How Insurers Determine Actual Cash Value

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- ACV is the market value of your vehicle before the crash, not what you paid for it.

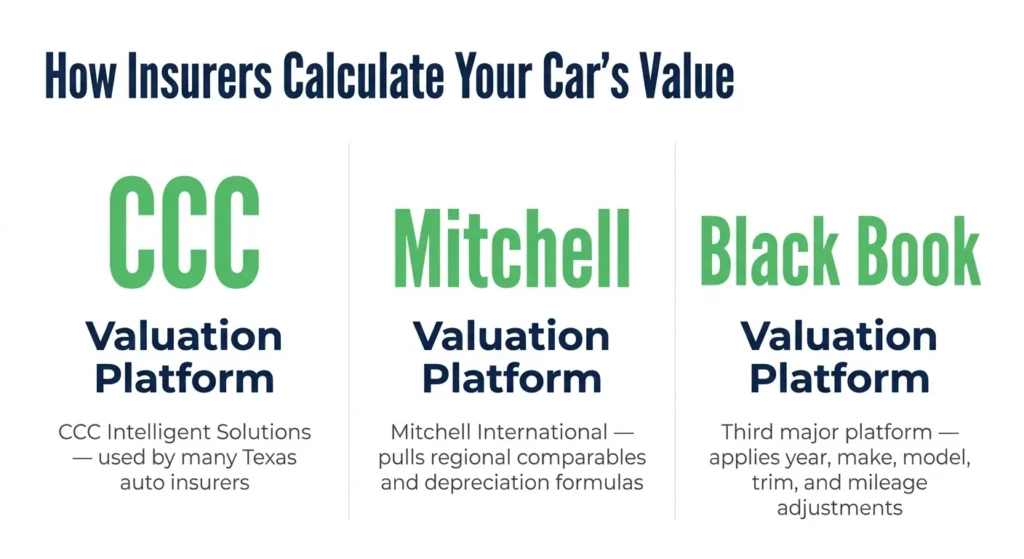

- Insurers use platforms, such as CCC Intelligent Solutions, Mitchell, and Black Book, to generate ACV reports for total loss claims.

- You can dispute a low ACV by gathering comparable listings and invoking the appraisal clause.

Another driver hit your car on the Southwest Freeway heading into Houston. The damage was severe enough that the insurer declared it a total loss. A few days later, you received their actual cash value (ACV) figure. The number was lower than you expected, and now you have to decide whether to accept it or push back.

What Is ACV?

Texas Transportation Code § 501.091 defines ACV as the market value of a motor vehicle immediately before the crash; this value is used as the foundation of every total loss settlement in the state.

Texas declares your vehicle a total loss when the cost to repair it, plus its salvage value, equals or exceeds its ACV. That comparison uses your vehicle’s pre-crash value, not what you paid for it or what you still owe on the loan.

Market value reflects what a willing buyer would have paid for a comparable vehicle in your area at the time of the car accident.

How Insurers Calculate Your ACV

The insurer does not determine your vehicle’s value by looking it up online. They run it through proprietary valuation software, and the number depends heavily on which data the platform uses and how it weights the inputs.

CCC Intelligent Solutions, Mitchell International, and Black Book are the three platforms Texas auto insurers use most often. Each pulls comparable vehicle listings from regional markets and applies depreciation formulas based on year, make, model, trim level, and mileage.

