How Trucking Companies Use Self-Insurance Programs

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- Self-insured trucking companies qualify under 49 CFR, Part 387, and pay claims from their own funds. There is no independent insurance company reviewing claims or the carriers' conduct.

- A self-insured retention (SIR) means that the carrier controls claims up to a set dollar amount even if it carries traditional insurance above that threshold.

- Preservation of evidence and early attorney involvement are more critical in self-insured carrier cases.

When a trucking company’s in-house claims department calls after your crash involving one of its vehicles on I-10 near Houston, you may assume you’re speaking with a traditional insurance adjuster. That may not be so, since some of the largest freight carriers in the country are self-insured (they pay claims out of their own funds and handle every aspect of them internally).

Many truck accident victims are surprised to learn that a lot of trucking companies are actually self-insured. Understanding what this means and how these companies handle liability is critical to get the best results from your claim.

What Self-Insurance Means in the Trucking Industry

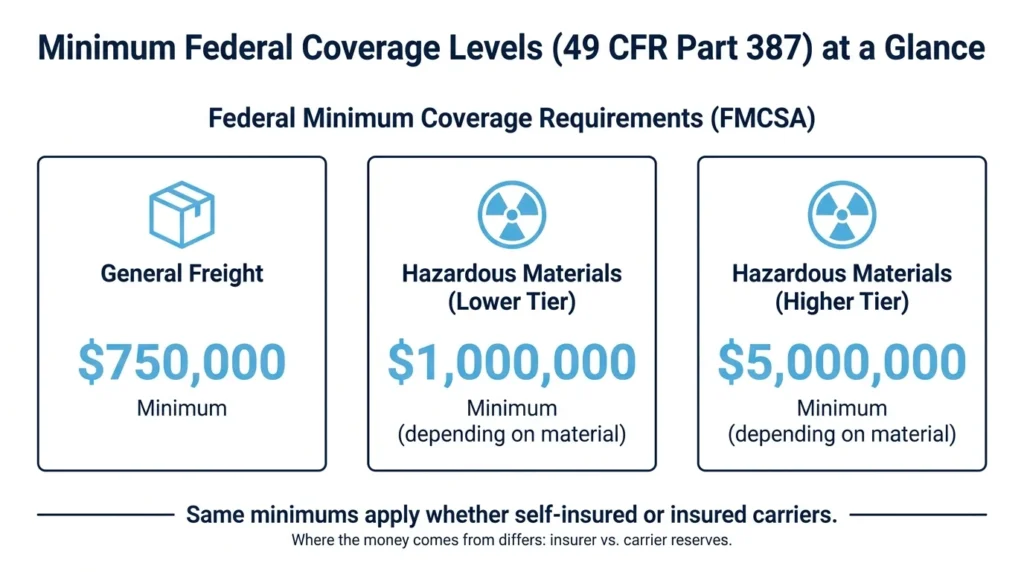

Motor carriers aren’t required by federal law to purchase traditional commercial insurance. Under 49 CFR, Part 387, a freight transporter can qualify as a self-insurer by demonstrating to the Federal Motor Carrier Safety Administration that it has enough funds to cover claims at the required minimum levels. Typically, only large trucking companies with substantial assets qualify to self-insure.

If you’ve been in an accident with a commercial carrier, you can check its insurance status in the federal government’s Safety and Fitness Electronic Records database. Search for the carrier by name or USDOT number. If the carrier is self-insured, the database will show “self-insurer,” rather than listing a commercial insurance company.

The coverage obligations are the same for a self-insured carrier and a traditionally insured carrier: $750,000 for general freight, $1 million or $5 million for hazardous cargo. The difference is that money used to pay claims comes from the carrier’s own reserves, not from a separate insurance company. For context on what coverage levels apply, see our explainer of Texas commercial truck insurance requirements.

