How Much Motorcycle Insurance Do You Need in Texas?

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- Texas law requires riders to carry at least 30/60/25 liability motorcycle insurance.

- State minimum limits rarely cover the full cost of a serious motorcycle crash.

- UM/UIM coverage protects you when an at-fault driver has no insurance or too little.

You just put a down payment on the bike you have wanted for years, and now the insurance quote is sitting in your inbox. You are riding the Loop 1604 frontage roads outside San Antonio on weekends, wondering if the cheapest policy is enough. The legal minimum looks affordable, but you have heard motorcycle crashes get expensive fast.

How much coverage do you actually need to protect yourself?

Texas Motorcycle Insurance Minimums

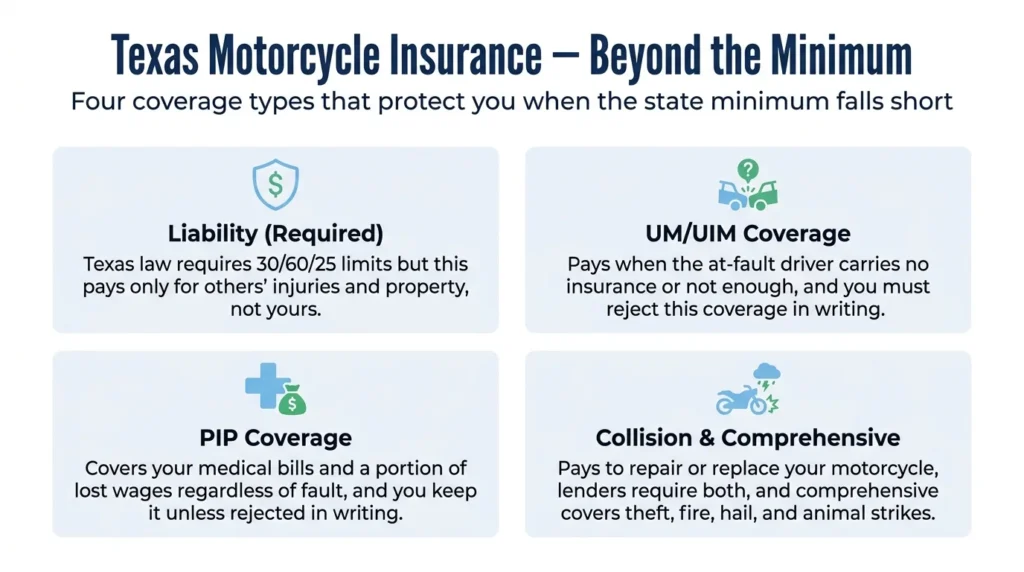

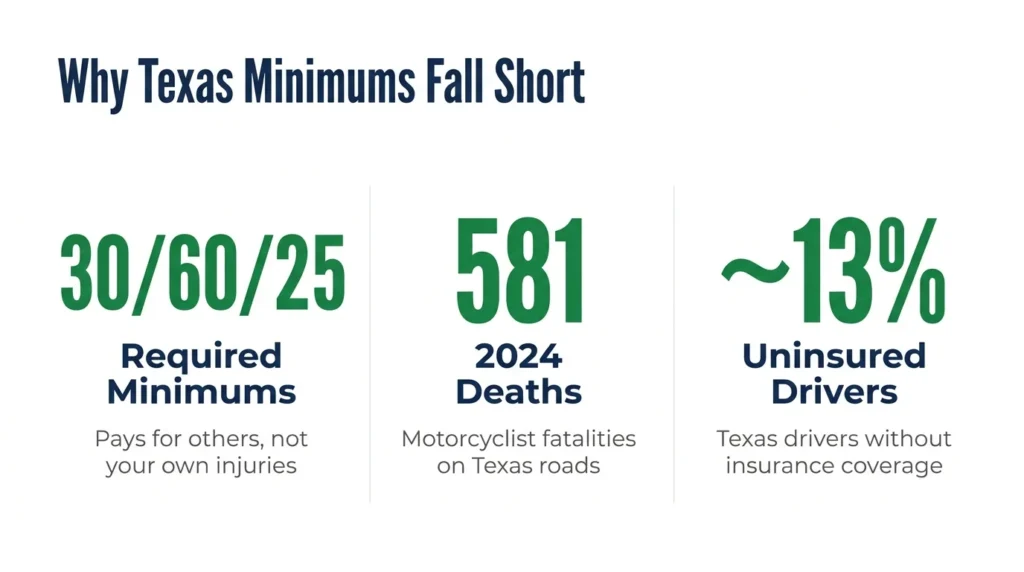

Texas requires every motorcycle rider to carry liability insurance with at least 30/60/25 limits. That means $30,000 for injuries to one person, $60,000 total when two or more people are hurt, and $25,000 for property damage. These minimums come from the Texas Transportation Code § 601.072.