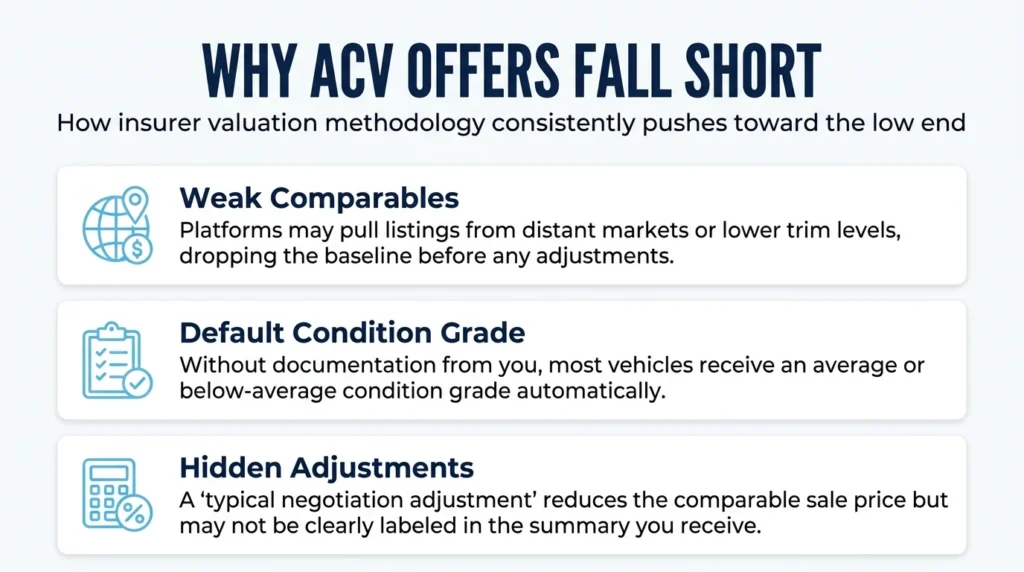

Insurers grade your vehicle’s condition on a scale from Excellent to Poor, adjusting its Actual Cash Value (ACV) accordingly. Without your documentation, adjusters will typically give your car an “average” or “below-average” grade by default.

Insurance companies often sneakily lower your car’s value using a “negotiation adjustment.” This discount isn’t clearly labeled in your final paperwork – it is usually buried as a line item deep inside the detailed report.

Why ACV Offers Often Fall Short

The insurance company’s final value is rarely a best-case scenario. Because every calculation they use works in their favor, their final offer usually lands at the absolute lowest end of what your car is actually worth.

Insurers often lower your car’s baseline value right from the start by choosing unfair “comparable” vehicles. They do this by pulling listings from cheaper geographic areas or selecting models with lower trim packages.

A low condition grade will drag your car’s value down. Even if your car was in great shape, the insurance company will likely grade it as average or worse unless you provide proof, like detailed service and maintenance records.

The rest of your car’s value is lost to depreciation. Insurance companies use general market averages to calculate this loss, meaning they won’t give you extra credit for a spotless maintenance history or a model that holds its value well in your local area.

How to Dispute Your ACV

You don’t have to accept the insurer’s first figure. If you believe the ACV is lower than what your vehicle was worth, you can push back with documentation.

