Insurance Coverage for Rental Cars After a Crash in Texas

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- Multiple insurance sources may apply after a rental car crash in Texas, but insurers often dispute who pays first, making documentation critical.

- Rental companies will usually pursue your personal insurance policy first, even if you aren’t at fault. Ask about purchasing a damage waiver if you want to avoid this.

- The Graves Amendment generally protects rental companies from liability, shifting focus to the at-fault driver’s insurance and your own coverage options.

Insurance Coverage for Rental Cars After a Crash in Texas

You picked up a rental car at Austin-Bergstrom International Airport yesterday for a weekend trip to see family. On your way down Congress Avenue, another driver ran a red light and slammed into your passenger side.

Now you’re dealing with a damaged rental, a stack of paperwork, and calls from multiple insurance companies. Each one seems to think someone else should pay.

Rental car crashes create a unique problem. Several insurance sources might apply to your situation, but they rarely agree on who pays first. Your personal auto policy, the other driver’s liability insurance, your credit card benefits, and even the rental company’s damage waiver could all play a role. Understanding how insurance works for rental cars under Texas law can help you avoid gaps and maintain your ability to collect compensation should you be injured.

How Are Rental Cars Insured in Texas?

When you get behind the wheel of a rental car, you are generally assumed to be an insured driver with coverage that would protect you and others in the event of an accident. Texas Transportation Code § 601.072 mandates that every driver carry liability insurance of at least 30/60/25. That means $30,000 per person, $60,000 per incident, and $25,000 in personal property damage.

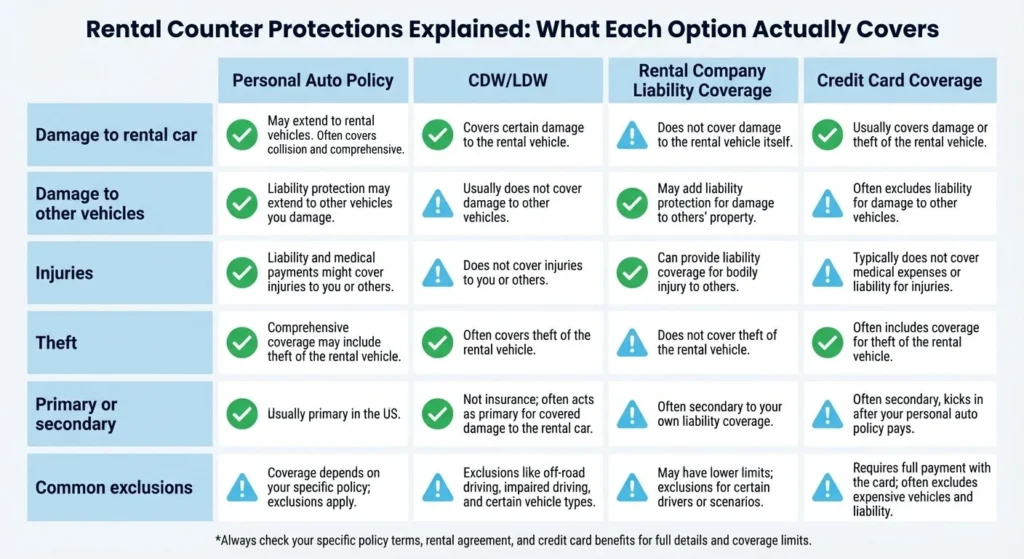

However, your own personal liability does not cover damage to a rental car that you’re driving. Your own existing car insurance policy likely extends to rental or borrowed vehicles, though check your own declarations page before renting to make sure.

Should your coverage transfer, your rental would be protected by your own collision or comprehensive coverage. Rental reimbursement coverage is not protection for rental cars—it covers the cost of a rental vehicle while your vehicle is being repaired after an accident.

Because your own coverage is primarily responsible for protecting their vehicle, most rental car companies will ask you for proof of insurance when you’re filling out your paperwork. They may refuse to rent to you if you do not have adequate coverage unless you also purchase their supplemental protection.

Protection Offered by Rental Companies

Before you take your car off the rental lot, an agent will likely go over available “coverages” or “protections” they offer to renters. These can vary from company to company, but most offer the option for at least the following:

- Damage waiver

- Liability coverage

- Roadside assistance

Rental Company CDW & LDW

The collision damage waiver (CDW) or loss damage waiver (LDW) you’re offered at the rental counter is not insurance. It’s a contractual agreement where the rental company foregoes its right to charge you for certain damage to the vehicle.

