Hit-and-Run Motorcycle Accidents in Texas

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- A fleeing driver counts as uninsured, so your UM coverage becomes your main recovery path.

- The physical contact rule blocks UM property damage claims when the car never touched you.

- Texas gives you two years to file an injury claim, even if the driver is never found.

You were riding home through Deep Ellum one evening when a car drifted into your lane and clipped your bike. By the time you got off the pavement, the driver was already gone.

Now you are facing medical bills, a damaged motorcycle, and a question no one prepared you for. How do you get paid when the person who hit you has vanished?

Texas Law on Hit-and-Run Drivers

Leaving the scene of a crash is a crime in Texas, not just a rude move. A driver who hits you and flees has broken the law the moment they drive away.

Texas Transportation Code § 550.021 requires every driver to stop, render aid, and exchange information after a crash that causes injury, death, or property damage. A driver who runs commits a criminal offense.

The same code adds a second duty. Under Texas Transportation Code § 550.026, the driver must immediately report the crash to law enforcement, and the resulting official crash record is what you will need to file an insurance claim later.

The criminal side and your money are two separate tracks. Even if police catch the driver and charge them, a conviction does not put a dollar in your pocket. You have to pursue your own civil recovery path to get compensation.

The rules for a motorcycle hit-and-run share roots with crashes involving any vehicle. For the broader picture, our overview of Texas hit-and-run accidents walks through how the law treats fleeing drivers across all vehicle types.

UM Coverage for Motorcycle Riders in Texas

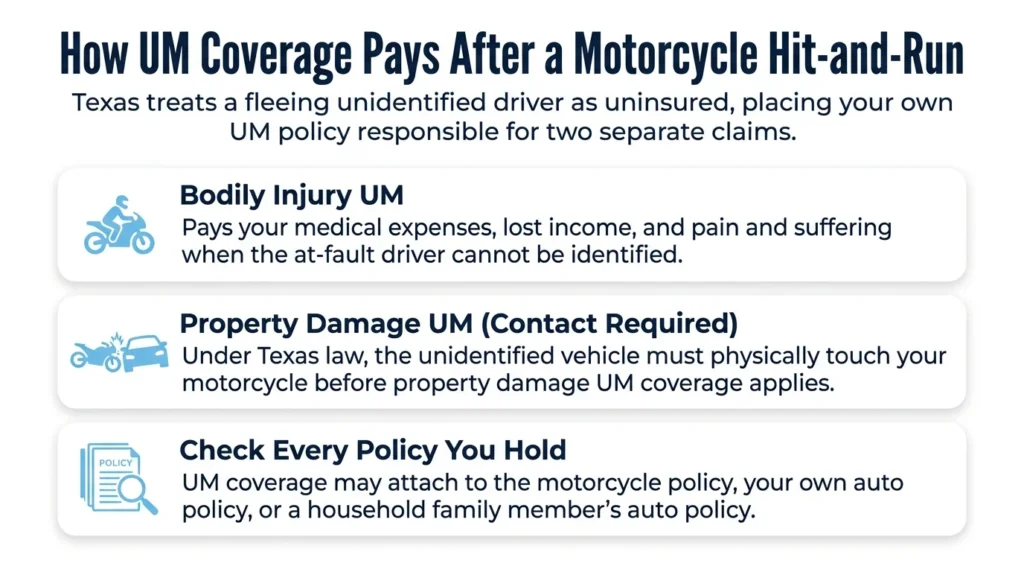

When the driver who hit you cannot be found, your own uninsured motorist coverage usually becomes your main way to recover. Texas treats a fleeing, unidentified driver as an uninsured motorist, which puts your own policy on the hook.

That coverage splits into two parts that follow different rules. One pays for your injuries. The other pays for your motorcycle, and it carries a catch many riders never see coming.

Our guide to uninsured motorist claims covers how this coverage works in plain terms.

