How Deductibles Work in Texas

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- Your deductible is what you pay out of pocket before your insurance covers the rest of a claim.

- Texas policies have separate deductibles for collision and comprehensive, and you can set each one.

- A higher deductible lowers your premium but means more cash out of pocket after a wreck.

How Deductibles Work in Texas

You just filed a claim after a fender-bender on I-35, and now your insurer says you owe $500 before they pay anything. That $500 is known as your deductible, the amount you pay out of pocket each time you file a covered claim.

The overwhelming majority of auto insurance policies have deductibles. Understanding how they work helps you figure out how much you should receive when settling a claim so you can accurately budget for repairs.

What Is an Auto Insurance Deductible?

A deductible is the fixed dollar amount you agree to pay toward a covered loss before your insurance kicks in. For example, if your repair bill is $3,000 and your deductible is $500, your insurer will pay $2,500 after you cover the first $500.

Texas insurers typically offer deductible options ranging from $250 to $2,500. The amount you choose when you buy your policy stays the same until you change it. You can adjust your deductible amount at renewal or mid-policy if needed.

You pay your deductible each time you file a claim, not once per year. Two claims in one year would mean two deductible payments. This matters if you are juggling bills after a wreck; knowing your deductible amount helps you plan for out-of-pocket costs before you miss work or delay repairs.

