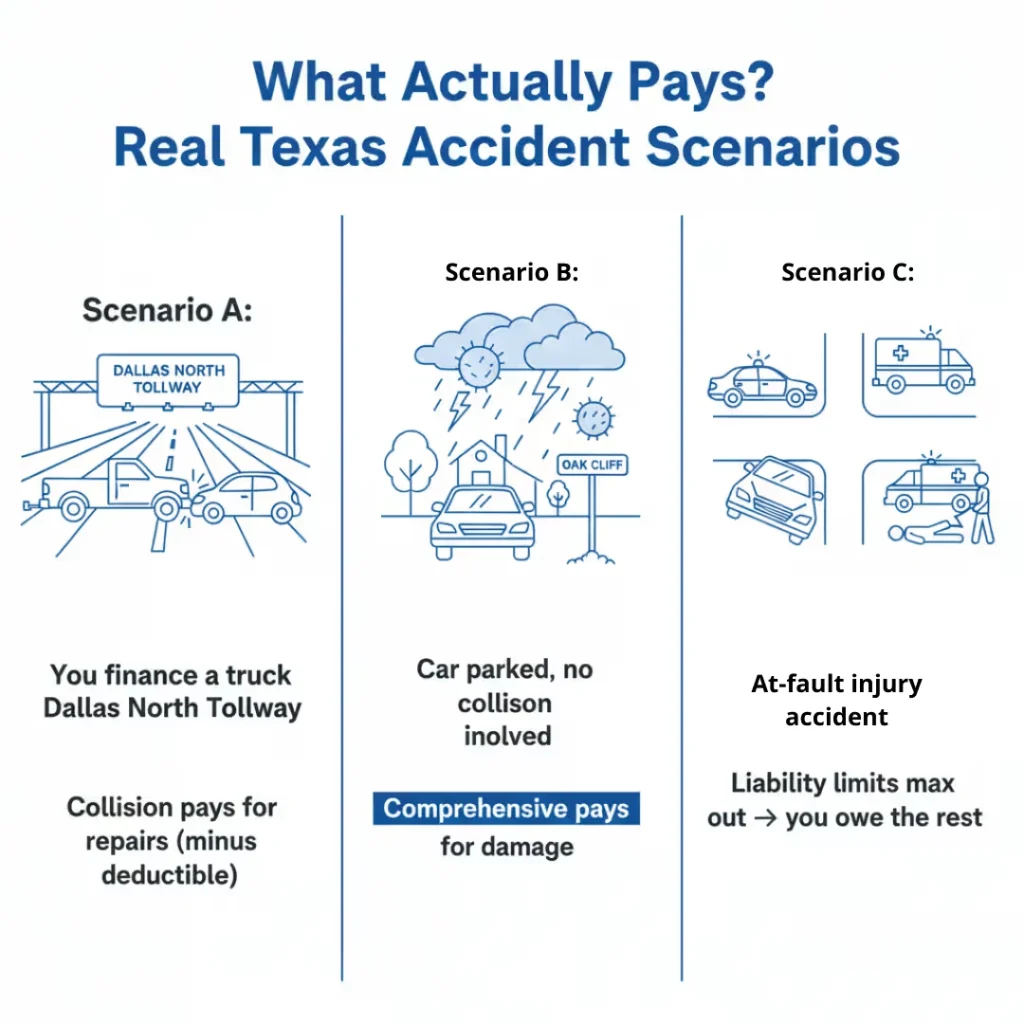

Scenario A: You finance a new truck and get sideswiped on the Dallas North Tollway. Collision coverage pays for your truck’s repairs, minus your deductible. You’re protected because your lender required this coverage.

Scenario B: A hailstorm damages your paid-off sedan while it’s parked at your home in Oak Cliff. Comprehensive coverage would cover the repairs. Without this coverage, you’d pay the full cost yourself.

Scenario C: You miss a red light and cause a wreck that injures two people. Their medical bills exceed your 30/60/25 liability policy limits. You would be personally liable for the difference, while higher policy limits likely would have covered the gap.

Insurance Coverage FAQs

What happens if my car is financed and I drop collision or comprehensive coverage?

If your car is financed, your lender almost certainly requires collision coverage as a condition of the loan. Dropping it without permission can trigger forced-placed insurance at a higher cost, so review your financing agreement or call your lender to confirm.

What does “full coverage” actually include?

“Full coverage” isn’t a legal term, so it varies. In practice, it usually means a policy with liability plus collision and comprehensive. Some policies also include UM/UIM, PIP, or rental reimbursement.

What if someone else causes an accident I am involved in?

If someone else causes your accident, their liability coverage should be responsible for paying for your vehicle damage and medical bills. If the driver is uninsured or underinsured, your own UM/UIM coverage fills the gap. Collision and comprehensive coverage protect your car, and PIP coverage helps with medical bills regardless of fault.

Know Your Coverage Before You Need It

The best time to understand your policy is before you’re involved in an accident. Review your declarations page, confirm your deductibles, and decide whether your liability limits match your financial reality. If you’ve already been in an accident and the coverage picture is unclear, call our team at Angel Reyes & Associates. We have guided Texans through situations like this for over 30 years and offer free consultations to review your options.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 70,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Graham Griffin

Editor

Graham Griffin is the editorial director responsible for accuracy and legal compliance across all firm content.

Graham Griffin

Reviewer

Graham Griffin also serves as legal reviewer, ensuring all claims and advice reflect current Texas statutes and case law.