How Commercial Insurers Investigate Truck Accidents

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

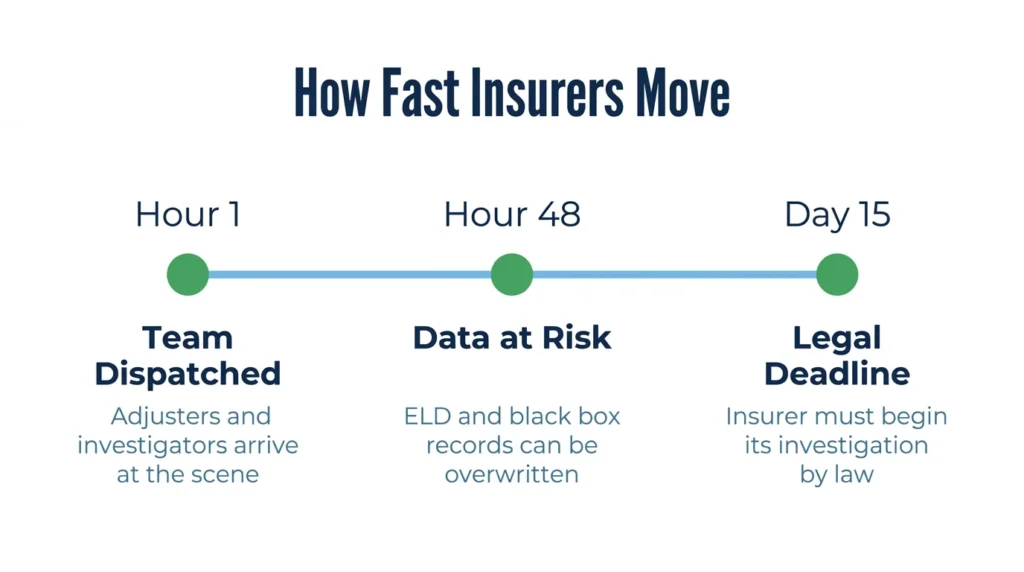

- Commercial insurers often dispatch rapid-response investigators within hours of a Texas truck crash to collect ELD data, black box records, and driver files.

- ELD and black box data can be overwritten within 14 to 30 days, so a formal preservation letter should go out within 48 hours of the crash.

- Under Texas law, insurers must begin investigating within 15 business days. Delays can trigger an 18% annual penalty under the Prompt Payment of Claims Act.

How Commercial Insurers Respond to a Crash

After a serious truck crash in Texas, a claims adjuster from the trucking company leaves a message on your voicemail. You are still in the emergency room, but the commercial insurer is already starting their investigation just a few hours later. By the time you are discharged, their team is already collecting evidence.

Understanding how their investigation works will put you in a better position to protect your claim.

When a commercial truck is involved in a serious crash, the carrier’s insurer typically dispatches a rapid-response team within a few hours. This team includes claims adjusters, defense attorneys, accident reconstruction specialists, and investigators. Their job is to document the scene, download electronic data, and build a defense file before the injured party has retained legal counsel.

The rapid-response model is standard practice for carriers that move significant amounts of freight in Texas. These teams arrive before roads are cleared, witnesses leave the scene, and the truck’s electronic systems overwrite their most recent data.

The insurer’s investigation happens at the same time as any government investigation. The carrier’s team is not a neutral party. They are protecting the carrier’s financial interest, and the documentation they gather will shape how your claim is handled, from the first phone call to the eventual lawsuit.

Under Texas Insurance Code (TIC) § 542.055, the insurer must acknowledge the claim and begin its investigation within 15 business days of receiving notice. This fast-approaching deadline tells you how urgently they are already moving right after the crash.

What Evidence Investigators Target First

In the first 48 hours after a truck crash, investigators focus on evidence that either disappears quickly or can be controlled by the carrier. Electronic logging device records, black box data, driver qualification files, and the physical condition of the truck are all gathered before independent parties can access them.

Electronic logging device (ELD) data is one of the first pieces of evidence that gets reviewed. Federal regulations require commercial truck drivers to log their hours of service in real time using ELDs. If the driver was close to or over their permitted driving-hour limit, that data is directly relevant to a claim that the at-fault driver was fatigued at the time of the crash.

Insurers move quickly to download ELD records before anyone else does. The black box (formally called the “event data recorder”) captures vehicle speed, braking force, throttle position, and steering input in the seconds before the crash. Some systems record on a continuous loop and overwrite data every 14 to 30 days.

Driver qualification files are also reviewed early. Under 49 CFR § 390.15, commercial carriers must maintain accident registers for at least three years. At the start of the investigation, the insurer’s team pulls the driver qualification file, which includes the driver’s license history, drug testing records, and prior violation history.

The insurance requirements for Texas commercial trucks can reach $750,000 or more in minimum coverage, which explains why insurers commit significant investigative resources as soon as possible.

The Risks of Giving a Recorded Statement

Shortly after a crash, the insurer’s adjuster may call to request a recorded statement. This call sounds routine, but the recording becomes part of the insurer’s claim file. Any statements made before medical records are complete or fault is established can be used to minimize the value of your claim.

