How Collision Coverage Works After a Crash in Texas

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- Collision coverage pays to repair or replace your own vehicle after a crash, regardless of fault, minus your deductible.

- You can often choose between filing a collision claim with your insurer or a liability claim with the at-fault driver’s insurer.

- Your insurer may recover your deductible through subrogation if the other driver was at fault and has sufficient coverage.

How Collision Coverage Works After a Crash in Texas

You were rear-ended in rush hour traffic on I-35 near downtown Austin. Your car is damaged, and now you’re wondering who pays for repairs. Your insurance company is asking questions, the other driver’s insurer hasn’t called back, and you need answers about how all of this is supposed to work after a wreck.

While the other insurance company seems to be dragging their feet, you can at least get your car repair started by filing a claim with your collision coverage on your auto policy.

What Collision Coverage Is & What It Pays For

Collision coverage pays to repair or replace your own vehicle after a crash. It applies regardless of who caused the accident. This is different from liability insurance, which pays for damage you cause to others.

When your car hits another vehicle, strikes an object, or rolls over, collision coverage can help cover the cost of fixing it. It pays up to your vehicle’s actual cash value, minus your deductible. Your insurer handles the claim directly with you.

Collision coverage does not pay for the other driver’s car, your medical bills, or mechanical problems unrelated to the crash. Those costs fall under other coverages or the at-fault driver’s liability policy.

Collision coverage is optional under Texas’s minimum insurance laws, but that doesn’t mean you aren’t required to have it. If you finance or lease your vehicle, your lender almost certainly requires you to carry collision and comprehensive coverage in addition to minimum liability. You can verify your coverage details on your policy’s declarations page.

When Collision Coverage Applies After a Texas Crash

Collision coverage typically applies after collisions with another vehicle, with a different object (i.e. a curb, wall, or parking lot bollard), or in a solo rollover crash. Your vehicle must be damaged in an incident to file a claim with your collision policy.

If your vehicle is damaged beyond repair, you can still file a collision claim; your insurer will simply pay out up to the cash value of your vehicle.

If you only carry liability insurance, you won’t have collision coverage to use. Drivers with financed or leased vehicles typically have collision because lenders require it.

Before filing a collision claim, confirm these basics:

- Your policy is active

- Collision coverage is included

- The damaged vehicle is listed on your policy

- The damage resulted from a collision or rollover

Some situations can complicate claims. If someone else who is excluded from your policy was driving the car at the time of the accident, or if the vehicle was used for commercial purposes, your insurer may have questions. These issues don’t automatically mean denial, but they can slow things down.

How Collision Deductibles Work

A deductible is the amount you pay out of pocket before your collision coverage kicks in. Common deductibles for collision policies range from $250 to $1,000 or more.

Here’s a simple example:

- Repair cost: $4,000

- Your deductible: $500

- Insurer pays: $3,500

You can either pay your deductible directly to the repair shop, or your insurer will subtract it from your settlement check. Either way, it comes out of your pocket first.

Can You Get Your Deductible Back?

Some people are hesitant to go through their own collision policy if they don’t believe they are at fault for an accident since it means paying their deductible out of pocket. However, there is some good news: you may be able to get your deductible payment back.

If the other driver was at fault, your insurer may pursue reimbursement from them or their insurance company through a process called subrogation. If they are successful, you may get your deductible back.

Recovery depends on several factors:

- Whether fault is clearly established

- Whether the other driver has insurance

- Whether their policy limits are sufficient

- How long the investigation takes

In hit-and-run cases or crashes involving uninsured drivers, recovering your deductible becomes more difficult. Keep your deductible payment receipt and all repair documentation in case reimbursement becomes possible later.

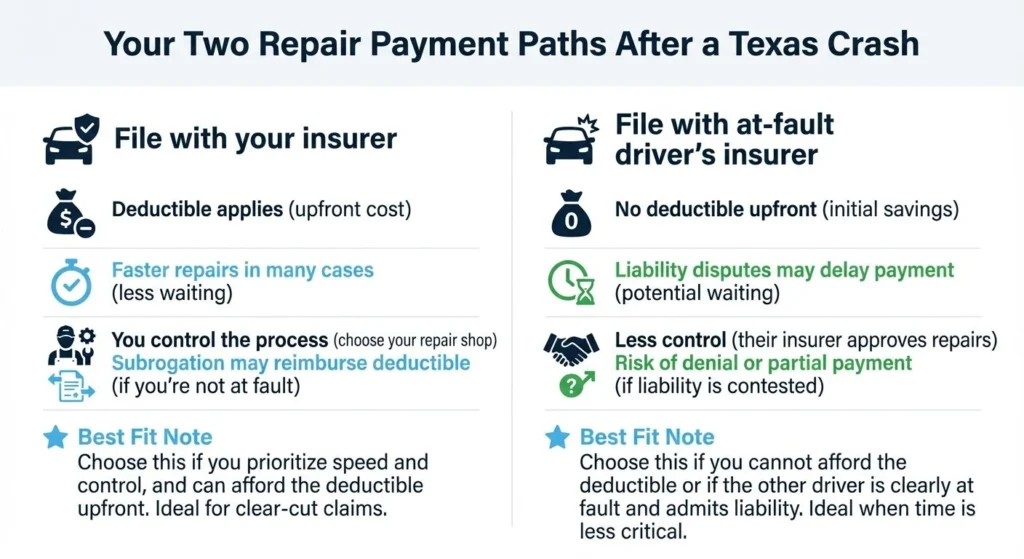

Collision vs. the At-Fault Driver’s Liability

Texas follows a fault-based insurance system. The driver who caused the crash is responsible for damages. Their liability insurance should pay for your vehicle repairs and other losses.

