How to Choose a Car Insurance Deductible in Texas

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- Calculate your break-even point by dividing annual premium savings by the deductible increase to see how many claim-free years would justify the higher deductible.

- Texas UMPD coverage commonly carries a $250 deductible, which may provide a lower out-of-pocket option after crashes with uninsured drivers.

- Financed vehicles require collision and comprehensive coverage, but you can often optimize costs by choosing different deductibles for each, based on local risks.

You just renewed your auto policy in Fort Worth, and your agent asked whether you want to raise your deductible from $500 to $1,000. The premium savings can sound tempting, but you’re also thinking about that hailstorm last spring, and the fender-bender on I-30 two years ago. How do you know which deductible actually makes sense for your situation?

Choosing the right deductible isn’t about finding a magic number. It’s about matching your budget, your vehicle, and your real-world driving risks to a coverage structure that protects you without draining your wallet.

The Purpose of a Deductible in Texas Auto Claims

A deductible is the amount of money you pay out of pocket before your insurance covers the rest of a claim. For example, if you have a $1,000 deductible, and your repair bill is $4,500, you will pay $1,000, and your insurer pays $3,500.

In Texas, deductibles typically apply per claim, rather than annually. That means if you file two separate collision claims in the same year, you pay your deductible twice. The Texas Department of Insurance explains this distinction clearly.

One common misconception is that if you’re not at fault, you won’t have to pay a deductible. That’s not always true. If you use your own collision coverage to get repairs done quickly, you’ll have to pay your deductible upfront. Your insurer may later recover that amount from the at-fault driver’s insurance through a process called “subrogation,” but recovery isn’t guaranteed, and it will take some time.

The basic tradeoff is pretty simple. Higher deductibles generally mean lower premiums. When you agree to absorb more risk yourself, the insurer charges you less. According to TDI, switching from a $500 to a $1,000 deductible can lower premiums a significant amount, but the exact savings will vary by driver, vehicle, and ZIP code.

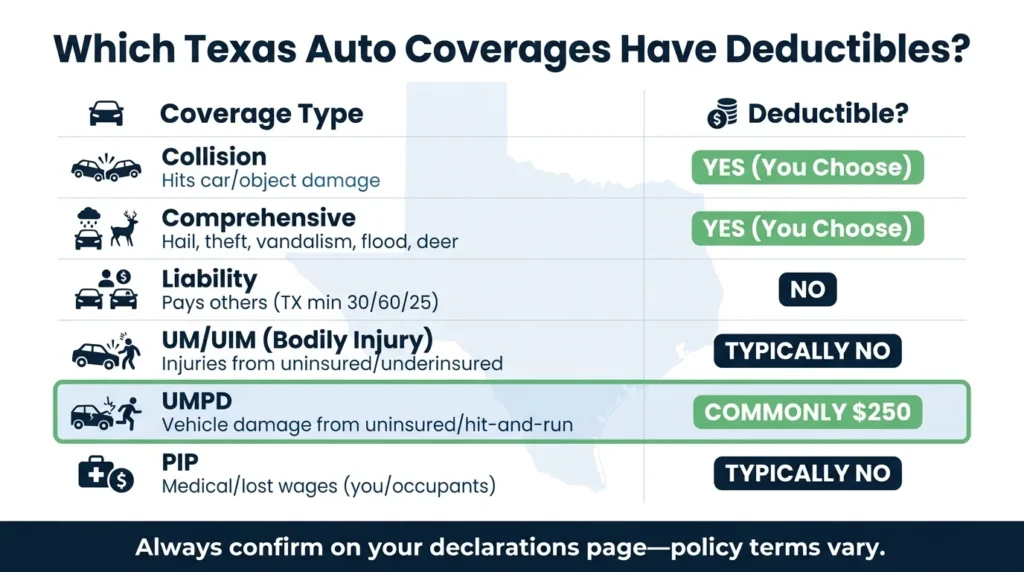

Which Coverages Have Deductibles in Texas

Not every coverage on your policy includes a deductible. Understanding which types of coverage include deductibles can help you make smarter choices.

