Who Pays After a Delivery Van or Fleet Vehicle Crash in Texas?

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

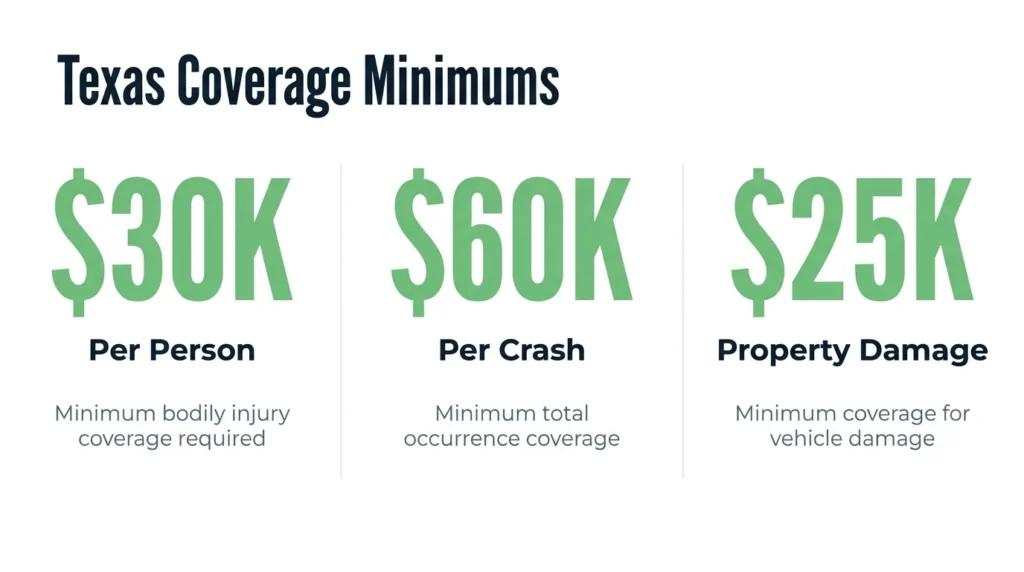

- Texas requires delivery vans and fleet vehicles to carry at least 30/60/25 liability coverage.

- Federal FMCSA rules raise minimums for interstate fleet vehicles over 10,001 pounds GVWR.

- USPS and government vehicle crashes follow FTCA or Texas Tort Claims Act rules, not standard insurance rules.

You were stopped at a light on Westheimer Road when a delivery van clipped your bumper and kept rolling into your driver-side door. The driver hands you a business card with a logo you don’t recognize and says his “company will handle it.” Days later, an insurance adjuster calls with questions that feel less like help and more like a trap, and the offer they send you won’t even cover your ER bill.

So, what coverage was the delivery van actually required to have, and how does it apply to you?

Texas Minimum Coverage for Fleet Vehicles

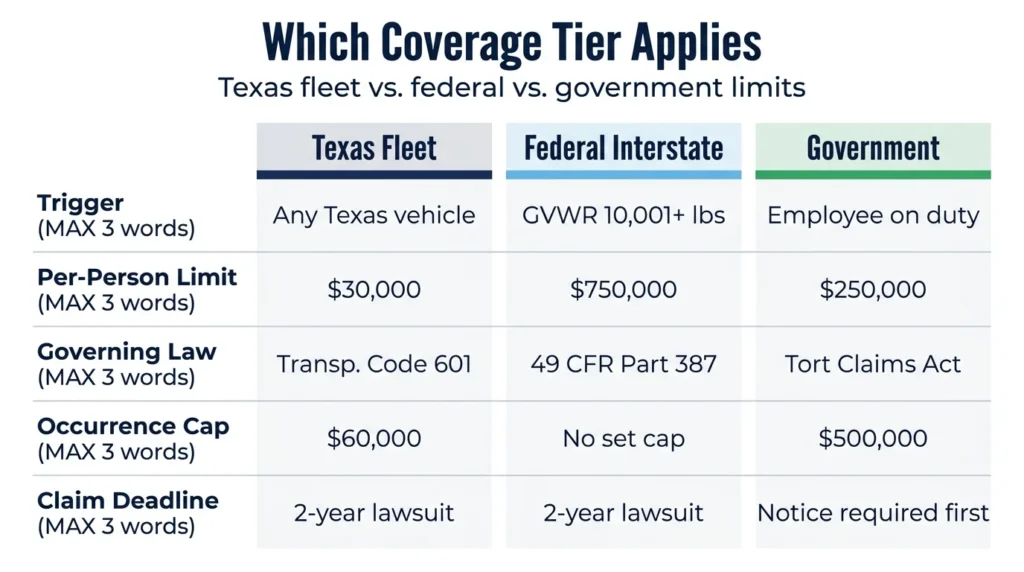

Delivery vans, fleet cars, and light service trucks operating in Texas must have an insurance policy that pays out at least $30,000 per injured person, $60,000 per occurrence, and $25,000 for property damage. This 30/60/25 baseline is the legal floor for financial responsibility. Most fleet operators have policy limits well above these minimums, which comes into play when injuries are serious.