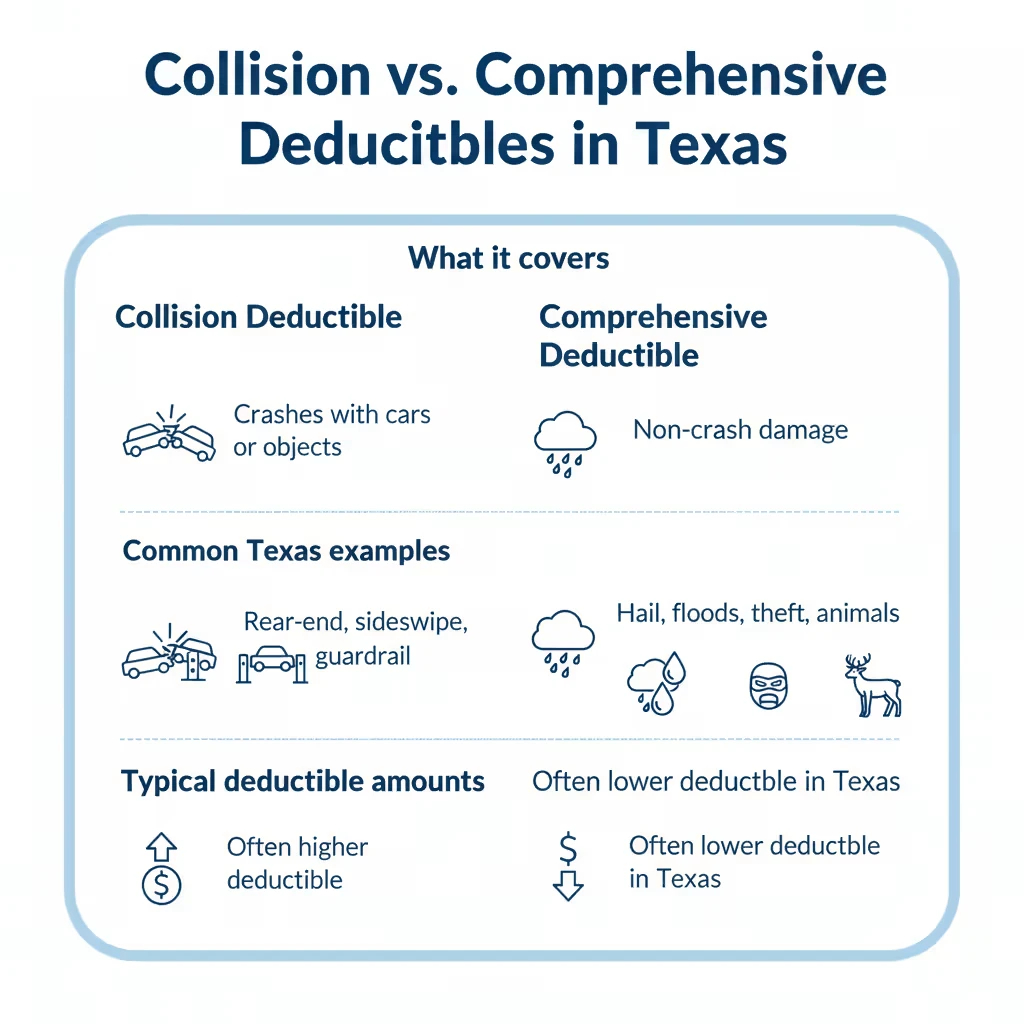

Collision Deductible vs. Comprehensive Deductible

Most Texas auto policies include two types of coverage, collision and comprehensive, and each has its own deductible. Collision covers damage from crashes. Comprehensive covers everything else: weather, theft, or animal damage. You can set different amounts for each deductible. Many Texans choose a higher collision deductible to lower premiums while keeping their comprehensive deductible low for weather-related claims.

Collision Deductible

Your collision deductible would apply when your car hits another vehicle or object. This includes rear-end crashes, sideswipes, and single-car accidents where you hit a guardrail or pole.

If another driver caused the wreck, you may be able to recover your deductible from their insurance. But you will often pay it upfront to get repairs started.

Comprehensive Deductible

Texas is no stranger to extreme weather. Vehicle damage from flash floods, high winds, and hailstorms falls under comprehensive coverage. Additionally, damage from animals (such as hitting a deer while driving on a rural road at night), vandalism, or vehicle theft are also covered under your comprehensive policy.

A $100 or $250 comprehensive deductible is common in hail-prone areas throughout Texas.

