How Credit Scores Impact Car Insurance Rates in Texas

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- Texas insurers use credit-based scores to set your premium, and poor credit often means higher rates.

- State law limits how insurers use credit and requires re-checks if your score improves at renewal.

- Disputing errors, paying down debt, and shopping insurers can lower what you pay for coverage.

How Credit Scores Affect Car Insurance Rates in Texas

You just opened your auto insurance renewal and the premium jumped again. In Texas, your credit history is one of the biggest factors insurers use to set your rate.

That surprises many drivers. You might assume your driving record matters most. It does matter. But Texas law allows insurers to weigh your credit-based insurance score heavily when calculating what you pay.

If you have strong credit, you likely pay less. If your credit took a hit from medical bills, a divorce, or job loss, your premium can climb by hundreds of dollars a year.

Understanding how this works puts you in a better position to manage costs and protect yourself after an accident.

How Texas Insurers Use Your Credit History

Texas insurers pull a credit-based insurance score when you apply for coverage or renew a policy. This score is different from the FICO score a lender sees. It focuses on patterns that insurers believe predict the likelihood of filing a claim.

If you’re juggling work, bills, and school pickups, you don’t have time to decode insurance scoring models. Here’s what actually affects your rate.

Under Texas Insurance Code Chapter 559, insurers must file their credit-scoring models with the Texas Department of Insurance (TDI). They cannot use your income, employment history, or marital status as direct factors.

They also cannot penalize you solely for having no credit history.

What they can consider includes:

- Payment history on credit accounts

- Outstanding debt relative to available credit

- Length of credit history

- Types of credit you use

- Recent credit inquiries

Insurers assign more weight to some factors than others. Payment history and credit utilization typically matter most.

A driver with a thin credit file or past collections may see a higher quote than someone with years of on-time payments. Industry data suggests drivers with poor credit often pay noticeably more than those with excellent credit for the same coverage in Texas.

If you live in the DFW area and commute on I-35E or LBJ 635, you already face higher base rates due to traffic density and accident frequency. A lower credit score on top of that can push your premium even higher.

What Texas Law Protects You From

Texas has rules limiting how insurers can use credit information. TDI requires insurers to re-check your credit at renewal if doing so would lower your premium.

You can also request a re-evaluation if your credit has improved.

Insurers cannot:

- Use credit as the sole reason to deny, cancel, or non-renew a policy

- Consider medical debt that appears in collections

- Penalize you for credit inquiries related to shopping for insurance, a mortgage, or an auto loan within a short window

- Factor in your race, religion, national origin, or neighborhood income level

If you believe an insurer violated these rules, you can file a complaint with TDI. You also have the right to ask your insurer which credit factors affected your rate and to dispute errors on your credit report directly with the credit bureaus.

One dispute letter to a credit bureau can correct a billing error or remove old medical debt that’s dragging down your score. With that fix you could easily see a lower insurance premium at your next renewal.

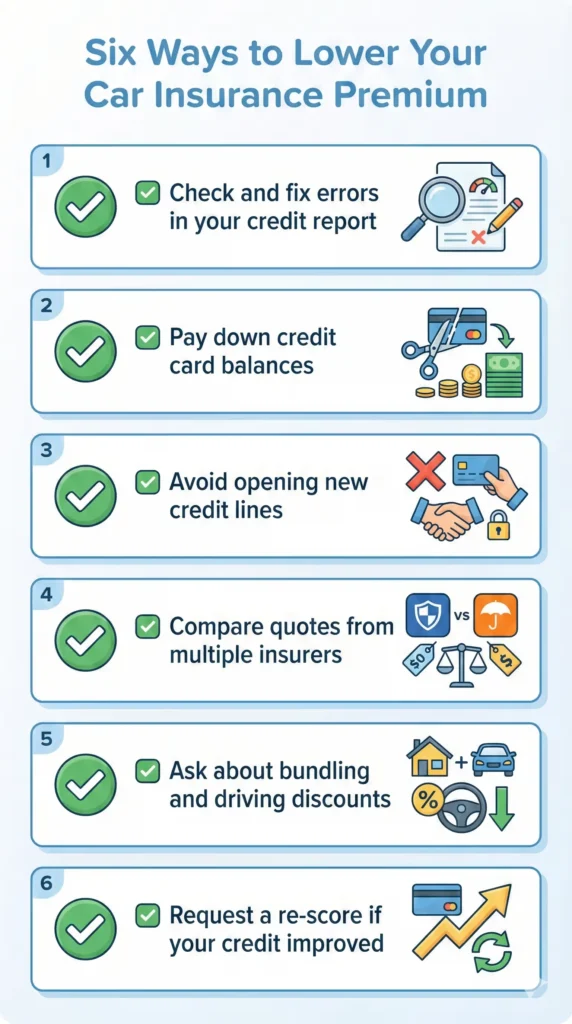

Practical Steps to Manage Your Premium

Six steps can lower your premium without cutting coverage.