These financial responsibility rules are described in Texas Transportation Code § 601.051, with the dollar minimums set in § 601.072. These apply to delivery vans and light service trucks that operate on intrastate Texas routes.

Personal auto policies typically do not cover vehicles used for business. That means a company cannot rely on a personal policy to cover its work vehicles, even if the driver owns the van. Fleet operators must have commercial auto coverage, and many of these claims are handled the same as truck accident cases.

Motor carriers that register delivery vans and service trucks with the Texas Department of Motor Vehicles must also file proof of insurance under Texas Transportation Code Chapter 643. The Texas Department of Insurance publishes a commercial automobile filing checklist that fleet operators use to confirm what their policies must include.

Federal Coverage Rules for Interstate Fleet Vehicles

Federal insurance rules apply when a commercial vehicle crosses state lines and has a gross vehicle weight rating (GVWR) of 10,001 pounds or more. At that point, the carrier falls under 49 C.F.R. Part 387, which sets minimum financial responsibility levels for interstate carriers. For non-hazardous cargo, the typical federal minimum is $750,000.

Most light delivery vans do not meet that weight threshold. They run local routes within Texas and are not subject to the federal requirements. For these vehicles, the minimum insurance requirements apply.

When a carrier crosses into federal territory, the Federal Motor Carrier Safety Administration (FMCSA) requires proof of insurance coverage on file. The agency’s insurance filing requirements page explains which carrier types must file and which forms are required. This filing creates a public record of the carrier’s insurance coverage.

The intrastate-versus-interstate distinction is important in an injury claim. A van running purely within Texas is governed by state law, but a van that crosses into Louisiana or New Mexico may be subject to federal rules and higher policy limits. Determining which tier applies often shapes the value of a commercial vehicle accident claim in Texas.

How Fleet Vehicle Coverage Works After a Crash

Texas is an at-fault state. This means the party that is responsible for the crash bears liability, and their insurer must pay up to the policy limits for bodily injury and property damage. When a fleet vehicle causes the crash, the claim is made against the company’s commercial policy first.

The commercial policy typically covers the vehicle and any employee who was operating it within the scope of employment at the time of the crash. The phrase “scope of employment” is a major point of dispute. For example, if the driver was running a personal errand, picking up lunch off-route, or clocked out at the time of the crash, then the insurer may argue that the policy does not apply.

Fleet policy limits often provide much higher coverage than the state’s minimum requirements of 30/60/25. For example, a national delivery company may have $1 million or more in available coverage per crash. The actual policy limits are more relevant than the legal minimum when calculating what you can recover.

Uninsured and underinsured motorist coverage in a commercial fleet policy works differently than personal auto UM/UIM. It may or may not protect a third-party injured driver, depending on how the policy is written. This is one of the technical layers that makes a commercial van crash different from a typical fender-bender.

Evidence preservation is critical after a crash with a delivery van or service truck. Photograph the vehicle’s commercial registration, employer logos, and DOT numbers. Note the driver’s work status, the time of the crash, and the route. If a company uses telematics or GPS, then the data is under their control, and it can be overwritten unless you send a preservation letter quickly.

Government Fleet Vehicles Follow Different Rules

Government-owned vehicles do not have the same private commercial insurance as a delivery company. If a USPS mail truck, TxDOT pickup, or city utility van hit you, the standard claims process does not apply. Two separate legal frameworks govern these claims, and not following the rules can end your case before it even begins.

