How to File a Car Insurance Claim in Texas, Step-by-Step

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- Texas insurers must acknowledge a claim within 15 days under Insurance Code § 542.056.

- First-party claims use your own coverage; third-party claims target the at-fault driver's policy.

- The statute of limitations to sue over a Texas car crash is generally two years from the date of the accident.

You’re sitting on the shoulder of I-35 near Round Rock, hazard lights blinking, the other driver pacing on his phone. Your bumper is crumpled, your neck already feels stiff, and you have no idea whose insurance company to call first.

The next few hours and days shape how your claim plays out, and it starts with the process of assembling evidence and then filing an insurance claim. But how do you do that correctly? If you’ve never been in a car accident or gone through the process before, this can be overwhelming. Let us walk you through how to file a car insurance claim in Texas.

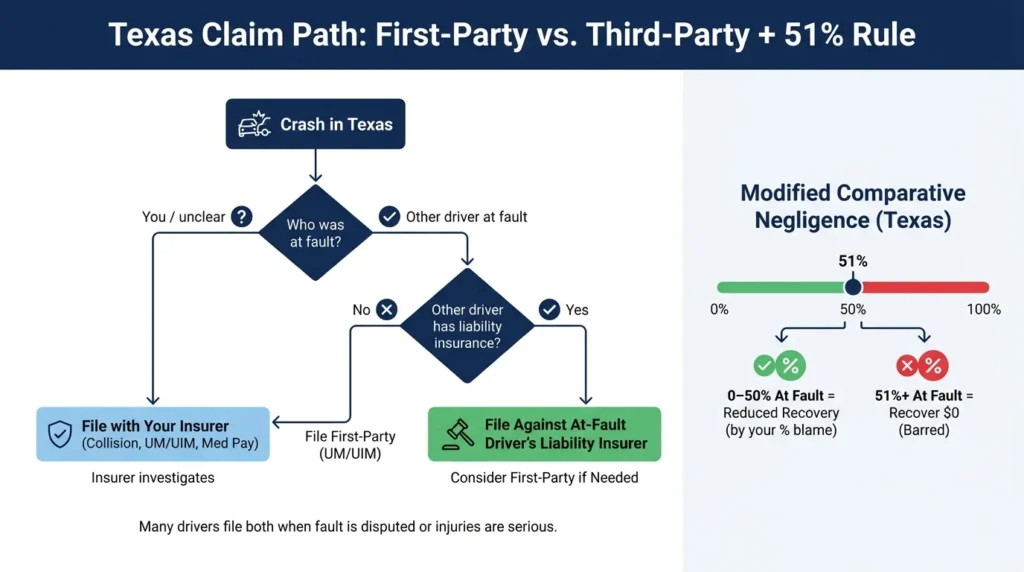

First-Party vs. Third-Party Claims

A first-party claim is one you file with your own insurance company under coverage you pay for, like collision or uninsured motorist. A third-party claim (or liability claim) is one you file against the at-fault driver’s insurer. The right path depends on who caused the crash and what coverages each driver carries.

If you caused the wreck, or fault is unclear, you generally file a first-party claim. If the other driver clearly caused the crash and has liability coverage, a third-party claim lets their insurer pay for your repairs, medical bills, and other losses. Many drivers file both at once, especially when injuries are serious or fault is disputed.

Texas follows a modified comparative negligence rule. If you are 51% or more at fault, you cannot recover damages from the other driver. If you are 50% or less at fault, your recovery is reduced by your share of blame. That math affects which claim to make and how much you can realistically expect.

Required Documentation & Evidence

Strong car insurance claims are built on documents, not arguments. Texas insurers want proof of what happened, who was involved, what was damaged, and what it costs to make you whole. What you do after a car accident impacts how organized your documentation is and how fast your claim moves.