Your motorcycle falls under the same financial responsibility law that covers every other vehicle on the road. Coverage is not optional, and you cannot waive it. The Transportation Code § 601.051 makes that requirement clear for all motor vehicle operators in the state.

Riding without insurance carries real penalties. You can face fines, a license suspension, and even vehicle impoundment. The Texas Department of Insurance outlines what riders must carry and what happens if you skip it.

Here is the part most riders miss. Liability coverage only pays for other people and their property when you cause a crash. It pays nothing for your own injuries, and nothing to repair or replace your own motorcycle.

Why Minimums Fall Short After a Crash

The state minimum keeps you legal, but it rarely covers a serious crash. A bad collision can run through $30,000 in medical bills within days, and you become personally responsible for everything past your limit.

Motorcycle crashes in Texas are severe and common. In 2024, 581 motorcyclists died and 2,534 suffered serious injuries on Texas roads, according to state crash figures. A single hospital stay, surgery, and rehab can blow past the minimum fast.

When your liability limits run out, the unpaid balance does not disappear. It follows you. The 30/60/25 minimum was built for legal compliance, not to shield your savings, your home, or your future wages.

You can see how often these crashes happen by year through the TxDOT crash data analysis portal. The numbers make the stakes concrete before you ever sign a policy.

Understanding what a serious claim is actually worth helps you judge whether your coverage is enough. Our breakdown of how motorcycle accident settlements work in Texas shows how quickly costs add up.

Optional Coverages Worth Considering

Beyond the required liability, a handful of optional coverages do the real work of protecting you. The two most riders confuse with each other deserve a closer look.

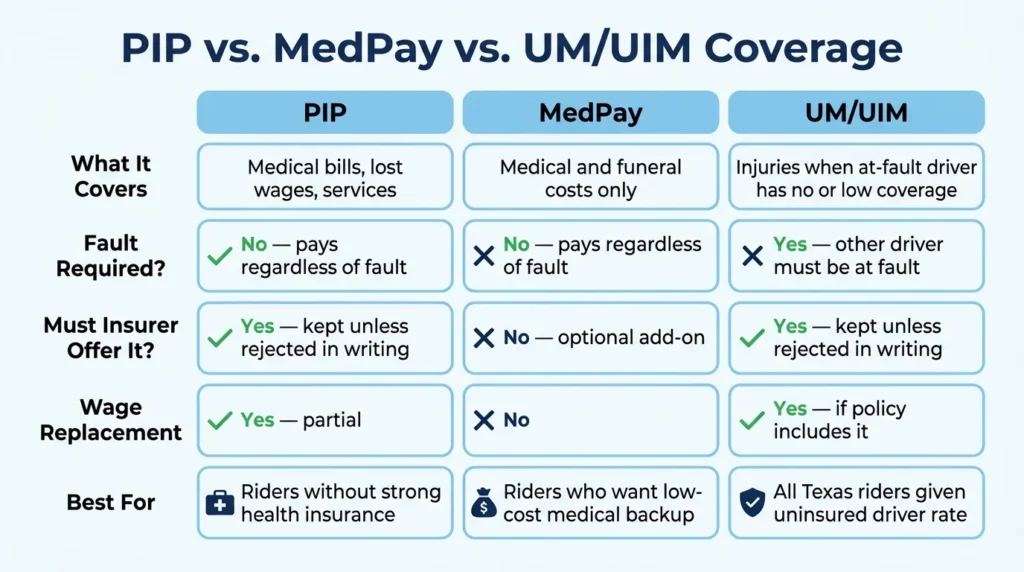

Uninsured & Underinsured Motorist Coverage

This coverage pays when the at-fault driver has no insurance, or not enough to cover your losses. Roughly 12 to 14 percent of Texas drivers are uninsured, which makes this the most valuable optional coverage you can add.

