How UM/UIM Applies to Motorcycle Accidents in Texas

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- UM coverage applies when a driver flees a Texas motorcycle crash and cannot be identified by police.

- Many Texas UM policies require physical contact between vehicles before a hit-and-run claim is paid.

- Texas insurers must offer UM/UIM coverage in writing, and rejections must be signed to be valid.

You were heading home on I-35 outside Round Rock when a driver swerved into your lane, clipped your bike, and accelerated off the next exit before you could read the plate. Your shoulder is in a sling, your bike is totaled, and the police report lists the other driver as unknown.

Now your own insurer is asking questions, and you are wondering whether the coverage on your policy actually helps you here.

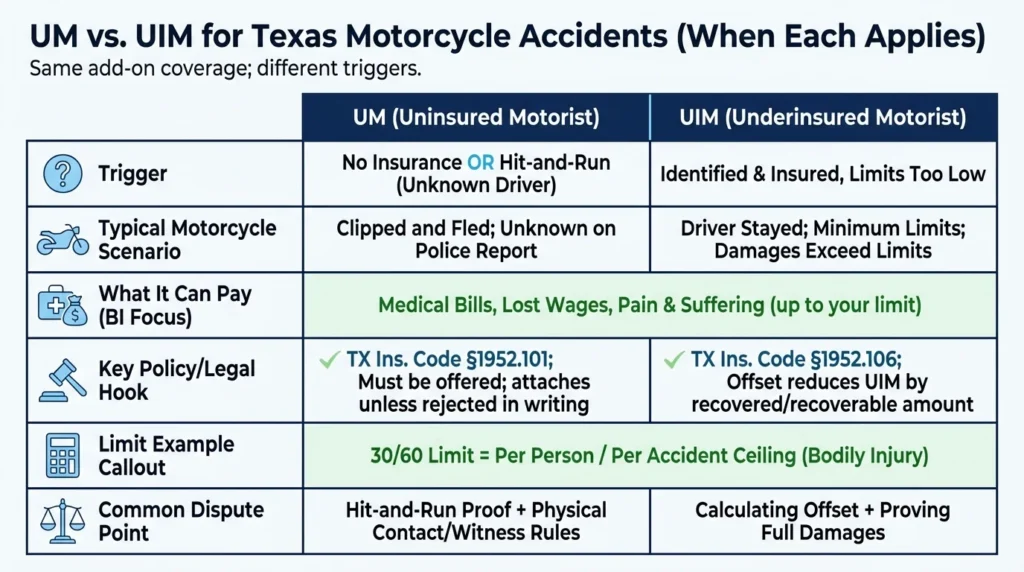

UM vs. UIM Coverage for Texas Riders

Uninsured motorist (UM) and underinsured motorist (UIM) coverage are two parts of the same add-on protection on your auto policy. UM pays when the at-fault driver has no insurance or cannot be identified, making it the operative coverage for a fled driver. UIM pays when the at-fault driver is known but carries too little insurance to cover your losses.

Uninsured Motorist Coverage

UM coverage steps in when there is no liable insurer on the other side. That includes the classic hit-and-run, where the driver leaves before anyone can identify them.

Under Texas Insurance Code § 1952.101, insurers must offer UM/UIM coverage with every auto policy in the state. You must reject it in writing, or it attaches to your policy by default. For riders, this is the coverage that pays medical bills, lost wages, and pain and suffering when the driver who hit you vanishes.

Coverage applies up to your policy limit. If you bought a 30/60 UM policy, that is the ceiling on what your insurer will pay for bodily injury, regardless of how high your actual damages climb. The Texas Department of Insurance overview of UM coverage walks through how these limits stack against typical injury claims.

Underinsured Motorist Coverage

UIM coverage is different. It applies when the at-fault driver is identified and has insurance, but their policy limits do not cover your full damages. UIM fills the gap, up to your own UIM limit.

Texas Insurance Code § 1952.106 governs how the offset works. The at-fault driver’s payment reduces your UIM benefit by the amount that is recovered, or that is recoverable from that driver’s insurer.

