How Commercial Truck Insurance Works in Texas

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- Federal regulations, multiple liable parties, and higher financial stakes push commercial truck insurers to defend aggressively against claims.

- Texas Insurance Code Chapter 542 requires insurers to acknowledge claims within 15 business days and imposes an 18% annual penalty for delay.

- Critical evidence including ELD data and dashcam footage can disappear quickly without a formal preservation letter.

When a commercial truck hits your car on I-10 near Houston, the insurance process that follows is nothing like anything you have dealt with before. The trucking company does not wait. Its insurer already has a team moving. Understanding what is happening on their side — and what your rights are — is the first step to protecting your claim.

Why a Truck Insurance Claim Looks Nothing Like a Car Accident Claim

Most people who have filed an auto insurance claim before assume a truck accident works the same way, just with a bigger vehicle. It does not. Commercial truck insurance is structurally different.

Federal regulations under 49 CFR Parts 387 and 390 govern commercial carriers and their insurance obligations. That means there is a layer of federal regulatory compliance on top of Texas state law that simply does not exist in a personal auto claim.

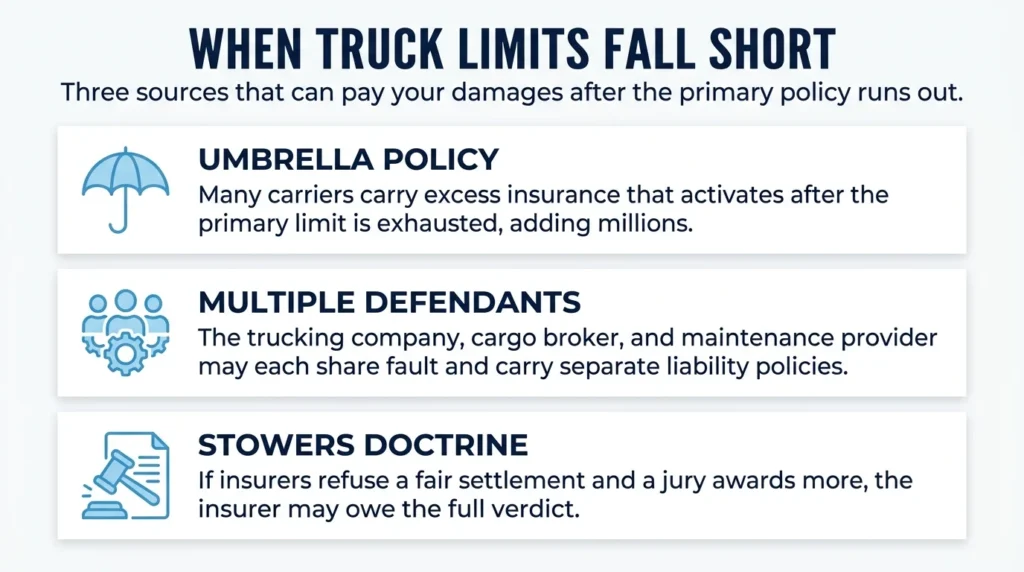

Liability in a truck crash also spreads across more parties. The driver, the trucking company, a trailer leasing company, a cargo broker, and a third-party maintenance provider may each hold some share of fault and may each carry a separate insurance policy. Every one of those policies has its own insurer, its own claims team, and its own interest in minimizing what it pays.

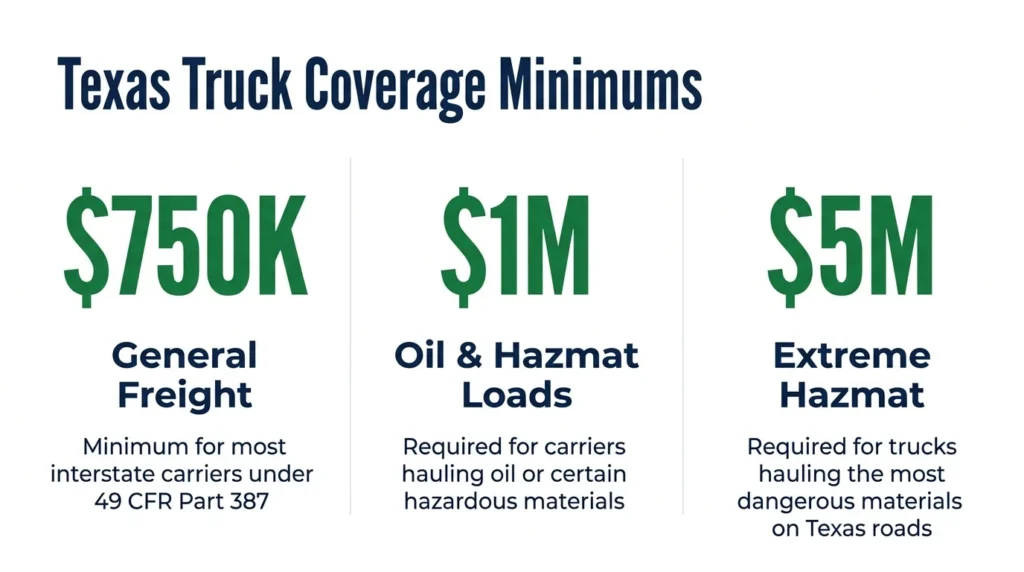

Finally, commercial truck policies carry limits of $750,000 to $5,000,000 or more. That is not generosity. Those limits create a powerful financial incentive for the insurer to contest your claim aggressively.