But here’s the reality: you can have two paths running at the same time.

| First-Party Claim (Your Collision) | Third-Party Claim (Their Liability) |

| Filed with your insurer | Filed with at-fault driver’s insurer |

| You pay your deductible | No deductible from you |

| Faster processing typically | May involve delays or disputes |

| Subrogation may recover costs | Direct payment if liability is clear |

When you use your collision coverage, your insurer pays you and then pursues the at-fault driver’s insurer for reimbursement. This subrogation process happens behind the scenes and may eventually return your deductible.

Should You Use Collision If the Other Driver Was at Fault?

This is one of the most common questions after a crash. In Texas’s fault-based system, the at-fault driver’s liability insurance should pay for your vehicle damage. However, that process isn’t always fast, and you could be stuck without a vehicle for some time while the investigation is ongoing.

Reasons to use your collision coverage:

- Faster repairs (you don’t wait on the other insurer’s investigation)

- More control over the repair process

- You are protected if fault is disputed or the other driver is uninsured

Potential drawbacks:

- You must pay your deductible upfront

- Your premium may be affected (though this varies by insurer and circumstances)

If liability is clear and the other driver’s insurer is responsive, filing a third-party claim with them can help you avoid paying a deductible. But if there’s any dispute or delay, using your collision coverage gets your car fixed while your insurer handles the rest.

Filing a Collision Claim: Step by Step

Here’s a practical workflow for filing your collision claim in Texas:

Immediately after the crash:

- Check for injuries and call 911 if needed

- Move to safety if possible

- Exchange information with the other driver

- Document the scene with photos

- Get contact information from witnesses

- Request a police report if officers respond

Starting your claim:

- Contact your insurance company to report the crash

- Provide your policy number, vehicle information, and crash details

- Schedule an inspection or get a repair estimate

- Choose a repair shop (your policy may have guidelines)

During repairs:

- Stay in contact with the adjuster

- Review any supplemental estimates if additional damage is found

- Keep all receipts for towing, storage, and related expenses

The Texas Department of Insurance FAQ provides additional guidance on what to expect during the claims process.

If Your Car Is Totaled

When repair costs exceed your vehicle’s value, your insurer may declare it a total loss. In that case, collision coverage pays the actual cash value of your car, minus your deductible.

If you have a loan or lease, the lienholder gets paid first from the settlement. This can leave you owing money if your loan balance exceeds the vehicle’s value. That’s where gap coverage helps. It covers the difference between what you owe and what the insurer pays.

If you believe the total loss valuation is unfair, you can request documentation of how the value was calculated and provide evidence of comparable vehicles. When disputes arise, speaking with a car accident attorney can help you understand your options.

When to Talk to a Texas Car Accident Attorney

Even when your main concern is vehicle damage, insurance issues can get complicated. Consider speaking with an attorney if you’re dealing with:

- Disputed liability

- A settlement offer that seems too low

- Total loss valuation disagreements

- Injuries in addition to vehicle damage

- An uninsured or underinsured driver

- Delays or denials from the insurance company

At Angel Reyes & Associates, we’ve helped Texas drivers navigate insurance claims for over 30 years. We offer free consultations and work on contingency, meaning you pay no fee unless we win. We have 16 locations across Texas and can handle most of your case remotely.

If you have questions about your collision claim or believe you’re not being treated fairly, reach out to us today to discuss your situation.

Collision Coverage FAQs

Does filing a collision claim in Texas affect my insurance rates even if I wasn’t at fault?

It can, depending on your insurer’s underwriting rules, but many companies are less likely to raise rates for not-at-fault claims; you should review your policy or ask your carrier directly.

Can I choose my own repair shop when using collision coverage in Texas?

Yes, Texas law allows you to choose your repair shop, although your insurer may recommend preferred shops that streamline the process. However, you are not obligated to go to them.

What happens if my repair costs end up being higher than the initial estimate?

If additional damage is found, the repair shop typically submits a supplemental estimate to your insurer, who may approve additional payments under your collision coverage.

Will collision coverage pay for a rental car while my vehicle is being repaired?

Not by itself. Rental reimbursement is a separate optional coverage, so you would need to have purchased that policy add-on for those costs to be covered. If you haven’t, it’s worth looking into—it usually only costs a few dollars extra per month.

How long does it usually take to resolve a collision claim in Texas?

Timelines vary, but first-party collision claims are often resolved faster than third-party claims, especially when liability is unclear or the other insurer delays.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 70,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Graham Griffin

Editor

Graham Griffin is the Web & Content Manager at Angel Reyes & Associates, where he oversees content strategy, AI-powered workflows, a...

Spencer Browne

Reviewer

Spencer Browne is a partner at Angel Reyes & Associates and a Board Certified personal injury trial lawyer with nearly 100 jury trials a...