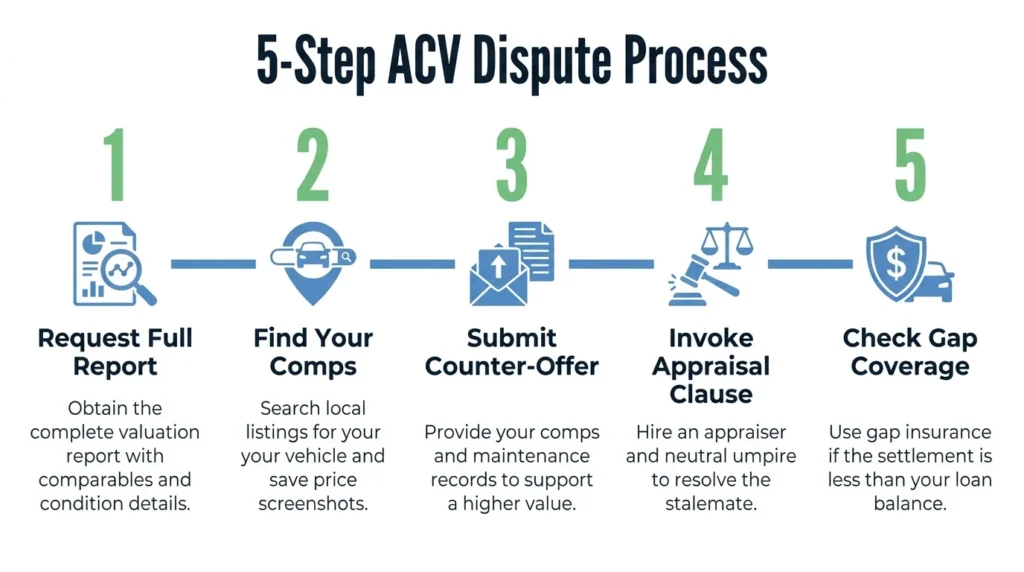

There are 5 steps you must take to dispute your ACV:

- Step 1: Request the full valuation report in writing. Ask the insurer to provide the complete report, including the comparable vehicles used, the condition grade assigned to your vehicle, and every adjustment applied. That document is the foundation of any counteroffer.

- Step 2: Gather your own comparable listings. Search regional used-vehicle sites for vehicles matching your year, make, model, trim level, and mileage range. Take dated screenshots of each listing and the asking price.

- Step 3: Submit a written counteroffer with documentation attached. Send the insurer your comparable listings along with any maintenance records, service receipts, or documentation supporting a higher condition grade. The insurer doesn’t have to accept it, but a written counter creates a record.

- Step 4: Invoke the appraisal clause if direct negotiation stalls. Most Texas auto policies include this provision: each party hires an independent appraiser, and a neutral umpire resolves any disagreement. If the insurer refuses to engage at all, you can also file a complaint through the Texas Department of Insurance consumer complaint process.

- Step 5 (optional): Check whether gap insurance applies. If the final ACV settlement falls below your remaining loan balance, gap insurance may cover the shortfall. For a full explanation of how gap coverage works in Texas, read about Texas gap insurance and total loss coverage.

Work with a Texas Injury Attorney

When the insurer’s ACV figure is lower than what your vehicle was worth, you don’t have to accept it as the final answer. An experienced attorney can assist you in fighting a lowball insurance offer.

Angel Reyes & Associates has spent more than 30 years representing crash victims across Texas. We have recovered more than $1 billion for our clients. We offer free initial consultations and take cases on a contingency basis, meaning you don’t pay unless we win. Contact us to talk through your total loss settlement options.

Past results do not guarantee future outcomes.

Actual Cash Value FAQs

How long does my insurer have to settle a total loss claim in Texas?

Under Texas Insurance Code Chapter 542, your insurer must acknowledge your claim within 15 calendar days, then accept or reject it within 15 business days of receiving all required documentation. Once the insurer accepts the claim, payment is due within 5 business days.

Can I keep my totaled car and still receive part of the ACV payout?

Yes. If you choose to keep the vehicle after a total loss, a process called owner retention, the insurer pays you the ACV minus the estimated salvage value. The car receives a salvage title, which limits how it can be sold or insured until it has been repaired and passed a state inspection.

Do aftermarket modifications or upgrades affect my ACV payout after a total loss?

Standard auto policies typically exclude equipment not installed by the manufacturer, so modifications often aren’t reflected in the base ACV figure. To recover their value, you need documentation showing the upgrades were professionally installed, and your policy may need a separate endorsement to cover them.

What is replacement cost coverage, and how does it differ from ACV?

Replacement cost coverage pays what it costs to replace your totaled vehicle with a comparable new or similar one, without subtracting depreciation. ACV coverage deducts depreciation from that figure, so the payout reflects what the vehicle was worth at the time of the crash, not the cost of buying a new one.

Can I dispute the insurer's repair estimate if I think it overstates the damage?

Yes. You can hire an independent body shop to provide a competing repair estimate. A lower estimate can bring the total below the threshold that triggers a total loss, which would mean your vehicle qualifies for repair rather than a total loss settlement.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 70,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...