Who Is on the Insurer’s Side After a Crash

The entity primarily responsible for covering crash victims is the carrier’s commercial auto liability insurer. But the picture is more complicated than one insurer and one policy.

Many large carriers operate under a self-insured retention arrangement, where the trucking company itself absorbs claims up to a defined threshold before the external insurer gets involved. In those cases, the company controls the early investigation and negotiation directly, with no independent insurer reviewing decisions.

Interstate carriers are required under 49 CFR Part 387 to carry an MCS-90 endorsement on their policy. That endorsement is a federal guarantee: the insurer will pay accident victims up to the required federal minimum even if the policy contains exclusions that would otherwise deny coverage. It is a protection for injured parties, not for the carrier.

Defense counsel is retained by the insurer the day of the crash or shortly after. If you have not yet hired an attorney, you are negotiating alone against a team of experienced professionals whose job is to reduce what you receive.

How the Trucking Company’s Adjuster Investigates

When the carrier’s adjuster calls you, they are not there to help. They work for the insurer, and their assignment is to document your claim and limit the company’s exposure.

Adjusters collect police reports, scene photographs, witness statements, dashcam footage, and electronic logging device data. They are trained interviewers who know what questions produce statements that cap claims. They may sound conversational and sympathetic. Their notes go directly to the insurer’s defense file.

Texas law does not require an injured third party to give a recorded statement to the opposing insurer. That is your right. Early recorded statements frequently understate injuries because the full extent of harm is not yet apparent. Once given, that statement is in the file and can be used to challenge the value of your claim.

However, in many cases, you do not have to give a recorded statement to the other insurance company under Texas law. Instead, you are allowed to request that they submit their questions to you in writing.

Adjusters may also offer a quick settlement early in the process, before medical treatment is complete and before the long-term consequences of your injuries are known. Accepting that offer ends the claim permanently. Future costs are not recoverable once a release is signed.

What Texas Law Requires of the Insurer

Texas law does impose real, enforceable obligations on the insurer. Texas Insurance Code Chapter 542 governs the prompt payment of claims. Under that statute:

- The insurer must acknowledge your claim in writing within 15 business days of receiving written notice

- The insurer must accept or deny your claim within 15 business days of receiving all required documentation

- Once accepted, the insurer must deliver payment within 5 business days

Violations are not free. An insurer that delays beyond those deadlines must pay an 18% annual penalty on the claim amount plus attorney’s fees. That penalty is designed to deter delay tactics and gives you leverage when an insurer drags its feet.

Texas Transportation Code Section 550.021 separately requires the truck driver to stop, identify themselves, and provide aid after a crash. The carrier cannot waive that obligation even if it disputes fault.

Evidence That Disappears Fast After a Truck Crash

One of the most important differences between a truck claim and a standard auto claim is how much evidence exists after a truck crash and how quickly it can disappear. Commercial trucks generate digital data that standard passenger vehicles do not.

- Electronic logging devices record hours of service and driving patterns.

- The engine control module captures speed, braking, and throttle input at the moment of impact.

- Dashcams installed in cabs and on trailers record footage on rolling loops that may overwrite within days.

- Driver qualification files contain training history, licensing records, and medical certifications that speak directly to the driver’s fitness to operate the vehicle.

Federal regulations under 49 CFR Part 390 require carriers to maintain accident records, but federal retention obligations do not prevent spoliation without a formal litigation hold. ELD data may be gone within six months. Dashcam footage may be gone within days.

Sending a preservation letter to the carrier immediately after the crash creates a legal obligation to retain all relevant records and signals that litigation may follow. That letter is one of the first things a truck accident attorney sends at the start of a truck accident claim timeline.

Injured In an Accident? Talk to a Lawyer

Commercial truck insurance claims involve federal regulations, multiple overlapping insurance policies, and defense teams working from the first hours after a crash. The insurer’s side is organized, experienced, and well-funded. Getting an attorney involved early levels that imbalance.

Angel Reyes & Associates has handled truck accident cases across Texas for over 30 years. We have recovered more than $1 billion for clients and offer free consultations with no fee unless your case is resolved in your favor. If you were seriously hurt in a truck accident and want to understand your rights before talking to the adjuster, contact us today.

Past results do not guarantee future outcomes.

Commercial Truck Insurance FAQs

How long does a commercial truck insurance claim take to resolve in Texas?

Most claims take six months to two years. Serious injuries, disputed liability, or multiple insurers extend that timeline. Investigation of ELD data, driver records, black box data, medical documentation can take months. Litigation adds a year or more.

What is an MCS-90 endorsement and how does it protect me?

The MCS-90 is a federal endorsement required on interstate carrier policies. It guarantees the insurer pays accident victims up to the federal minimum even if policy exclusions would otherwise block coverage. It protects crash victims, not the carrier.

What if the trucking company says it is self-insured?

Self-insured carriers cover claims from their own funds, meaning the company controls its own investigation and negotiation. They can still be held fully liable. An attorney can confirm self-insurance status and identify any excess coverage above the self-insured threshold.

Can I file a claim against more than one party after a truck accident?

Yes. Fault may be shared across the driver, trucking company, trailer lessor, cargo broker, or maintenance provider. Each carries separate coverage, and you can pursue all of them simultaneously. Identifying every liable party early is critical.

What happens if I miss the deadline to file a truck accident lawsuit in Texas?

Texas gives injury victims two years from the accident date to file suit. Missing that deadline almost always eliminates your right to recover, no matter how strong your case. Government entity claims may have shorter deadlines. The clock starts at the crash.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 55,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...