Uninsured Motorist Bodily Injury Coverage

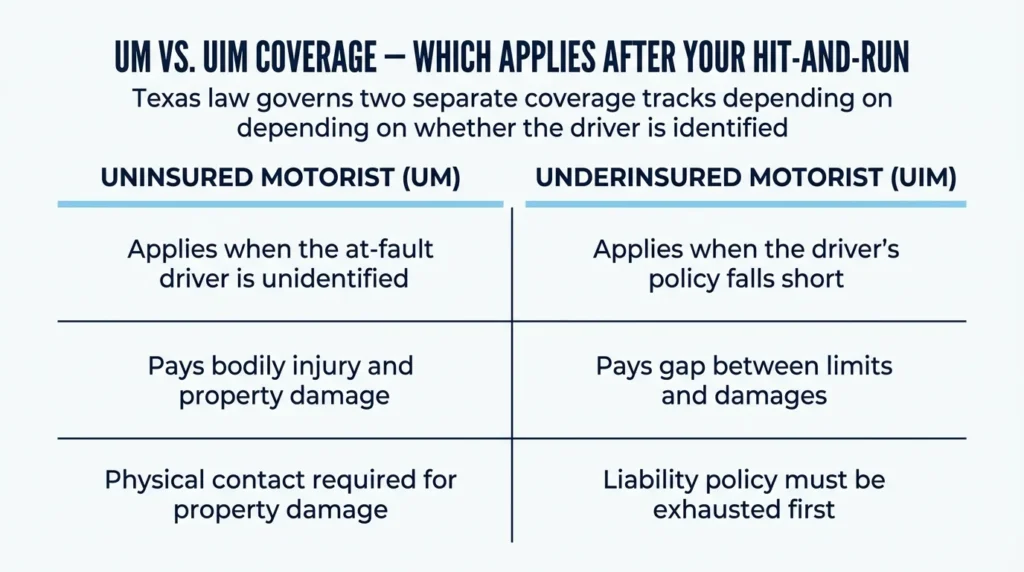

Your uninsured motorist bodily injury coverage pays for medical expenses, lost income, and other injury costs when the at-fault driver cannot be identified. Texas Insurance Code § 1952.101 treats that fleeing driver as uninsured, so your own insurer steps into their shoes.

Texas does not require a separate motorcycle UM policy. Any auto policy that does not exclude motorcycles may cover you, so pull your declarations page and check exactly what you carry.

If you are unsure what your coverage includes, the Texas Department of Insurance explains how UM coverage is structured and what to look for in your policy.

Uninsured Motorist Property Damage & the Physical Contact Rule

Here is the catch. Texas Insurance Code § 1952.104 requires that the unidentified vehicle actually touch your motorcycle before your property damage coverage will pay.

A “phantom vehicle” that runs you off the road without contact usually fails this test. If a car forces you down but never hits you, your property damage UM claim will likely be denied.

Texas courts have allowed indirect contact in narrow cases. One example is a chain-reaction crash, where the fleeing car strikes a second vehicle that then hits you. If that happened to you, document the exact sequence while it is fresh.

There is a different path if the driver is later identified but carries too little insurance. Underinsured motorist coverage under Texas Insurance Code § 1952.103 governs that situation, and it serves as your fallback once an identity is known.

For more on dealing with a driver who has no coverage, our guide on what to do after an uninsured driver hits you breaks down your next moves.

Steps to Identify a Fleeing Driver

Your best shot at finding the driver starts in the first minutes after the crash and runs through the days that follow. Move fast on these steps, because the evidence that identifies a vehicle disappears quickly.

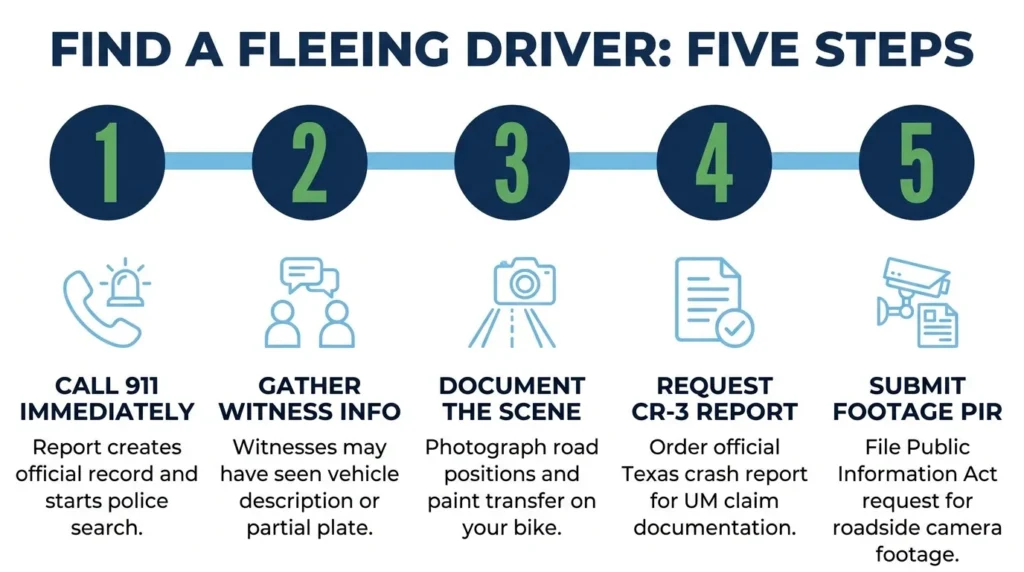

Step 1: Call 911 immediately. A police report creates the official CR-3 crash record you need for a UM claim, and it puts law enforcement to work trying to find the vehicle.