Texas insurers must offer it on every auto liability policy. If you do not want it, you have to reject it in writing. The Texas Insurance Code § 1952.101 sets that requirement.

The two halves work differently. Uninsured motorist coverage applies when the other driver carries no insurance at all. Underinsured motorist coverage applies when their limits are too low to cover what you actually lost. You can buy them together or separately. Our guide to handling an uninsured motorist accident walks through how a claim like this plays out.

Official state guidance explains what this coverage includes and why it matters in Texas. Even if you carry liability limits well above the minimum, an uninsured driver can still leave you with a gap, which is the case for carrying coverage above the minimums on UM, UIM, and PIP.

MedPay & PIP Coverage

Both MedPay and Personal Injury Protection cover your medical costs no matter who caused the crash. They differ in what else they pay for and whether the insurer has to offer them.

PIP is the broader of the two. It covers medical bills, a portion of your lost wages, and certain services like household help. MedPay covers only medical and funeral expenses, with no wage replacement. The Insurance Code § 1952.151 defines what PIP includes.

Your insurer must offer PIP, and you keep it unless you reject it in writing. The Insurance Code § 1952.152 sets that default. If you never sign a rejection, you are covered.

Picking between them depends on your other coverage and your budget. A side-by-side comparison of PIP, MedPay, and UM/UIM rules can help you weigh the cost before you decide.

Collision, Comprehensive & Custom Parts Coverage

These three coverages protect your motorcycle itself, not other people. None are required by law, but your lender will likely require the first two if you financed the bike.

Collision coverage: Pays to repair or replace your motorcycle when you are at fault or fault is disputed. Lenders almost always require it on a financed bike.

Comprehensive coverage: Pays for non-crash losses like theft, fire, hail, and animal strikes. Texas weather and theft rates are worth weighing here before you skip it.

Custom parts and equipment coverage: A separate endorsement for aftermarket parts and accessories. Standard collision and comprehensive policies cap custom parts at a low default amount, so riders with real money in modifications should confirm the policy covers full replacement cost.

The right mix depends on what your bike is worth and how much you put into it. A rider on a paid-off stock motorcycle weighs these differently than someone with a financed, heavily modified machine.

Work with an Attorney

Choosing the right coverage now is far easier than fighting over a gap after a crash. If you have questions about whether your limits would actually protect you, we can help you understand where you stand.

Angel Reyes & Associates has represented injured motorcyclists across Texas for more than 30 years. We offer free consultations, charge no fee unless we win, and have more than $1 billion recovered for clients. Our team handles Texas motorcycle accident claims and can review how a serious crash might affect you financially.

If you want a clear read on your situation, reach out to us for a free consultation. You can also meet the attorneys who would handle your case before you decide.

Past results do not guarantee future outcomes.

Motorcycle Minimum Insurance FAQs

Can a passenger on my motorcycle file a claim under my liability policy if they are injured in a crash?

Yes. Your liability policy covers injuries to passengers when you are at fault, up to your per-person limit. Passengers are treated as any other injured party under your 30/60/25 policy.

Does my Texas motorcycle policy cover me if I ride a borrowed or rented motorcycle?

Most standard motorcycle policies do not extend to bikes you do not own. Some insurers offer non-owned motorcycle coverage as an add-on, but coverage varies by policy, so check your declarations page before riding someone else’s bike.

How does Texas's comparative fault rule affect my ability to recover after a motorcycle crash?

Texas follows a modified comparative fault rule. If you are found 51% or more at fault, you cannot recover from the other driver; if you are 50% or less at fault, your recovery is reduced by your percentage of fault.

Is there a deadline to file a motorcycle accident lawsuit in Texas?

Texas gives injured riders two years from the date of the crash to file a personal injury lawsuit. Missing that deadline generally means losing the right to sue.

Can I stack UM/UIM coverage across multiple motorcycle policies in Texas?

Stacking lets you combine UM/UIM limits from more than one policy to increase your total available coverage. Texas law permits stacking in some situations, but many policies include anti-stacking clauses, so the answer depends on your specific policy language.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 70,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...