CDW and LDW typically cover:

- Damage to the rental vehicle from a collision

- Theft of the rental vehicle

- Vandalism

They typically do not cover:

- Your injuries or medical bills

- Damage to other vehicles or property

- Injuries to other people

- Certain vehicle types or uses (trucks, off-road driving)

CDW/LDW is not a get-away-free excuse to abuse rental cars—companies have restrictions on what they will and won’t honor the agreement for. For example, taking a car off-road is usually forbidden due to the risk involved, and the protection is also usually nullified if you take your car out of the country (something important for our South Texas communities).

Even with CDW/LDW, the rental company may still bill you for loss-of-use fees (the income they lost while the car was being repaired) and administrative charges. Ask about these fees before you sign the rental agreement.

Liability Coverage

If you purchase liability coverage from your rental provider, this is a type of insurance, but it is usually set up to be secondary to your own liability insurance. In other words, if you only have minimum liability insurance, purchasing the rental car’s additional liability coverage can extend the amount of available coverage you have. Your own liability coverage will cover you first, but you (and any other third parties) can then make a claim on the rental company’s liability policy to fill in any remaining losses.

What About My Credit Card Rental Coverage?

Many credit cards offer rental car damage benefits. This coverage usually applies to damage or theft of the rental vehicle itself.

Most credit card coverage is secondary. This means your personal auto insurance pays first, and the credit card benefit covers what’s left (like your deductible). Some premium cards offer primary coverage that pays before your auto policy, but this is rare. Check with your card issuer first.

Credit card benefits typically do not cover:

- Liability for injuries to others

- Damage to other vehicles

- Rentals longer than 15-31 days (varies by card)

- Certain vehicle types (trucks, luxury cars, SUVs in some cases)

To use credit card coverage, you usually must decline the rental company’s CDW/LDW and pay for the entire rental with that card. You’ll need to file a claim promptly with documentation, including the rental agreement, police report, and repair estimates.

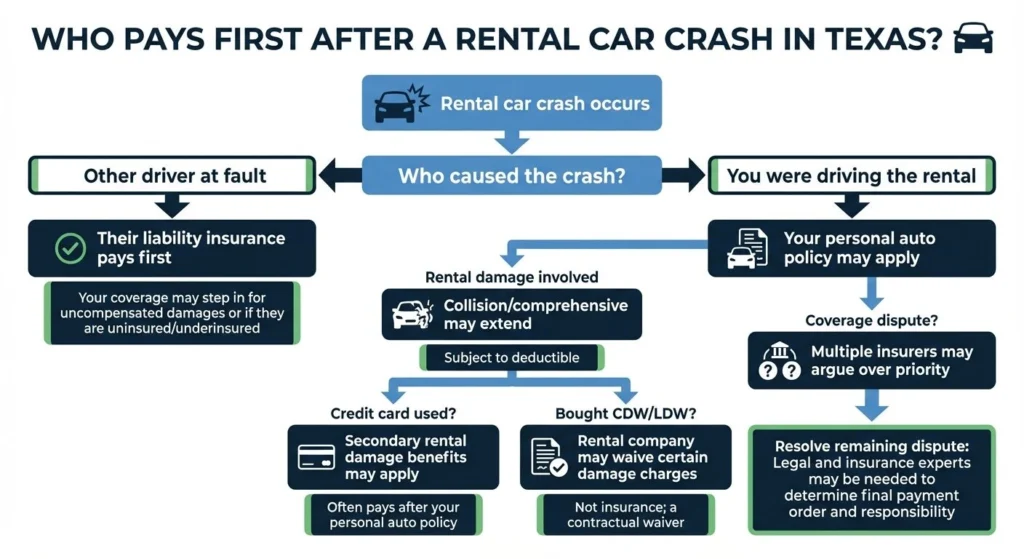

What Policy to Pursue in a Rental Car Accident

If you are involved in an accident with another motorist who is driving a rental car, you might be wondering how to proceed with your claim. Which policy do you file your claim against? What policy will cover your various losses in this accident?

- If the other driver is at fault, their own liability insurance will be the first policy you turn to. This will cover damage to your vehicle, any injuries you have sustained, and any other property damage you have suffered.

- If the other driver’s liability coverage runs out, any supplemental liability they may have purchased from the rental company, or that they may have from a credit card comes next.