Collision coverage pays for damage when your car hits another vehicle or object. This coverage allows you to select the deductible.

Comprehensive coverage pays for non-collision losses, such as hail, theft, vandalism, flooding, or hitting a deer. This also has a deductible, and you can often choose a different amount than your collision deductible.

Liability coverage pays others when you cause a crash. It generally doesn’t have a deductible because it covers the other party’s losses, not yours. Texas requires minimum liability limits of 30/60/25 ($30,000 per person for bodily injury, $60,000 per accident, $25,000 for property damage) under Texas Transportation Code § 601.072.

Uninsured/underinsured motorist (UM/UIM) coverage and personal injury protection (PIP) have their own rules. Texas insurers must offer both, and you can only decline them by rejecting them in writing under Texas Insurance Code Chapter 1952.

These coverages interact with deductibles in important ways after a crash. The Office of Public Insurance Counsel provides helpful explanations of how these coverages work together.

The $250 UMPD Deductible in Texas

If an uninsured driver hits you, or you’re the victim of a hit-and-run, uninsured motorist property damage (UMPD) coverage can help pay for repairs. Texas guidance commonly cites a $250 deductible for UMPD claims when this coverage applies.

This is different from your collision deductible. If you have both types of coverage, and an uninsured driver damages your car, you may have options for which coverage to use. The TDI’s UM/UIM guide explains how this coverage works, and why documentation is so important.

Check your declarations page. Not every policy includes UMPD, and terms may vary. Be sure to confirm whether you have this coverage and what deductible applies.

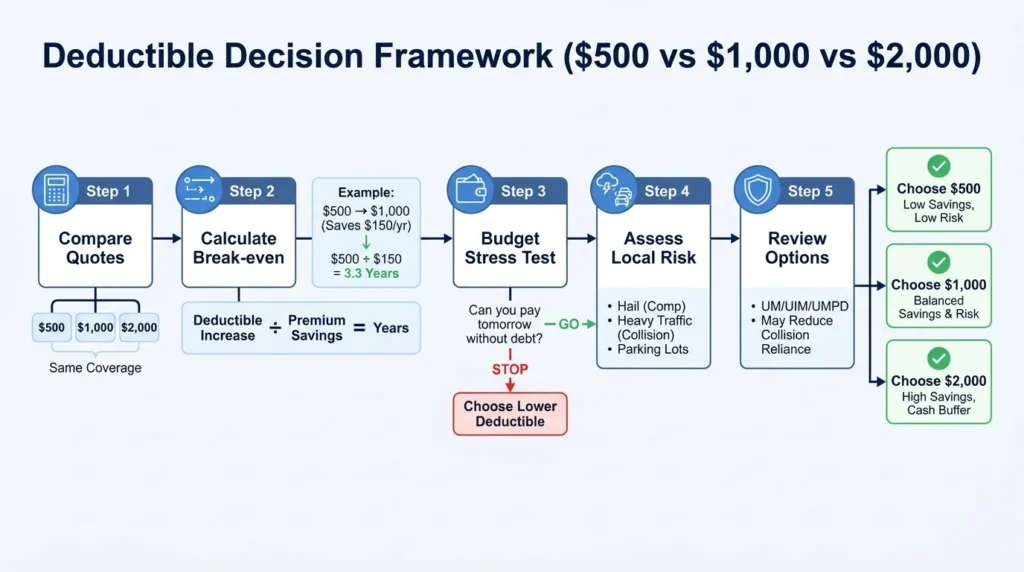

A Step-by-Step Guide to Deciding on a Deductible ($500 vs $1,000 vs $2,000)

Rather than relying on guesswork, use this method to make a decision based on actual numbers.

Step 1: Get comparison quotes. Ask your insurer for premium quotes at $500, $1,000, and $2,000 deductibles for both collision and comprehensive coverage. Keep your other insurance coverage the same.

Step 2: Calculate your break-even point. Divide your annual premium savings by the deductible increase. If raising your deductible from $500 to $1,000 saves you $150 per year, you’ll need about 3.3 claim-free years to come out ahead ($500 ÷ $150 = 3.3 years).