Claims Against Federal Government Vehicles

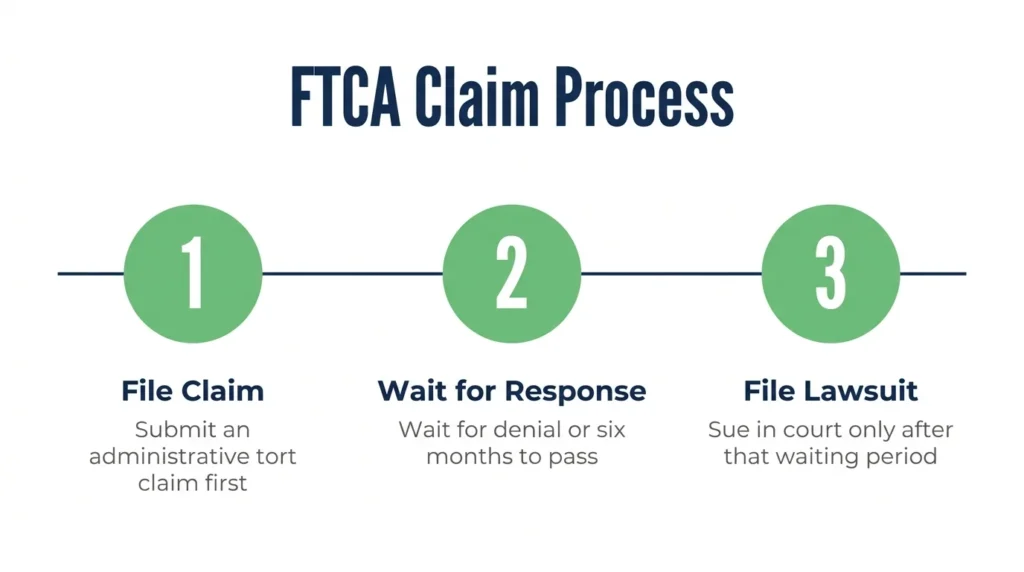

USPS mail trucks and other federal agency vehicles fall under the Federal Tort Claims Act. This means you cannot sue the federal government directly in court before filing an administrative tort claim with the responsible agency. After filing this claim, you must wait for either a denial or for six months to pass before filing a lawsuit.

The FTCA administrative claim deadline is two years from the date of injury. If you miss this deadline, you cannot recover any compensation, regardless of who caused the crash. Our guide to government truck accident claims explains this federal process in detail.

Claims Against State & Local Government Vehicles

The Texas Tort Claims Act allows you to sue the government in limited situations for crashes involving state and local government vehicles, but not all government vehicle crashes qualify under this act. It only applies when a public employee was operating a motor vehicle while doing their job.

Under Texas Civil Practice and Remedies Code § 101.023, the amount you can recover in a case against the government is strictly limited. A claim against a state or city agency is capped at $250,000 per person and $500,000 per occurrence for bodily injury or death. Claims against a local government drop to $100,000 per person and $300,000 per occurrence.

Texas law also requires written notice to the governmental unit before a lawsuit can be filed. Failing to give timely notice can dismiss an otherwise valid claim. The process for suing a government entity involves shorter deadlines and stricter procedures than a typical insurance claim.

Talk to an Attorney About Commercial Vehicle Accidents in Texas

Commercial fleet and government vehicle claims involve aspects that ordinary crashes do not. This includes multiple coverage layers, disputes over whether the crash happened within the driver’s scope of employment, and strict legal deadlines.

Angel Reyes & Associates has over 30 years of experience handling commercial vehicle accident claims in Texas, including delivery van crashes, service truck collisions, and government vehicle cases. We have recovered more than $1 billion for clients.

We work on contingency, so there is no fee unless we win, and consultations are always free. Our client testimonials show how we approach these cases. Contact us today to find out what your claim may be worth.

Past results do not guarantee future outcomes.

Delivery Van & Fleet Vehicle Crash FAQs

Can a fleet driver's employer be held liable if the driver was an independent contractor, not an employee?

It depends on how much control the company exercised over the driver’s work. Texas courts look at factors like who set the schedule, who owned the vehicle, and who directed the route when deciding whether an “independent contractor” is actually an employee when it comes to liability.

Does Texas require fleet vehicles to carry cargo insurance in addition to liability coverage?

Not usually. Liability coverage and cargo coverage are separate. Texas law does not require cargo insurance for most intrastate light fleet vehicles, but carriers hauling certain goods or operating under a motor carrier permit may face cargo coverage requirements under their specific registration class.

What happens if the at-fault fleet vehicle had a lapsed or canceled insurance policy at the time of the crash?

A lapsed commercial policy means the injured party may need to pursue recovery through their own uninsured motorist coverage or directly from the company. Texas law requires drivers and companies to maintain proof of financial responsibility, but policy lapses may still occur. In this case, the injured party bears the burden of pursuing other available ways to recover compensation.

Does the driver's personal auto insurance ever apply in a fleet vehicle crash?

Rarely. Most personal auto policies exclude vehicles used for business or owned by an employer. If the driver was operating a company-owned delivery van at the time of the crash, their personal policy will likely not apply.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 55,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...