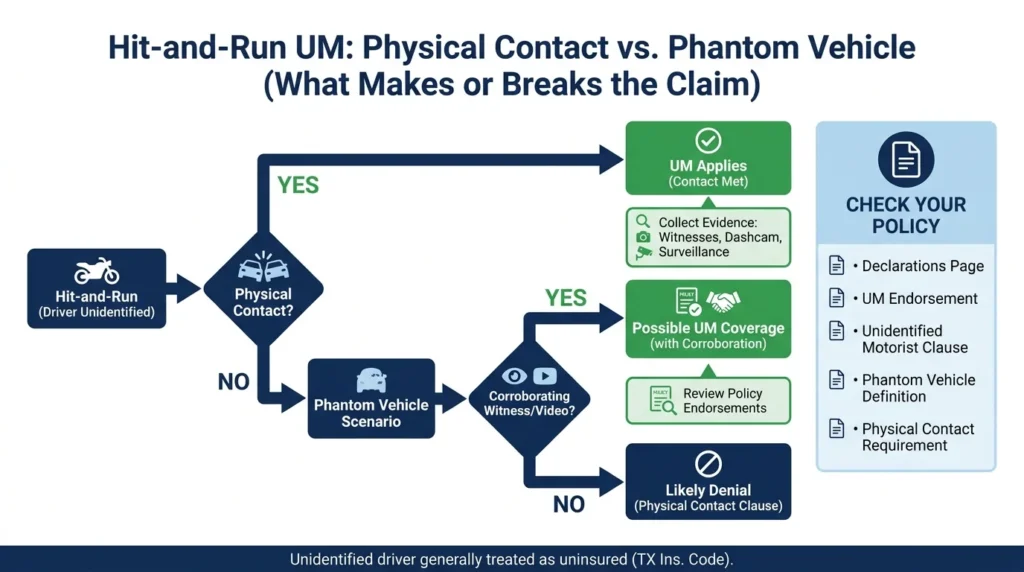

The Physical Contact Requirement in Hit-and-Run Claims

Many Texas UM policies require that the fleeing vehicle make actual physical contact with your motorcycle. If a driver ran you off the road without ever touching your bike, a standard UM claim may be denied. This single policy term decides a large share of hit-and-run disputes.

A crash in which the other vehicle never touches yours is called a phantom vehicle or no-contact claim. Some UM policies cover these scenarios only if you can produce a corroborating witness who saw the other vehicle cause the crash. Without that witness, your insurer can point to the contact clause and refuse to pay.

Policy language controls. Pull your declarations page and look for “unidentified motorist” or “phantom vehicle” provisions next to the physical contact clause. The wording on your specific policy is what your insurer will use to evaluate the claim.

The financial responsibility framework in Texas Transportation Code § 601.051 establishes the baseline insurance requirement for Texas drivers, and the definition of an “uninsured motor vehicle” for UM purposes is set out in Texas Insurance Code § 1952.102. That definition shapes how insurers treat phantom vehicle claims, since an unidentified driver is presumed uninsured for UM purposes. For more on dealing with these situations, see our guide on what to do after being hit by an uninsured driver.

An attorney can help you read your policy and push back when an insurer denies a no-contact claim using ambiguous language. Riders who need help evaluating coverage can start with our Texas motorcycle accident practice.

What Happens If You Rejected UM/UIM Coverage?

A valid written rejection under § 1952.101 closes the UM/UIM avenue. Without that coverage, your remaining options are a direct lawsuit against the at-fault driver (if identified) or a Personal Injury Protection (PIP) claim if you maintained personal injury protection. After a hit-and-run with no identified driver, the practical effect of a rejection is no first-party recovery.

The rejection must be in writing and signed. If you cannot locate a signed rejection form in your file, the coverage may not have been validly waived. Insurers sometimes claim a verbal rejection or assume one from policy paperwork, but neither is enough under Texas law.

Even when a signed form exists, it can be challenged. If you were not clearly informed of what you were giving up, an attorney can assess whether the waiver was knowing and voluntary. Riders in this situation should also see how claim handling differs for hit-and-run accident cases, since procedural posture matters when no liable driver is on the hook.

If property damage was your only loss, the calculus changes. Our breakdown of Texas non-injury accident claims covers how those cases move without a bodily injury component.