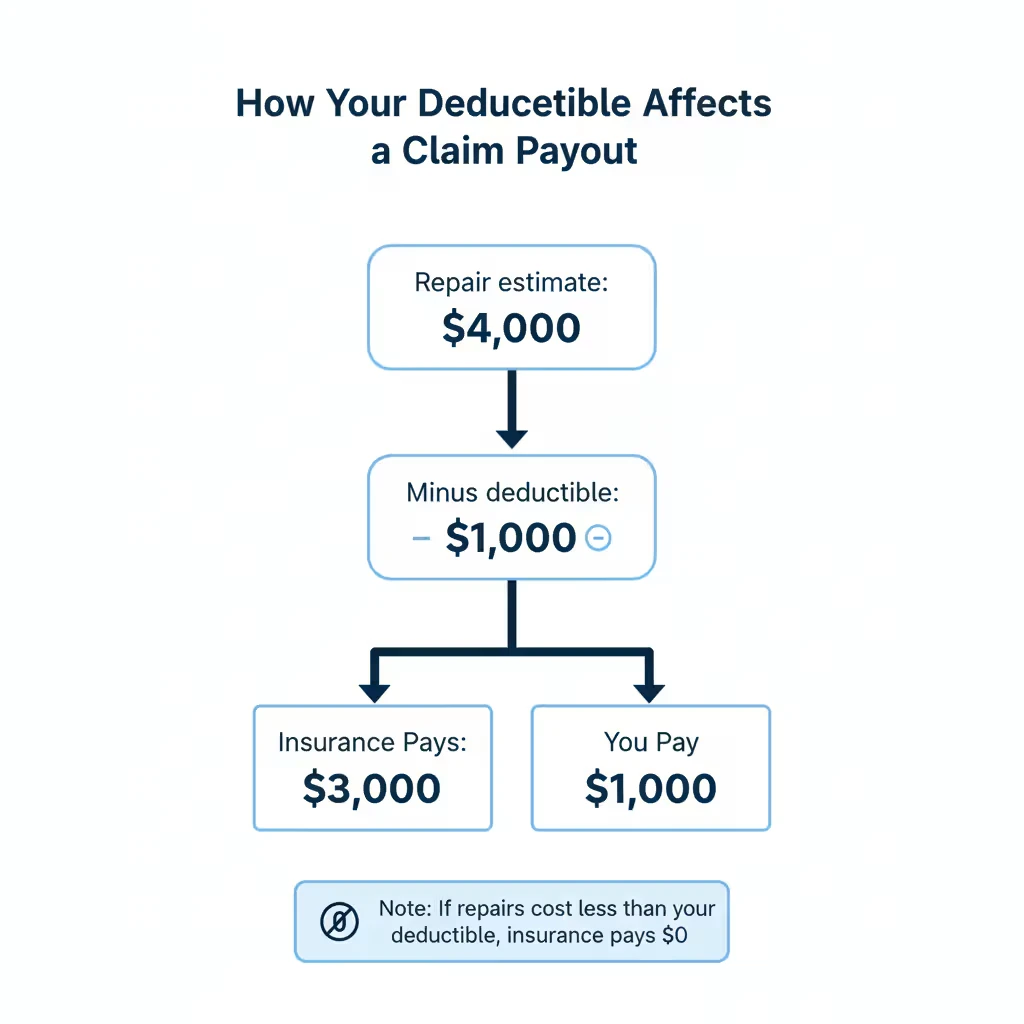

How Your Deductible Affects Claim Payouts

Your insurer subtracts your deductible from the claim payout. The higher your deductible, the less your insurer pays.

Here is how it works:

- Repair estimate: $4,000

- Your deductible: $1,000

- Insurer pays: $3,000

- You pay: $1,000

If the damage is less than your deductible, filing a claim may not make sense. You would pay the full repair cost yourself.

Filing small claims can also raise your premiums. A claim stays on your record and can continue to impact your premiums for three to five years.

When another driver is at fault, their liability insurance should cover your damages without you paying a deductible. But their insurer may delay or dispute the claim, so you might use your own collision coverage and pay your deductible to get repairs done faster.

You can then seek reimbursement of your deductible from the at-fault driver’s insurer through subrogation. Your insurance company handles most of the legwork, but it can take weeks or months to resolve.

Choosing the Right Deductible in Texas

Once you understand how deductibles affect payouts, the next question is whether your current deductible fits your budget. Your deductible choice affects both your monthly premium and your out-of-pocket costs after a car accident. If you are reviewing your policy or recovering from a claim, this is a good time to check whether your amounts still make sense.

Higher Deductible

A higher deductible lowers your monthly premium. This works well if you have savings to cover a $1,000 or $2,000 expense after an accident.

If paying that amount would strain your budget, a lower deductible may be smarter. However, a lower deductible also means a higher monthly premium, so it’s important to get quotes and run the numbers for yourself.

Lower Deductible

A lower deductible means higher monthly premiums. You pay more each month but less out of pocket when you file a claim.

A lower deductible helps if you cannot easily cover a large unexpected expense. It also makes sense if you drive frequently on busy Texas highways where accidents are more common.

Here are some great questions to ask yourself:

- Can I afford my deductible amount today if I had a wreck?

- How often do I drive in high-risk conditions?

- Do I park outside where hail or theft is more likely?

Review your deductible amounts at each policy renewal. Your financial situation and driving habits may change.

When to Contact an Attorney

If the other driver’s insurer refuses to pay or drags out the process, you may struggle to recover your deductible. If you suffered injuries, medical bills can add another layer of complexity. For guidance on handling conversations with the other driver’s insurer, see Should I Talk to the Other Driver’s Insurance Company.

An attorney from our skilled and highly experienced team at Angel Reyes & Associates can help you pursue the at-fault driver’s insurance for your deductible, repair costs, and injury-related damages. We have guided Texans through situations like this for over 30 years. If your claim is disputed or involves injuries, request a free consultation to help you understand your options.

Insurance Deductible FAQs

Do I pay my deductible if the other driver was at fault?

If the other driver was at fault, you should not have to pay a deductible when filing against their liability insurance. But if you use your own collision coverage to speed up repairs, you will have to pay your deductible first and seek reimbursement later through subrogation.

Can I change my deductible after an accident?

You can change your deductible after an accident, but the new amount only applies to future claims. It will not affect a claim you have already filed.

What happens if my repair cost is less than my deductible?

If your repair cost is less than your deductible, your insurer pays nothing. You cover the full repair cost yourself. Filing a claim in this situation could raise your premiums without any payout benefit.

Does a police report affect my deductible?

A 5A police report does not change your deductible amount, but it can help prove fault and support your claim against the other driver’s liability insurance. For more on when you need a police report, see Do You Need a Police Report for Insurance Claims in Texas.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 70,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...