How to File a Commercial Vehicle Insurance Claim in Texas

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- Commercial claims face higher policy limits and aggressive adjusters, so thorough documentation is essential.

- Texas Insurance Code Chapter 542 requires acknowledgment within 15 calendar days and payment within 5 business days of acceptance.

- Texas gives most injury claimants two years from the crash date to file under CPRC § 16.003.

You were headed back to Pasadena on I-10 when an 18-wheeler drifted into your lane and clipped your driver-side door. By the time you got to the ER, a man with a clipboard was already at the scene taking photos for the trucking company. Now their insurer is calling, and the offer sounds nothing like what your bills look like.

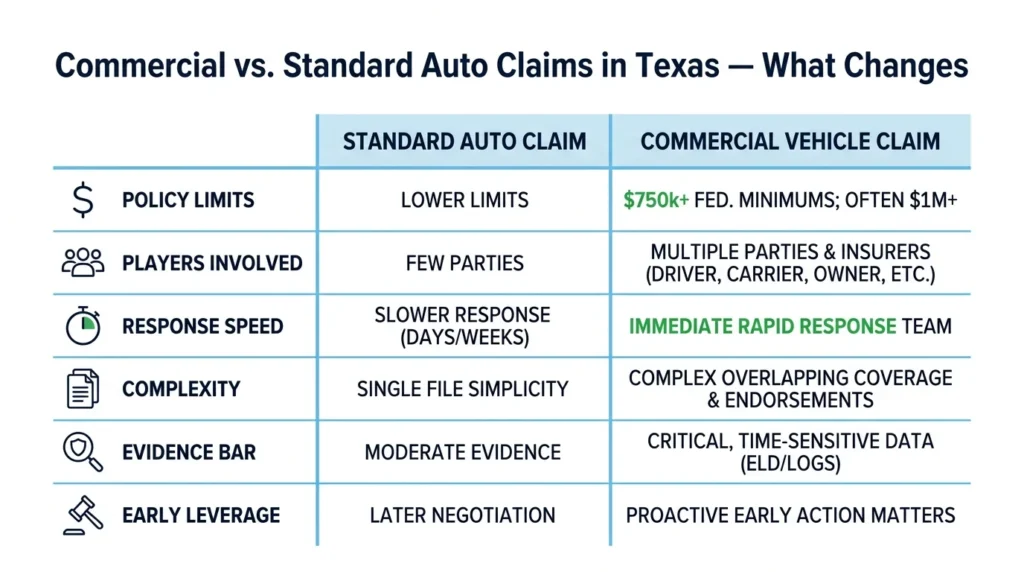

Commercial vs. Standard Auto Claims in Texas

Commercial vehicle claims operate on a different scale than ordinary auto claims. Policy limits for interstate carriers start at $750,000 under federal minimums for general freight, with many carriers and brokers requiring $1 million or more in practice. Multiple insurers may share liability, and the carrier’s rapid-response team is usually building a defense before you leave the hospital.

The trucking company knows the value of moving first. You should know it too.

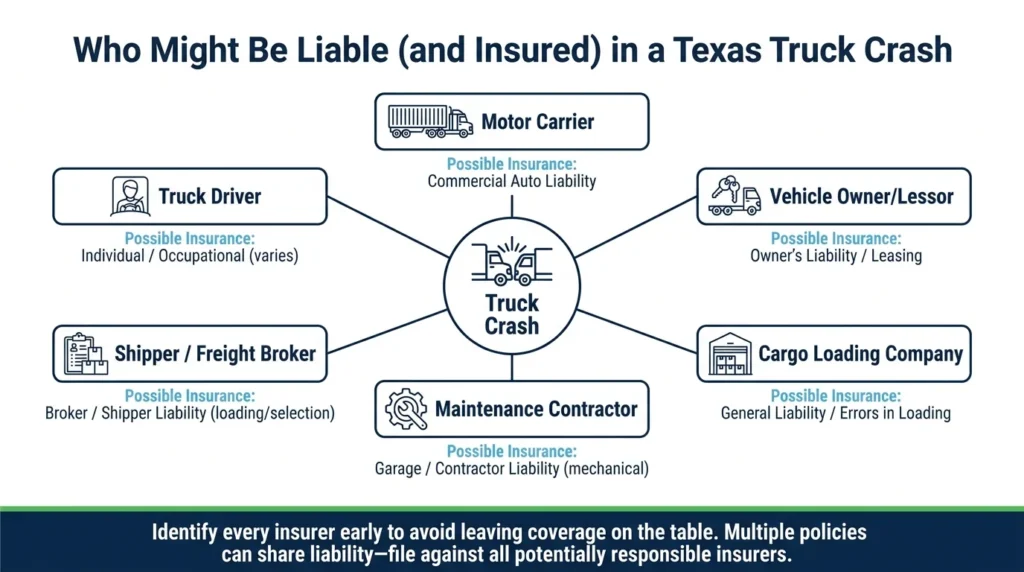

Multiple parties may carry coverage on a single crash: the driver, the carrier, the vehicle’s owner, a cargo shipper, or a maintenance contractor. Identifying every potentially liable insurer before you file shapes your strategy and your leverage. Treating the claim as a single-defendant case can leave money on the table.