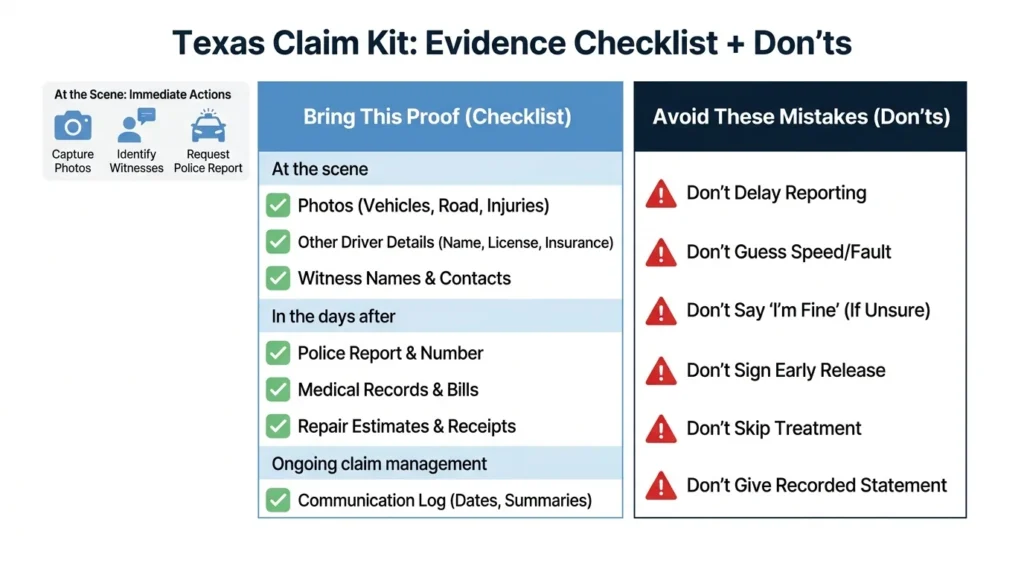

Start with the crash scene itself by taking photos of:

- Every vehicle from multiple angles

- The road

- Skid marks

- Traffic signs

- Any visible injuries

Get the other driver’s name, address, license number, license plate, insurance carrier, and policy number. Ask witnesses for their names and phone numbers before they leave.

A police report carries weight with adjusters. In Texas, officers are required to investigate crashes involving injury, death, or apparent damage of $1,000 or more. You can request the official report from the Texas Department of Transportation crash reports portal once the officer files it. Even when officers don’t respond to the accident scene, you can file a Driver’s Crash Report yourself.

For injury claims, keep every medical record, bill, prescription receipt, and physical therapy note. For property damage, get at least one written repair estimate and save receipts for towing, rental cars, and rideshare trips. Proper documentation can make the difference between a paid personal injury claim and a denial.

Texas Filing Deadlines & Timelines

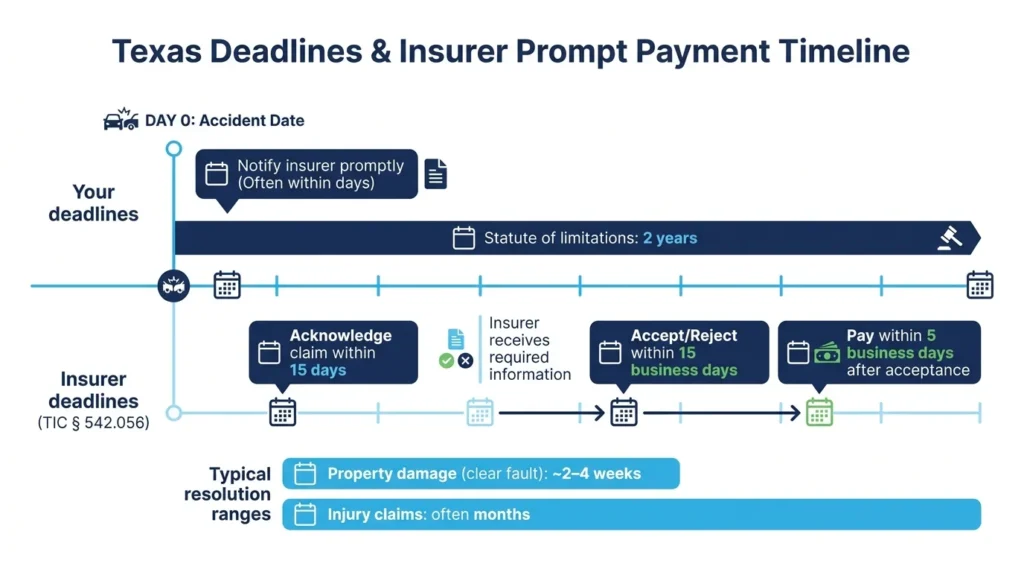

Two clocks run after a crash. The first is your policy’s prompt notice requirement, which usually means notifying your insurer within days. The second is the legal deadline to sue, which in Texas is generally two years from the date of the accident under the statute of limitations for personal injury and property damage.