Step 3: Stress-test your budget. Could you pay the higher deductible tomorrow without using a credit card or dipping into rent money? If not, the premium savings aren’t worth the financial strain after a loss.

Step 4: Factor in local risks. In the DFW area, hail season creates real comprehensive claim exposure. Heavy traffic on I-35W, I-30, and Loop 820 increases collision risk for daily commuters. Parking lot damage in busy areas like Sundance Square or the Stockyards makes things even more complicated.

Step 5: Consider your other types of coverage. If you have strong UM/UIM coverage, you may have options beyond collision after a not-at-fault crash. This can affect how much you rely on your collision deductible.

When Raising Your Deductible Makes Sense

A higher deductible often works well when:

- Premium savings are substantial (run the break-even calculation to be sure).

- You have an emergency fund that can cover the deductible.

- Your vehicle has higher value, which makes comprehensive and collision coverage worth keeping.

- You have a clean driving history and lower claim frequency.

A lower deductible often makes more sense when:

- Premium savings are minimal.

- Cash flow is tight.

- You park outside in hail-prone areas.

- You’ve had multiple small claims in recent years.

Financed vs Paid-Off Vehicles: Different Strategies

Your ownership situation changes your options.

If your car is financed or leased, your lender almost certainly requires collision and comprehensive coverage. You can’t drop these types of coverage to save money. In this case, your strategy should focus on optimizing your deductible levels within these required types of coverage.

Consider setting your comprehensive deductible lower than your collision deductible if hail or theft is a bigger concern than crashes. This split-deductible approach can balance premium costs against your most likely claim types.

Also, be sure to confirm whether your lender sets a maximum deductible. Some financing agreements cap deductibles at $500 or $1,000.

If your car is paid off, you have more flexibility. Eventually, keeping collision coverage on an older car may not be worth the cost. Compare your annual collision premium plus your deductible against your car’s actual market value. If you’re paying $800 per year in collision premium with a $1,000 deductible on a car worth $4,000, you’re spending a significant percentage of the car’s value on coverage.

That said, comprehensive coverage can still make sense, even on older vehicles, considering that a single hailstorm can total a car. To decide, compare the premium cost to how hard the vehicle would be to replace.

Remember: Raising your deductible is different from reducing your liability limits. Saving money on premiums is tempting, but reducing or eliminating your liability coverage can leave you underprotected after a major crash. The minimum 30/60/25 limits may not be enough after a serious crash, and the financial consequences of being underinsured may cost you far more than your deductible.

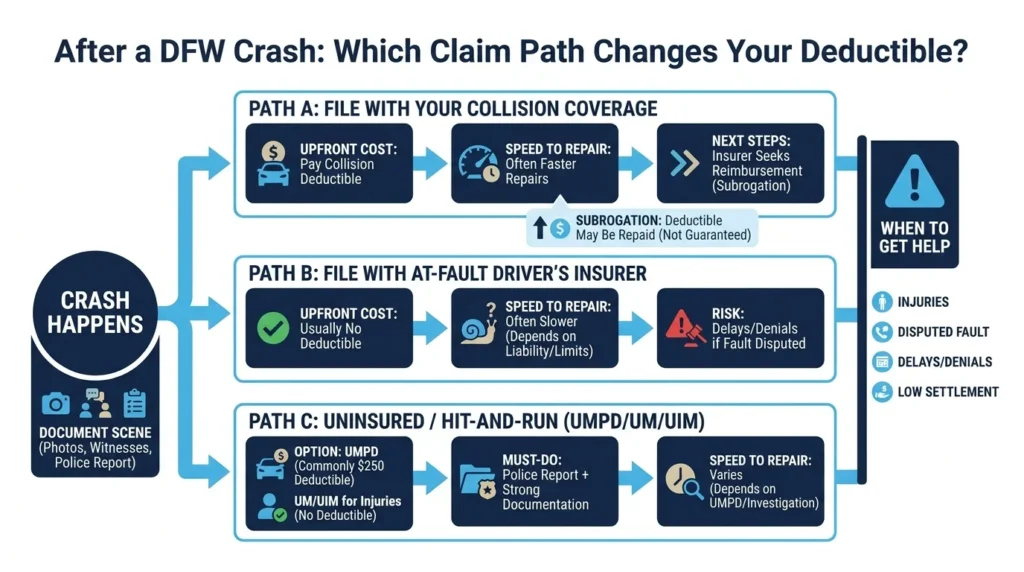

What Happens After a Crash

Understanding how deductibles work in real claims can help you plan ahead. Here are two different scenarios that may occur after a crash:

Scenario 1: You file a claim with your own collision coverage. You pay your deductible, get your repairs done, and your insurer pursues the at-fault driver’s insurance for reimbursement. This is often a faster process, but it requires upfront payment on your part.

Scenario 2: You file a claim directly with the at-fault driver’s insurer. You may avoid paying a deductible, but the process typically takes longer and depends on whether the other driver has adequate coverage or not.

For hit-and-run crashes or collisions with uninsured drivers, your UM/UIM and UMPD coverages become critical. Report these incidents to the police right away. Document everything, including photos of the damage, witness contact information, the police report number, and repair estimates.

If the at-fault driver’s insurer disputes liability, delays your claim, or offers a settlement that doesn’t cover your losses, the situation becomes more complex. When injuries are involved, speak with an attorney before accepting any offer to protect your interests.

How to Lower Premiums Without Raising Deductibles

If you want to save on your premiums but can’t afford a higher deductible, here are some other options you can explore:

- Ask about discounts for bundling home and auto policies.

- Inquire about safe driver or defensive driving course discounts.

- Consider usage-based insurance programs if you drive fewer miles.

- Pay your premium in full, rather than in monthly installments.

- Shop quotes from multiple insurers.

Credit-based insurance scores can also affect your rates in Texas. Improving your credit may lower your premiums over time.

You can also review optional types of coverage, like rental reimbursement and roadside assistance. These add-ons have value, but if you already have other ways of covering these needs, then removing them may lower your costs without increasing your deductible risk.

When to Talk to an Attorney

Deductible decisions are primarily financial planning questions, but after a crash, the financial impact goes beyond your deductible.

Consider getting legal help when:

- You have injuries requiring medical treatment.

- The insurance company disputes who was at fault.

- You’re dealing with a commercial truck or multiple vehicles.

- The adjuster pressures you to give a recorded statement or accept a quick settlement.

- Your claim is delayed or denied without a clear explanation.

- The at-fault driver was uninsured or underinsured.

Insurance companies are businesses. Their goal is to resolve claims efficiently, which often means doing so for the lowest reasonable payout. That’s not malicious; it’s their business model, but it also means your interests don’t always align with theirs.

At Angel Reyes & Associates, we’ve spent over 30 years helping Texas drivers navigate insurance claims and injury cases. We offer free consultations, and you pay nothing unless we win. Our team has recovered more than $1 billion for clients across the state.

If you’ve been in a crash, and you’re unsure whether your insurance company is treating you fairly, reach out to us today. We can review your situation and help you understand your options.

Insurance Deductible FAQs

Can you change your car insurance deductible at any time in Texas?

Usually, yes, but the new deductible generally applies only after the change takes effect, and it does not apply to a loss that has already happened. If you have a loan or lease, your lender may also need the updated policy to stay within its deductible limit.

Does deductible choice affect a total loss claim in Texas?

Yes. If your car is declared a total loss, and your policy includes a deductible for that coverage, the insurer typically subtracts that amount from the payout.

Is there a deductible for bodily injury claims under UM/UIM in Texas?

Typically, not for uninsured or underinsured motorist bodily injury claims. The $250 deductible usually refers to uninsured motorist property damage, not injury payments. The terms of your policy still determine the details of your coverage.

Will gap insurance pay my deductible if I still owe money on my car?

Not always. Gap coverage is designed to cover certain differences between what you owe and the vehicle’s actual cash value after a total loss, but whether it covers a deductible depends on the terms of your contract.

Should an older car have the same deductible as a newer car?

Not necessarily. On an older car, a very high deductible can make coverage less useful because you may end up paying most of the smaller repair costs before your insurance contributes.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 70,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...