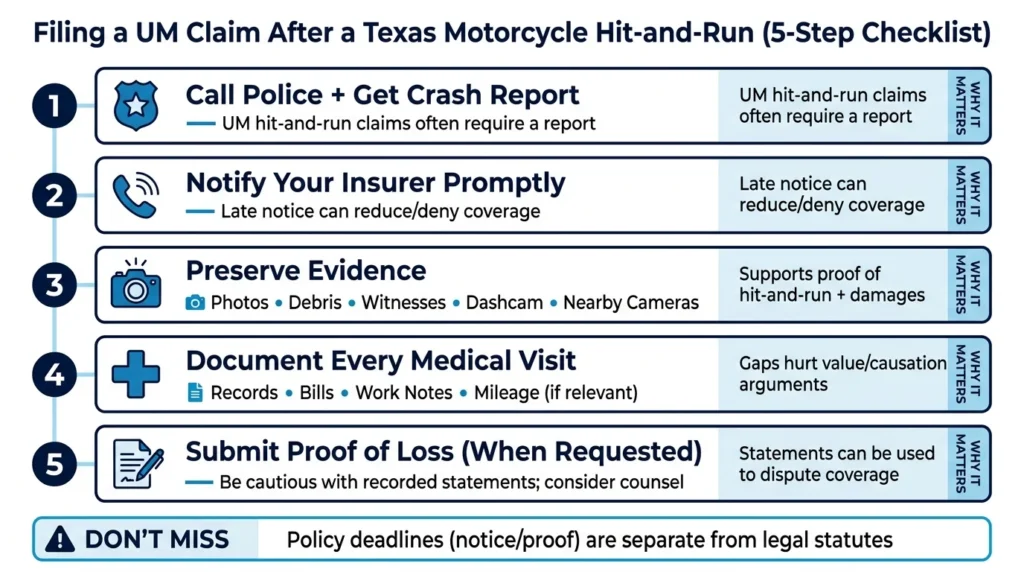

Filing a UM Claim After a Motorcycle Hit-and-Run

A UM claim is a first-party claim against your own insurer, where the process has specific steps, and missing one can give the insurer grounds to reduce or deny the payout. Treat the claim as adversarial from the start. Your insurer is a business with its own financial interest in minimizing what it pays.

Step 1: Call the police and get a crash report. A documented police report is a standard insurer condition for hit-and-run UM claims. File one even if you were taken from the scene before officers arrived.

Step 2: Notify your insurer promptly. Most UM policies contain a prompt-notice condition, and a delayed notice can be used to deny the claim or reduce the payout. A phone call preserves the right; you do not need a formal claim filing on day one.

Step 3: Preserve evidence. Photograph the scene, your bike, your injuries, and any debris from the fleeing vehicle. Get witness names and numbers, and look for dashcam footage from nearby vehicles and surveillance video from businesses on the route.

Step 4: Document every medical visit. UM bodily injury claims are valued on documented medical costs, treatment records, and lost wage evidence, so gaps in treatment give the insurer a tool to argue your injuries were minor or unrelated. Familiarity with common motorcycle accident injuries helps you understand what to track.

Step 5: Submit a written proof of loss when the insurer requests it. The insurer may ask for a recorded statement. Talk to an attorney before giving one, because your statement can be used to support a coverage denial later, and there is no benefit to providing it without counsel reviewing the questions first.

Our Texas case results show outcomes in motorcycle insurance disputes and reflect how these claims play out when handled with experienced support.

Get Help with Your Motorcycle UM/UIM Claim

With over 30 years of experience, Angel Reyes & Associates represents injured Texas motorcyclists in UM/UIM disputes and hit-and-run cases. We work on contingency, which means no fee unless we win.

We are available 24/7 and offer free consultations. Contact us today to discuss your hit-and-run claim with a Texas motorcycle accident attorney.

Past results do not guarantee future outcomes.

Texas Motorcycle UM/UIM FAQs

Can I stack UM coverage from multiple policies after a motorcycle hit-and-run in Texas?

Texas allows stacking of UM coverage in some cases, but only if your policies do not contain an anti-stacking clause. Many Texas auto and motorcycle policies include language that limits recovery to a single policy limit, so you need to check each policy’s terms.

Does my UM policy cover a passenger on my motorcycle who was injured in a hit-and-run?

A passenger may be covered as an “insured” under your UM policy, but this depends on how your policy defines that term. Some policies extend UM protection to passengers on a covered motorcycle, while others limit coverage to the named insured and certain family members.

How long do I have to file a UM claim after a motorcycle hit-and-run in Texas?

Texas has a four-year statute of limitations for contract claims, which includes UM claims against your own insurer. By contrast, you only have two years from the date of the crash to file a standard personal injury lawsuit against the at-fault driver. Filing your claim promptly still matters, though, because your policy’s notice condition is separate from the legal deadline and can be enforced against you earlier.

Will my health insurance have to be repaid if my UM claim later settles?

If your health insurer paid medical bills related to the crash, it may have a subrogation right to recover those costs from your UM settlement. The amount owed depends on your health plan type, since ERISA-governed plans and private Texas plans follow different subrogation rules.

Can the at-fault driver be pursued personally if they are identified after I already filed a UM claim?

Yes. If the driver is later found, you may have the right to pursue them directly, but your insurer may have a subrogation interest in any recovery you obtain. Texas Insurance Code § 1952.108 addresses the insurer’s right to recover UM benefits paid once a liable party is identified.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 70,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...