Intrastate Coverage Requirements

Texas regulates commercial vehicles operating solely within state borders. The Texas Transportation Code Chapter 643 governs motor carrier registration and insurance filings for these intrastate carriers. The applicable minimums depend on vehicle weight and cargo type.

You will need to know whether the truck was running an intrastate or interstate route. The governing rules and the insurer’s compliance duties depend on that single fact.

Interstate Coverage Requirements

Federally regulated carriers crossing state lines fall under 49 CFR Part 387, which sets minimum coverage and the MCS-90 endorsement requirement. The MCS-90 acts as a backstop when the primary policy has gaps or exclusions.

This endorsement can be a critical recovery tool when an insurer denies coverage on technical grounds. It obligates the insurer to pay a judgment up to the federal minimum limit, even when the carrier wants to walk away.

Evidence & Documentation to Gather First

Commercial adjusters apply a heavier standard of evidence than personal-auto adjusters because the dollars at risk are larger. Missing or thin records are the most common basis for disputing injury severity. The earlier you start building your file, the harder it is for the insurer to write your claim down.

At the scene, take photos of all vehicles from multiple angles, as well as skid marks, road conditions, and signage visibility. Get the driver’s license, CDL number, carrier name, and the USDOT number printed on the cab door. Ask about dashcam footage and the bill of lading, or the legal document issued by the carrier.

Additional documents to request include driver logs, hours-of-service records, the driver’s employment status, vehicle inspection reports, and any prior safety violations on the carrier’s FMCSA file. Electronic logging device data is time-sensitive, and spoliation, or the failure to preserve evidence, can occur if you do not make a request in writing quickly.

Medical documentation drives the injury portion of your claim. Collect all ER records, diagnosis codes, treatment notes, prescriptions, and a written statement from your treating physician about future care. Gaps in treatment give the adjuster a reason to argue you were not really hurt.

Document your economic losses too: pay stubs or employer wage verification, tax returns if you are self-employed, repair or total-loss estimates, and receipts for out-of-pocket costs. Finally, request the official Texas Peace Officer’s Crash Report (CR-3) from TxDOT as soon as it is available. The same evidence discipline applies in most Texas car insurance claims, but commercial cases require more of it and faster.

An attorney experienced in truck accident cases can send preservation letters to the carrier before ELD data or driver logs cycle out.

How to File Your Claim Against a Commercial Insurer

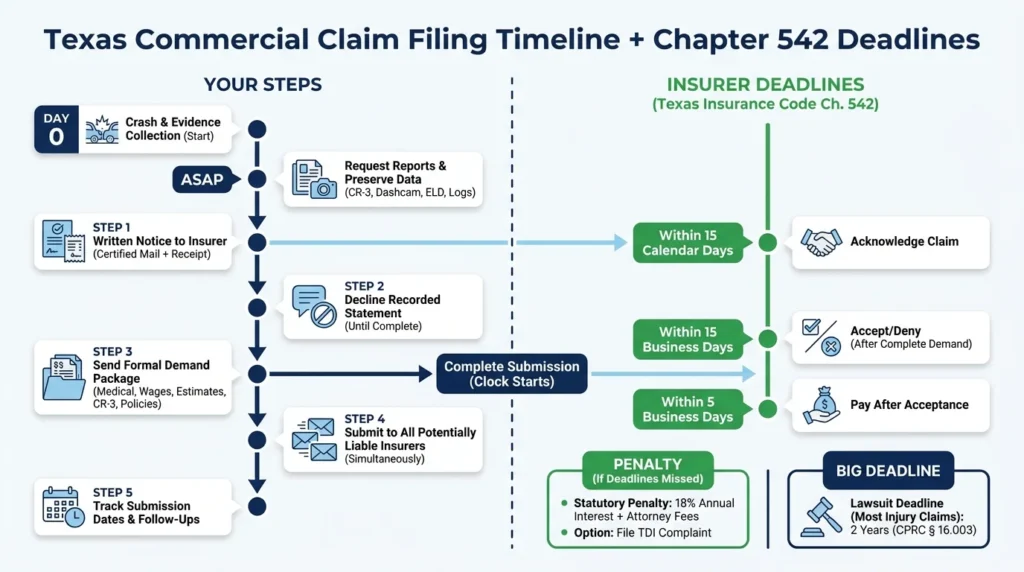

Filing a commercial claim is a sequence, not a single action. Each step protects the next one. Skipping a step usually means the insurer gets to dictate the pace.

