Texas Minimum Motorcycle Insurance Requirements

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- Texas requires 30/60/25 motorcycle insurance, but liability coverage only protects others, not you.

- A $30,000 per-person bodily injury limit can be exhausted by a single night in a trauma center.

- UM/UIM coverage bridges the gap when the at-fault driver's limits don't cover your actual losses.

You bought a motorcycle policy because Texas requires one. The agent told you the numbers: 30/60/25. You paid the premium, got the proof of insurance card, and figured you were covered.

You are legal. But in a serious crash, “legal” and “covered” are not the same thing.

What Texas Insurance Law Requires

Texas law sets the minimum at $30,000 per injured person, $60,000 per accident for all bodily injury claims combined, and $25,000 for property damage. These numbers come from the Texas Transportation Code § 601.072, the Motor Vehicle Safety Responsibility Act, and they apply to every motor vehicle registered in Texas, including motorcycles.

What that coverage actually does is easy to misread. Liability insurance protects other people from you. If you cause a crash, your policy pays the injured party’s bills and property damage, up to those limits.

Your own medical bills and your motorcycle repairs are not covered under a basic liability policy.

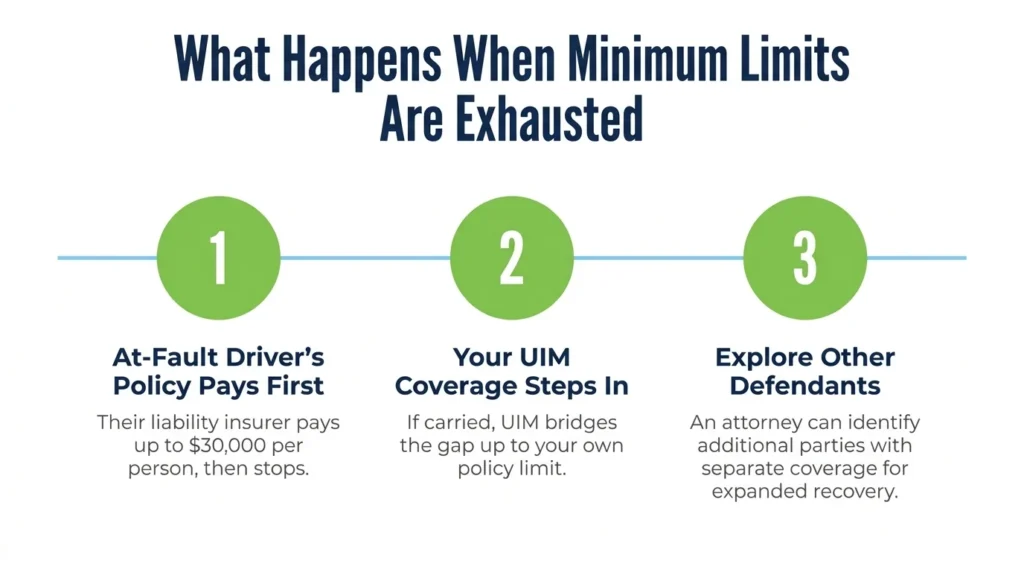

If the other driver causes the crash and they carry only the Texas minimums, their policy will pay toward your losses, up to $30,000 for your injuries. No more.

For a broader look at how Texas minimum coverage works across vehicle types, review the Texas minimum car insurance requirements.

Why Minimum Limits Fall Short in a Serious Crash

A $30,000 bodily injury limit sounds like real money until you spend two nights in a trauma unit.

Serious motorcycle injuries frequently involve traumatic brain injuries, spinal cord damage, multiple fractures, and extensive soft tissue damage. A single emergency room admission, stabilizing surgery, and a short inpatient stay can consume the entire $30,000 per-person limit before rehabilitation begins.

When the at-fault driver carries only the Texas minimum, their insurer pays your claim up to $30,000 and closes the file. Whatever your bills total beyond that amount is not their problem. If you also carry only minimum liability and no additional coverages, there is no other policy to turn to.

The property damage minimum also only works one direction. The $25,000 on your policy pays for damage you cause to someone else’s property; it does not repair or replace your own motorcycle.

Understanding how motorcycle accident settlements work in Texas helps clarify which policies apply to which losses after a crash.

Riders who face a gap between the at-fault driver’s policy limits and their actual medical costs have specific legal options worth understanding before accepting any settlement.