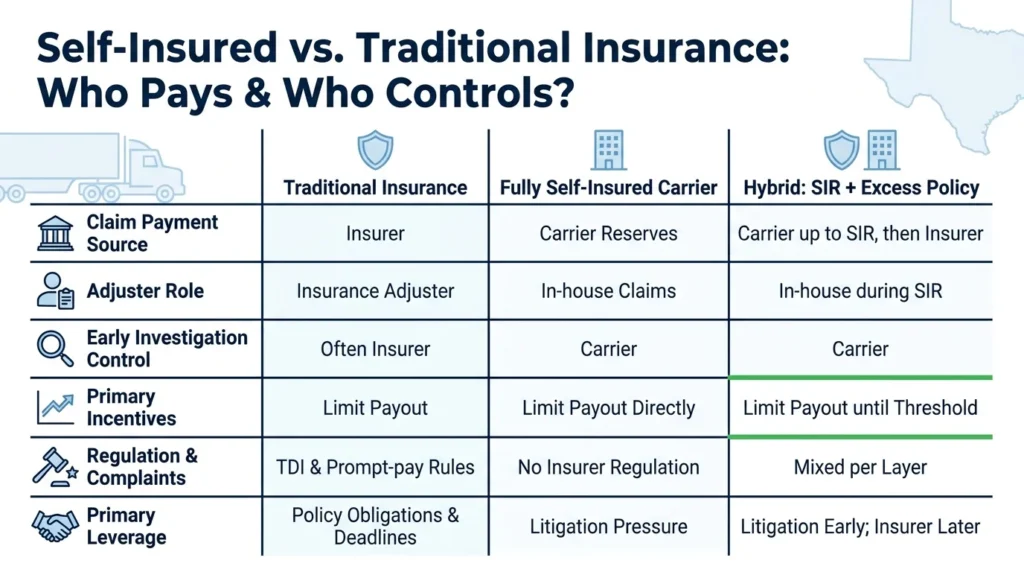

Self-Insured Retention: The Hybrid Model

Not every motor carrier that operates like a self-insurer is technically fully self-insured. Many large carriers use a self-insured retention (SIR) mechanism under an umbrella or excess policy.

In a SIR arrangement, the carrier pays a set dollar amount of any claim out of pocket (often $500,000 to upward of $2 million) before its own insurer takes over.

During the SIR period, the trucking company’s in-house team controls the investigation and settlement. If you’ve been injured in an accident with a vehicle from a carrier with a large SIR, know that the company, practically speaking, operates as a self-insured carrier during the most critical phase of negotiations over your claim.

That’s why it is key to your litigation strategy to find out right away whether the motor carrier is fully self-insured or operating with a SIR.

For a closer look at how commercial carriers try to get the upper hand with accident victims, see how trucking companies and insurers delay and deny claims in Texas.

Who Is Actually Handling Your Claim

The person who calls you from the carrier’s claims department is not a licensed independent adjuster employed by a regulated insurance company. As an employee of the trucking company, the representative is tasked with handling your claim in a way that is best for their employer, which is not what is best for you financially.

Large self-insured motor carriers often have internal claims management teams whose performance goals include limiting total claims payouts. Some carriers tie compensation for these employees to how little the company pays in damages to accident victims.

There is no independent insurer reviewing their decisions, no insurance regulatory board overseeing their conduct, and no Texas Department of Insurance complaint process that applies to their claims practices.

When you speak with the carrier’s in-house claims team, you are speaking directly with the party that owes you money and has a financial incentive to pay you as little as possible. Every statement you make goes into a file they control.

What Texas Law Does and Does Not Protect

Under Texas Insurance Code Chapter 542, licensed insurance companies are required to promptly and fairly handle claims; violating the law, including by using delay tactics or missing deadlines, can result in 18% annual interest penalties. A self-insured carrier, however, is not a licensed insurer, so in most circumstances, these penalties do not directly apply if the carrier improperly managed your claim.

This does not mean you have no legal recourse. A self-insured carrier that handles your claim in bad faith can be held liable under Texas tort law. That exposure includes actual damages and, in egregious cases, may support punitive damages. The process is carried out through the courts, not the insurance regulatory system.

The timeline and leverage are different. For a step-by-step guide on how the process works, see our Texas truck accident claim timeline.