The adjuster’s goal is to capture your version of events before you have reviewed any documentation, received full medical treatment, or spoken with an attorney. Inconsistencies between an early statement and later medical findings can be used to challenge who is at fault for the crash, as well as the severity of your injuries.

Adjusters are trained to ask follow-up questions that seem casual, like “Were you feeling okay before the crash?” and “Did anything distract you on the road?” These questions are meant to introduce other possible causes for the crash into the record.

As an injured third party, you are generally not required under Texas law to give a recorded statement to the at-fault driver’s insurer. Understanding how Texas insurance companies investigate accident claims can help clarify what the insurer does with this information.

What Texas Law Requires from Insurers

Texas insurers must follow specific deadlines when handling commercial truck accident claims. Under the Texas Prompt Payment of Claims Act, the insurer has 15 business days to acknowledge the claim and begin the investigation, and 15 additional business days after receiving all required information to accept or reject the claim.

If the insurer delays payment beyond the deadline without a good reason, Texas Insurance Code § 542.060 authorizes an 18% annual penalty on the unpaid claim amount, plus attorney fees. This rule gives claimants leverage when an insurer is delaying payment.

The carrier’s responsibility goes beyond the policy itself. Under 49 CFR § 390.15, commercial carriers must keep an accident register, with crash records preserved for at least three years. That register, along with driver qualification files and maintenance logs, can be accessed during the legal discovery process.

The step-by-step timeline of a Texas truck accident claim sets realistic expectations for when the insurer must respond and what happens if they don’t. Understanding Texas truck accident claims, including how commercial policies and carrier liability interact, is key to evaluating early settlement offers.

Take These Steps to Protect Your Claim

Protecting your claim starts at the scene of the accident and continues throughout the days that follow. Whatever you say, whatever documents you sign, and whatever you post online before hiring an attorney can become something the insurer uses against you.

Taking the following steps can help strengthen your claim before evidence disappears:

- Seek medical attention immediately, even if your injuries seem minor at first. Delayed medical attention allows adjusters to argue that your injuries were not caused by the crash or are not serious. Your medical records from the first 24 hours build the foundation of your claim.

- Do not sign any medical authorization forms or release any records to the insurer without knowing what you are agreeing to first. General authorizations can allow access to unrelated medical history that the insurer may use to argue that you had a pre-existing condition before the crash.

- Your attorney can send a formal preservation letter to the carrier within the first 48 hours after the crash. This is a legal notice that requires the carrier to preserve ELD data, black box recordings, driver logs, and maintenance records. Carriers that destroy records after receiving this notice can be punished in court.

- Avoid posting about the crash or your recovery on social media. Insurers routinely monitor your social media during the investigation period.

Work with an Attorney on Your Commercial Truck Accident Claim in Texas

Commercial truck accident investigations move quickly, and the insurer’s team always gets a head start while you are recovering from your injuries. Angel Reyes & Associates has handled truck and commercial vehicle claims across Texas for over 30 years. Our firm works on contingency, which means you pay no fee unless we win. Contact us for a free consultation.

Past results do not guarantee future outcomes.

Commercial Truck Accident Investigation FAQs

Are commercial truck drivers required to be drug tested after a serious crash?

Sometimes. Federal regulations under 49 CFR Part 382 require post-accident drug and alcohol testing in the following circumstances: when a crash results in a fatality; when a driver receives a ticket and the crash involves bodily injury that requires medical treatment; when a driver receives a ticket and a vehicle needs to be towed from the scene. In these cases, alcohol testing must occur within 8 hours of the crash, and drug testing must occur within 32 hours of the crash.

What happens if the trucking company repairs or scraps the truck before my attorney can inspect it?

If the carrier disposes of or repairs the truck after receiving a formal preservation letter, a court may issue an adverse inference instruction. This allows the jury to assume that the evidence would have harmed the carrier’s case. An attorney can also seek emergency injunctive relief, which legally requires the carrier to halt repairs or disposal of the truck before inspection occurs.

Can I check a trucking company's crash history without filing a lawsuit?

Yes. The FMCSA’s SAFER Web system provides publicly accessible carrier safety data, including reported crash counts, inspection results, and violation history. However, the full accident register with supporting documentation requires a formal legal discovery request.

How long does a commercial truck insurance investigation typically take before a settlement offer is made?

Texas law requires the insurer to accept or reject your claim within 15 business days of receiving all required information, but complex commercial cases regularly take weeks or months while expert opinions are gathered and liability is disputed. You will typically receive a low settlement offer early on, before the full extent of your injuries is documented. This offer does not reflect the claim’s actual value.

If I file a claim with my own insurer, will they start their own investigation?

Yes. If you pursue uninsured or underinsured motorist coverage, or if you file a collision claim under your own policy, then your insurer will conduct an independent investigation that is separate from the trucking carrier’s investigation. Any statements you make to your own insurer may surface during a lawsuit, so you should still be careful before agreeing to give your own insurer a recorded statement.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 55,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Graham Griffin

Editor

Graham Griffin is the Web & Content Manager at Angel Reyes & Associates, where he oversees content strategy, AI-powered workflows, a...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...