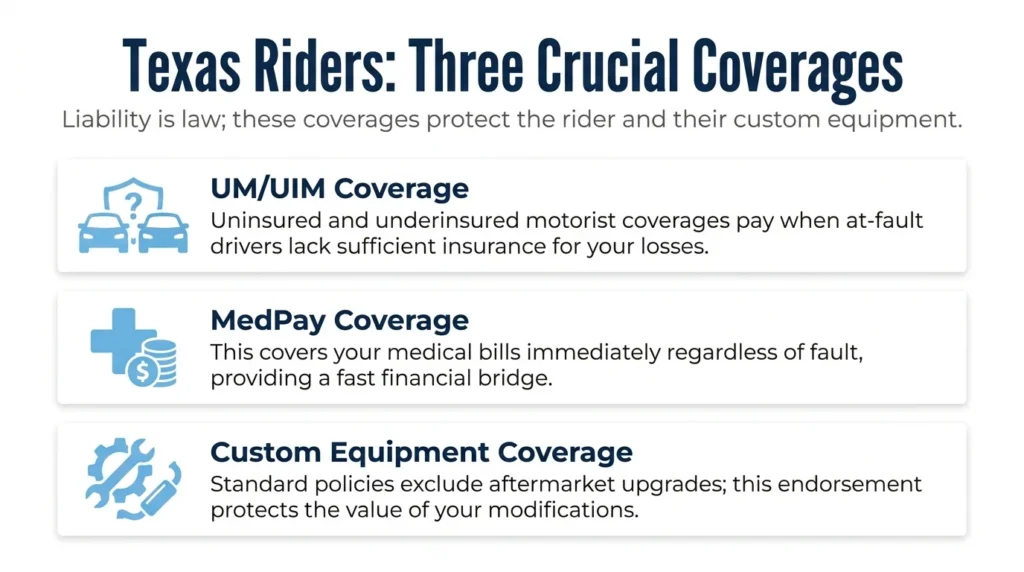

Coverage Riders Actually Need

Liability coverage is what Texas requires. The coverages below are what riders who want actual financial protection should consider adding.

UM/UIM Coverage

Uninsured motorist (UM) and underinsured motorist (UIM) coverage address the two most common coverage gaps riders face after a serious crash.

UM coverage pays you when the at-fault driver has no insurance at all. UIM coverage pays when the at-fault driver has insurance, but their limits are too low to cover your actual losses. If a driver with $30,000 in coverage causes you $90,000 in medical bills, UIM steps in to cover the difference, up to your own UIM limit.

Texas law requires every auto liability insurer to offer UM/UIM coverage under the Texas Insurance Code § 1952.101. You have this coverage unless you signed a written rejection when you purchased the policy.

If you are not sure whether your policy includes it, check your declarations page or call your insurer.

You can also review how UM/UIM claims work after a crash.

MedPay Coverage

Medical payments (MedPay) coverage pays your own medical bills regardless of who caused the crash. You do not need to prove fault or wait for liability to be determined. Your insurer pays covered medical expenses up to your MedPay limit as bills come in.

MedPay is narrower than personal injury protection (PIP): it covers medical expenses only, while PIP also covers a portion of lost wages. Neither is required in Texas, but both can fill the gap between what your health insurance pays and your actual out-of-pocket costs.

Custom Equipment Coverage

If your motorcycle has aftermarket modifications, a standard liability policy will not cover them. Chrome upgrades, custom exhaust systems, specialized seats, and other accessories have real value that a basic policy ignores.

A custom equipment or accessories endorsement covers the actual value of your modifications if the bike is damaged or totaled in a crash. Without it, you replace your customized bike with the payout for a stock version of the same model.

What Happens When Coverage Runs Out

When both the at-fault driver’s policy and your own policy limits are exhausted and bills remain, you are looking at a more complicated situation. The injured rider’s personal assets can be exposed to remaining medical debt without additional coverage to absorb it.

Getting Help After a Serious Motorcycle Crash

An attorney can assess whether other recovery options exist. Third-party defendants, commercial entities, or product liability claims may all be avenues depending on the facts of the crash.

Angel Reyes & Associates has helped injured Texas riders work through insurance coverage questions and personal injury claims for over 30 years. We handle motorcycle accident cases on contingency, meaning you pay no fee unless we recover compensation for you, and offer free consultations.

If you or someone you care about has been seriously injured in a motorcycle crash, reach out to us to discuss your options.

Past results do not guarantee future outcomes.

Texas Minimum Motorcycle Insurance FAQs

Does the $60,000 per-accident limit apply if I'm the only person injured?

No. The $60,000 limit is a cap on total bodily injury payments across all injured people in a single crash. If you are the only person injured, the per-person limit of $30,000 controls, not the $60,000 per-accident figure.

Will my motorcycle insurance cover my passenger's injuries if I cause the crash?

Your liability coverage can pay for your passenger’s injuries if you are at fault, up to the per-person bodily injury limit. Adding MedPay or PIP provides a faster, fault-free option to cover a passenger’s medical bills regardless of how liability is resolved.

If I financed my motorcycle, am I required to carry more than the minimum?

Most lenders require collision and comprehensive coverage on a financed motorcycle, on top of the state-required liability minimum. Once the loan is paid off, those additional coverages become optional, though riders who want protection for their own bike often keep them.

Can the other driver sue me personally if my liability limits don't cover all their damages?

Yes. If the damages from a crash you caused exceed your policy limits, the other party can pursue a personal judgment against you for the remaining amount. Higher liability limits reduce that exposure.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 55,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...