Step 1: Notify the insurer in writing. Verbal notice does not create a paper record. Send a written notice by certified mail and keep the receipt.

Step 2: Decline a recorded statement until your file is complete. Recorded statements made before you have full documentation are routinely used to minimize claims. There is no Texas rule that forces you to give one on the adjuster’s schedule.

Step 3: Submit a formal demand package. Include the CR-3 report, all medical records and bills, your physician’s narrative on future treatment, lost wage documentation, vehicle damage estimates, and a cover letter naming every carrier and policy number you are claiming against.

Step 4: Submit to every potentially liable insurer at the same time. Holding one claim while waiting on another insurer creates coverage gaps and timing problems you do not want.

Step 5: Track every submission date. Texas Insurance Code Chapter 542 sets specific acknowledgment, acceptance, and payment deadlines once the claim is filed. Your submission date is the foundation for enforcing those obligations later. Reviewing a typical truck accident claim timeline can help you set expectations for how long each stage takes.

Texas Insurer Response Deadlines You Should Know

Chapter 542 of the Insurance Code creates hard deadlines for insurers handling covered claims. The insurer must acknowledge receipt within 15 calendar days, accept or deny within 15 business days of receiving all required documentation, and pay within 5 business days of acceptance. Missing these triggers a statutory penalty.

That penalty is 18 percent annual interest on the delayed amount, plus reasonable attorney fees. When commercial policy limits are involved, the dollar value of that penalty grows quickly. Insurers know this, which is part of why tracking your submission dates matters.

If the insurer stops communicating or stalls past the deadlines, the Texas Department of Insurance accepts formal complaints. Filing a TDI complaint creates an official record and often speeds up compliance.

Adjuster delay tactics are common in commercial claims because every week the file sits open is a week the carrier keeps the money. Document each contact, each request for additional information, and each promise the adjuster makes.

Work with a Commercial Vehicle Injury Attorney

Commercial vehicle claims reward preparation and punish delay. Texas gives most injury claimants a two-year deadline from the date of the crash under Texas Civil Practice and Remedies Code § 16.003, and that window closes whether your file is ready or not.

Angel Reyes & Associates has over 30 years of experience handling commercial vehicle claims against trucking companies and their insurers across Texas. The firm works on contingency, meaning no fee unless we win, and has recovered more than $1 billion for clients.

Free consultations are available, and the team can handle most of your case remotely. Contact us today to talk through your situation and the next steps.

Past results do not guarantee future outcomes.

Commercial Vehicle Insurance Claim FAQs

Can a commercial insurer in Texas deny my claim because the truck driver was an independent contractor?

Carrier insurers sometimes argue they are not responsible for an independent contractor’s actions, but Texas courts and federal regulations look closely at how much control the carrier actually had over the driver. The FMCSA’s “statutory employee” doctrine can override contractor labels for interstate drivers, meaning the carrier may still be liable regardless of how the employment relationship is classified.

What is the MCS-90 endorsement's coverage limit, and is it the same for every truck?

The MCS-90 limit varies by cargo type: $750,000 for general freight, $1 million for oil transport, and $5 million for hazardous materials under 49 CFR Part 387. The endorsement only covers the federal minimum, so if the carrier’s primary policy limit is higher, the MCS-90 alone does not get you there.

Does Texas allow me to file a complaint if a commercial insurer low-balls my settlement offer?

A low offer by itself is not a violation the Texas Department of Insurance can act on, but an insurer that misrepresents policy terms, fails to investigate within a reasonable time, or ignores documentation you submitted may be engaging in an unfair settlement practice under Texas Insurance Code Chapter 541. Filing a TDI complaint in those situations creates an official record and can prompt the insurer to revisit its position.

Can the cargo owner or shipper be held responsible if defective loading caused the crash?

Yes. If improper loading or an unsecured load contributed to the crash, the shipper, freight broker, or loading company may share liability alongside the driver and carrier. Each of those parties may carry separate insurance coverage, which is why identifying every company in the cargo chain is necessary early in the claims process.

What happens to my claim if the trucking company files for bankruptcy after the crash?

If the carrier files for bankruptcy, an automatic stay may pause your civil claim, but you can often still pursue the insurer directly for the policy proceeds since insurance assets are typically treated separately from the carrier’s general estate. Texas courts and federal bankruptcy procedures both allow injured claimants to petition for relief from the stay in order to proceed against available insurance coverage.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 70,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...