- If fault is disputed, you may wish to file a claim with your own insurance policy to get your vehicle’s repairs started. Your own insurer can pursue the claim while your vehicle is fixed and then be made whole through subrogation.

How Texas Fault Rules Affect Your Rental Claim

Texas uses a fault-based insurance system. The driver who caused the crash is generally responsible for damages, but their percentage of fault influences how much the other parties may be able to collect.

Under Texas Civil Practice and Remedies Code § 33.001, if you’re found more than 50% responsible for the crash, you cannot recover damages from the other driver. If you share some fault but stay at 50% or below, your recovery gets reduced by your percentage of responsibility.

The Graves Amendment & Rental Company Liability

Many people assume the rental company shares responsibility in an accident because it owns the vehicle. Federal law generally says otherwise.

The Graves Amendment (49 U.S. Code § 30106) protects rental companies from vicarious liability. This means you typically cannot sue rental company just because it owned the car that hit you. The only exception to this rule is if the rental company was independently negligent, meaning they rented a car with known issues that prevent it from operating safely. However, this requires proof, and collecting evidence that shows this can be difficult.

Usually, the focus in a rental car accident shifts to the at-fault driver and their insurance.

Common Billing Items that Create Disputes

After a rental car crash, you may receive bills for charges beyond the repair costs:

- Loss-of-use fees compensate the rental company for lost rental income while the vehicle was being repaired. These fees can add up quickly. Request documentation showing the daily rate, repair timeline, and fleet utilization.

- Administrative fees cover the rental company’s paperwork and claims processing. These typically range from $50 to $150 but can be higher.

- Diminished value claims argue the vehicle is worth less after being repaired than it was before the crash. Rental companies sometimes pursue these against at-fault drivers.

If you receive a bill demanding immediate payment, request an itemized breakdown with supporting documentation. Don’t ignore deadlines, but don’t pay disputed charges without understanding what you’re paying for.

When to Get Legal Help

Some rental car claims resolve smoothly. Others become complicated when insurers point fingers at each other or dispute liability.

Consider speaking with a Texas car accident attorney if:

- Multiple insurers deny coverage or claim someone else should pay

- The at-fault driver has minimum limits that won’t cover your losses

- You’re being blamed for a crash you didn’t cause

- The rental company is pursuing you for disputed fees

Angel Reyes & Associates has helped Texas drivers navigate insurance disputes for over 30 years. We are an experienced team of advocates offering qualified advice and representation to help in the aftermath of an accident.

We offer free consultations and work on contingency, meaning no fee unless we win. Contact us to discuss your rental car crash and understand your options.

Rental Car Accident FAQs

Does my PIP or MedPay policy cover me in a rental car crash?

Often, yes. If your Texas auto policy includes Personal Injury Protection or Medical Payments coverage, it may help pay injury-related costs if you were driving a rental, depending on your policy terms.

Can the rental car company pursue me if I decline coverage and am involved in an accident?

Yes. The rental company will almost certainly file a claim against your policy for the damage to the vehicle, even if you were not at fault. They will also usually collect your deductible payment from you directly.

If you weren’t at fault, they will generally leave it up to your insurance company to pursue the at-fault driver on your behalf.

Will uninsured motorist coverage help if the driver who hit my rental car has no insurance or flees the scene?

It may. In Texas, uninsured or underinsured motorist coverage can help with certain losses after an uninsured driver or hit-and-run crash. Verify in your policy disclosures that UM/UIM coverage transfers to rental vehicles.

Can a rental company deny my CDW/LDW and other coverages if someone not listed on the agreement was driving?

Yes. Rental contracts are legally binding, and the terms of the purchased coverages hinge on the insurance company screening and documenting drivers who will be operating the vehicle. If a driver not listed on the contract was in control of the vehicle at the time of the accident, contract terms usually render the purchased coverages void.

Do I need to notify the rental company right away after an accident?

Usually yes. Prompt notice can help protect your claim and reduce disputes over damage, fees, or missing documentation.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 55,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Graham Griffin

Editor

Graham Griffin is the Web & Content Manager at Angel Reyes & Associates, where he oversees content strategy, AI-powered workflows, a...

Spencer Browne

Reviewer

Spencer Browne is a partner at Angel Reyes & Associates and a Board Certified personal injury trial lawyer with nearly 100 jury trials a...