These take time, but for a driver in Houston dealing with 610 Loop traffic and already paying elevated urban rates, even a modest credit improvement can translate into real savings.

- Check your credit reports for errors. You can get free reports from Equifax, Experian, and TransUnion at AnnualCreditReport.com. Dispute inaccuracies in writing.

- Pay down revolving balances. Lowering your credit utilization ratio often improves your score within a few billing cycles.

- Avoid opening unnecessary new accounts. Each hard inquiry (a credit check that can temporarily lower your score) adds up.

- Shop multiple insurers. Credit-scoring models vary. One company may rate your history more favorably than another. Get at least three quotes before renewing.

- Ask about discounts. Bundling home and auto, completing a defensive driving course, or using a telematics device (a plug-in or app that tracks your driving habits) can offset some of the credit-related increase.

- Request a re-score at renewal. If your credit improved since your last policy term, ask your insurer to pull a fresh score before they finalize your rate.

How Driving Records and Credit Interact

Insurers weigh your credit alongside your driving record, claims history, vehicle type, and where you park overnight.

A clean driving record helps, but it may not fully offset poor credit. Strong credit can reduce the rate increase if you have a minor at-fault accident on your record.

In Texas, most accidents and violations stay on your driving record for three to five years. During that window, both your record and your credit score influence what you pay.

But here’s where it gets frustrating: an accident you didn’t cause can still hurt your finances in ways that raise your insurance costs.

If you were injured in a crash caused by another driver, the at-fault driver’s insurer should cover your damages. Your own rates should not increase for an accident that wasn’t your fault, though some insurers still factor claims into their models.

The real problem is what happens next. If you were hurt in a wreck and are dealing with medical bills, lost wages, or vehicle repairs, those financial pressures can affect your credit.

Late payments or new debt from an accident you did not cause can drag your credit score down. Next thing you know your insurance premium goes up just when you can least afford it.

When to Talk to a Texas Personal Injury Attorney

If an accident you didn’t cause is threatening your credit and your insurance rates, getting fair compensation faster can break that cycle.

Insurance companies have teams dedicated to minimizing what they pay. If you were injured in an accident caused by someone else, you deserve fair compensation for medical expenses, lost income, and pain and suffering. Recovering what you’re owed helps you pay bills on time, avoid collections, and protect the credit score that affects what you pay for insurance.

We’ve guided Texans through situations like this for over 30 years. A free consultation can help you understand your options and whether pursuing a claim makes sense for your situation.

Credit Scores and Insurance FAQs

Can an insurer deny me coverage in Texas just because of my credit score?

No, an insurer cannot deny you coverage in Texas based solely on your credit score. Texas law prohibits insurers from using credit as the sole reason to deny, cancel, or non-renew a policy. They must consider other factors as well.

Will shopping for insurance quotes hurt my credit?

Shopping for insurance quotes will not significantly hurt your credit. Multiple insurance inquiries within a short period are typically grouped together and have minimal impact on your score. The same applies to mortgage and auto loan shopping.

How often can I ask my insurer to re-check my credit?

You can ask your insurer to re-check your credit at any renewal. If your credit has improved, the insurer must use the new score if it results in a lower premium. See “What Texas Law Protects You From” above for more on your rights.

Does paying off collections immediately raise my score?

Paying off collections does not always immediately raise your score. The impact depends on the scoring model your insurer uses. Some newer models ignore paid collections entirely. Others still factor them in. Paying off debt is generally positive, but the timing of score improvement varies.

What if my credit suffered because of accident-related medical bills?

If your credit suffered because of accident-related medical bills, Texas law offers some protection. Medical debt in collections cannot be used against you under Texas insurance credit-scoring rules. If you see it affecting your rate, file a complaint with TDI and dispute the entry with the credit bureaus.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 70,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Graham Griffin

Editor

Graham Griffin is the Web & Content Manager at Angel Reyes & Associates, where he oversees content strategy, AI-powered workflows, a...

Spencer Browne

Reviewer

Spencer Browne is a partner at Angel Reyes & Associates and a Board Certified personal injury trial lawyer with nearly 100 jury trials a...