Insurance companies also have deadlines to follow. Under the Texas Insurance Code (TIC) § 542.056, an insurer must acknowledge your claim within 15 days of receiving notice. After receiving all the requested information, the insurer has 15 business days to accept or reject your claim. If accepted, payment is generally due within five business days.

Real timelines vary. A simple property damage claim with clear fault may close in two to four weeks. Injury claims often take months because medical treatment must stabilize before the full value is known.

If your insurer drags its feet without a valid reason in bad faith, that delay can become its own problem. Fighting a Texas insurance bad faith claim can be challenging on your own. A lawyer can help explain when delays cross the line.

Step-by-Step Filing Process

After a crash in Texas, these are the practical steps you should follow in most cases:

- Call your insurer’s claims line as soon as you’re safe, even if you think the other driver is at fault.

- Provide basic facts: date, time, location, vehicles involved, and a short description of what happened.

- Submit photos, the crash report number, medical records, and repair estimates as they become available.

- Cooperate with the assigned adjuster, but stick to facts and avoid guessing about speed, distance, or fault.

- Track every call, email, and letter in a single folder with dates and names.

Adjusters are trained negotiators. They may ask for a recorded statement or a broad medical authorization. You are not required to give either before understanding what you are signing. Take notes during every call and ask for written confirmation of any deadline they set.

If you’re filing a third-party claim, expect more friction. The other driver’s insurer owes you nothing until liability is established. Send a clear written notice of claim, then follow up in writing each time you provide new information.

An attorney can step in at this stage when adjusters stop returning calls or start questioning your medical treatment.

Common Filing Mistakes to Avoid

Small missteps early in your claim can cost thousands later. The most common mistake is waiting too long to report. Even a few weeks of silence gives an insurer reason to argue the damage came from something else.

Another frequent error is talking too much. Adjusters listen for casual phrases like “I’m fine” or “I didn’t see him” and use them later to reduce payouts. Stick to what you know. If you are unsure about an injury or detail, say so.

Quick settlement offers are tempting, especially when bills are stacking up. But early offers rarely reflect future medical care, lost wages, or long-term pain. Once you sign a release, your claim is closed for good. Understanding your claim’s true value requires a careful look at all damages, not just the bills already in hand.

Finally, do not skip medical appointments or stop treatment early. Gaps in care give insurers room to argue you weren’t really hurt. The Texas Department of Insurance consumer guidance on claim problems covers your rights when an insurer pushes back, including how to file a formal complaint.

Work with an Experienced Attorney

Insurance claims are easier to handle when someone in your corner knows the playbook. Angel Reyes & Associates has spent over 30 years helping Texas drivers file, fight, and finalize car insurance claims across the state.

We work on a contingency fee basis, so there is no fee unless we win your case, and consultations are always free. Our attorneys have recovered more than $1 billion for clients. If your claim is stalled, denied, or just feels too complicated to handle alone, contact us for a free, no-obligation review.

Past results do not guarantee future outcomes.

Insurance Claim Filing FAQs

What happens if the other driver doesn't have insurance in Texas?

You can file an uninsured motorist claim with your own insurance company if you have this coverage. Texas doesn’t require uninsured motorist coverage, but many policies include it.

What if my insurance company asks me to use a specific repair shop?

You have the right to choose your own repair shop in Texas. Insurance companies may recommend preferred shops, but they cannot require you to use them.

How much does it cost to get a copy of the police report in Texas?

Texas crash reports typically cost $6 to $8 through the Department of Public Safety online portal. Some local police departments may charge different fees.

What should I do if the insurance adjuster seems to be stalling my claim?

Document all delays and missed deadlines, then file a complaint with the Texas Department of Insurance if the insurer violates prompt payment requirements under state law.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 70,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...