Step 2: Gather witness information. Get names, phone numbers, and what each person saw. Riders sit lower than drivers, so a nearby witness may have caught a partial plate or vehicle description you never could.

Step 3: Document the scene. Photograph road positions, skid marks, and debris. Capture any paint transfer on your bike, since the color and make of the fleeing car can show up right there on your frame.

Step 4: Request the CR-3 crash report. The official Texas crash report is available through TxDOT’s crash records portal (https://www.txdot.gov/data-maps/crash-reports-records.html) and serves as core documentation for your claim.

Step 5: Submit a Public Information Act request for traffic camera footage. TxDOT keeps footage from roadside cameras, but it gets overwritten on a rolling cycle. File your request promptly through TxDOT’s open records portal, a process the Texas Government Code § 552.001 authorizes for public records.

Step 6: Canvas nearby businesses for private footage. Gas stations, intersections, and parking lots often run cameras that catch what public road cameras miss. An attorney who knows hit-and-run evidence recovery can move on surveillance requests before that footage is lost.

Preserving every scrap of evidence matters more for riders than most. National motorcycle safety data shows how exposed riders are in a crash, and our look at Texas motorcycle accident statistics puts those risks in a local frame.

Compensation When the Driver Is Never Found

If your search comes up empty, your bodily injury UM coverage remains your main path to compensation. It can pay for medical bills, lost wages, and pain and suffering up to your policy limits, with your own insurer standing in for the driver who fled.

Our breakdown of how motorcycle accident settlements work in Texas shows what that recovery can look like.

Property damage is the harder piece. Without physical contact between the at-fault vehicle and your bike, your property damage UM claim will likely be denied, so read your policy’s exclusion language closely.

Do not stop at UM coverage when you count your options. Health insurance and MedPay can pay medical expenses on their own, no matter how the UM claim turns out. Inventory every coverage you hold before you decide nothing is available.

A hard deadline sits over all of this. Texas Civil Practice and Remedies Code (CPRC) § 16.003 gives you two years to file a personal injury claim, and that clock runs even when the driver is never named.

Tell your insurer about the hit-and-run as soon as you can. Late notice can trigger policy defenses and tangle your claim even when the facts are plainly on your side. An attorney can help you work through UM requirements, insurer pushback, and coverage limits when the at-fault driver has disappeared, which you can read more about on our motorcycle accident page.

Work with a Texas Motorcycle Injury Lawyer

A hit-and-run leaves you chasing a stranger while the bills pile up, and you should not have to chase your own insurer too. Angel Reyes & Associates has stood with injured Texas riders for over 30 years.

We handle motorcycle hit-and-run claims on contingency, so there is no fee unless we win. Our team has more than $1 billion recovered for clients across Texas, offers free initial consultations, and answers the phone 24/7.

You can reach out to us for a free consultation and learn more about our team before you decide anything.

Past results do not guarantee future outcomes.

Uninsured Motorist Motorcycle Accident FAQs

Does Texas require UM coverage on a motorcycle policy?

Texas requires insurers to include UM coverage in every policy unless the rider rejects it in writing. If you never signed a written rejection, your policy likely carries UM coverage even if you did not specifically request it.

Can I file a UM claim under a family member's policy if I don't carry my own?

Texas UM coverage generally extends to family members who live in the same household as the policyholder. If you were riding your own bike but live with a family member who has UM coverage and did not exclude motorcycles, that policy may cover your injuries.

Will filing a UM claim for a motorcycle hit-and-run raise my insurance rates in Texas?

Texas law protects you from rate increases for no-fault claims, including UM claims where another driver fled the scene. Your insurer may still review your overall risk profile at renewal, but the UM claim itself should not trigger a surcharge.

What happens to my UM claim if the hit-and-run driver is identified later?

If the driver is found and carries liability insurance, that policy becomes the primary source of payment and your UM claim shifts to a UIM claim for any gap between their limits and your total damages. Your insurer may also pursue the at-fault driver directly through subrogation to recover what it paid you.

Does UM coverage apply if the hit-and-run happened in a parking lot?

Yes. Texas UM coverage applies to crashes on private property, including parking lots, as long as your policy does not exclude private-property accidents. Report the crash to law enforcement and your insurer the same way you would for a crash on a public road.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 70,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...