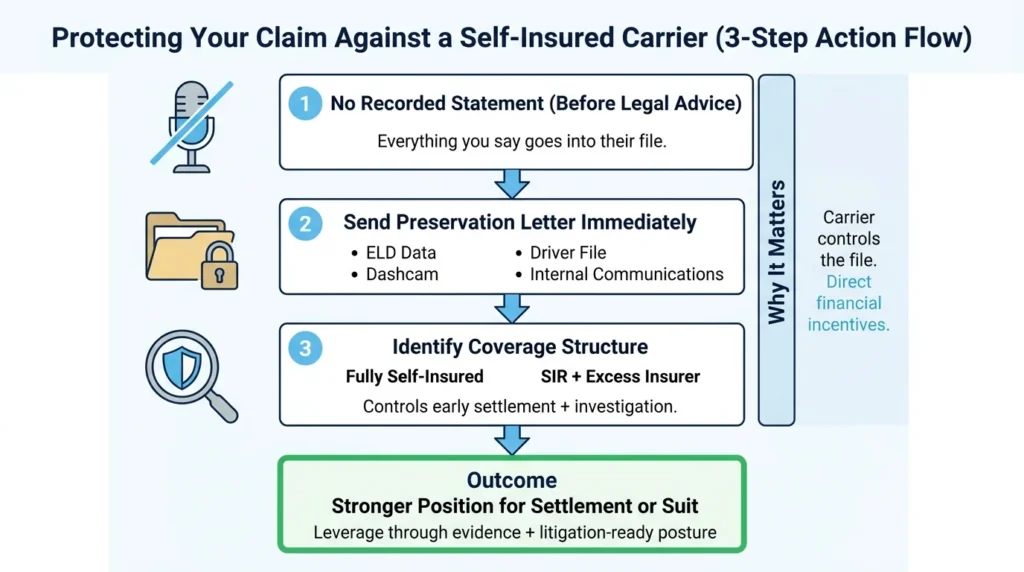

What to Do When the Carrier Is Self-Insured

The fundamental rules of protecting your claim don’t change, but the absence of a regulated insurer means every step matters more.

- Do not give the carrier’s in-house team a recorded statement before speaking with an attorney. There is no independent insurer reviewing whether the claims team is following proper procedures.

- Send a preservation letter to the carrier immediately, to ensure that relevant evidence and records (electronic logging device data, dashcam footage, driver qualification files, internal communications about the crash) are not destroyed, altered or lost.

- Determine whether the carrier is fully self-insured or using a SIR mechanism. The SAFER database, the carrier’s own disclosure, or litigation discovery will surface this information. If a traditional insurer takes over after the SIR threshold is met, that insurer is a separate party with its own interests and obligations.

For complete details on the claims process and what to do at each stage, check out how truck accident claims work in Texas.

Talk to a Lawyer Before You Settle

Claims against self-insured trucking companies require a different approach than claims against carriers backed by traditional insurers. There is no insurance regulatory system to use as leverage. The only effective tool is the courts, but using them effectively requires knowing what evidence to preserve, what claims to assert, and how to apply litigation pressure against a company that has every financial reason to fight.

Angel Reyes & Associates has handled truck accident cases across Texas for over 30 years. Our attorneys offer free consultations, and you pay no fee unless your case is resolved in your favor. If you were injured in a crash and the trucking company appears to be handling the claim itself, contact us, or visit the truck accidents page.

Past results do not guarantee future outcomes.

Self-Insured Trucking Company Accident FAQs

Can I still recover compensation from a self-insured carrier if it refuses to pay?

Yes. A self-insured carrier is liable for accidents caused by its drivers just like any other defendant. If the carrier refuses to settle a valid claim, you can file a lawsuit and pursue a judgment in court. The judgment would be satisfied from the carrier’s own assets, rather than from an insurance policy. For publicly traded carriers, those assets are substantial; for smaller or financially stressed carriers, solvency becomes a factor.

Does the MCS-90 endorsement apply to self-insured carriers?

No. The MCS-90 endorsement is a component of a commercial liability insurance policy. Self-insured carriers demonstrate financial responsibility to the FMCSA through a different mechanism. The federal minimum coverage obligation still applies to self-insured carriers, but it is enforced through a direct lawsuit, rather than by asserting the endorsement against an insurer.

Is the claims process faster or slower with a self-insured carrier?

It varies, but many truck accident attorneys report that self-insured carriers can be slower to settle because there is no independent insurer with its own cost-benefit analysis. The carrier’s in-house team may be motivated to minimize payouts, delay, and gather as much information as possible before acknowledging liability. There is also no insurance regulatory deadline (like the 15-business-day acknowledgment period under Texas Insurance Code Chapter 542) that formally applies. In practice, litigation is often the fastest path to a fair result with a self-insured carrier.

What happens to my claim if a self-insured trucking company files for bankruptcy?

If the carrier becomes insolvent and files for bankruptcy, your accident claim becomes a general unsecured debt in the bankruptcy proceeding. Unlike an insurance claim, there is no separate insurer to pursue. Recovery depends on the carrier’s available assets and where your claim falls in the creditor priority order. Identifying other potentially liable parties (a leasing company, a cargo broker, a maintenance provider) is important for your ability to collect if the carrier’s financial condition is in question.

About the Authors

Alex Ivanov

Writer

Alex Ivanov is a personal injury attorney at Angel Reyes & Associates, focused on car, truck, and motorcycle accident cases. Licensed in Texas and multiple federal districts, Alex brings international legal experience and a global education to his practice. He earned his LL.M. from Texas A&M University School of Law after graduating from Belarussian State University in 2016. Alex is fluent in Russian, English, Ukrainian, and Belarussian, and is recognized by multiple national trial lawyer associations for his results and leadership under 40.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...