What Happens When Multiple Commercial Policies Apply?

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- "Other insurance" clauses in commercial liability policies determine whether a policy pays first, last, or proportionally. The motor carrier's policy is made primary by federal law, regardless of clause language.

- Each insurer's prompt-payment obligations under Texas Insurance Code § 542 run independently.

- Crash victims are not required to resolve coverage disputes between carriers. To hold insurers accountable, send written notice of your claim to all potentially applicable carriers.

If you’ve been in a crash with a commercial truck, you are suffering both physical and emotional trauma. But layered over that is the stressful financial consequences of this nightmare. You have medical bills as well as possible missed paychecks because of time off from work. Complicating matters is that collisions involving commercial carriers rarely involve just one insurer, and no company wants to foot the bill for damages from this accident.

The motor carrier carries its own liability policy. The owner-operator may carry separate coverage. The freight broker may have a contingent liability policy. When multiple commercial policies apply to the same crash, each insurer’s first priority is to determine whether its policy is the one that has to pay. And this can result in an ugly coverage dispute.

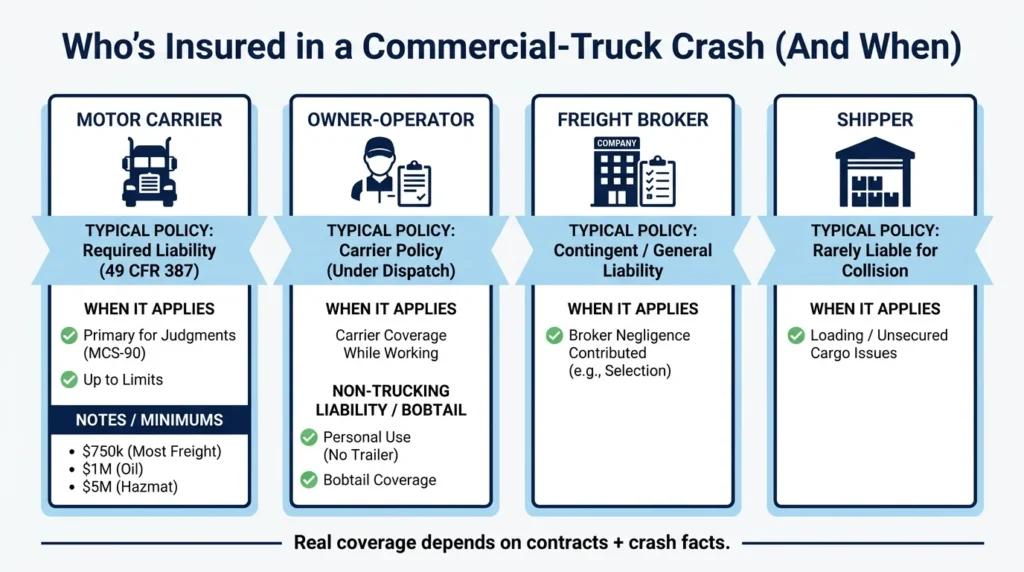

Which Parties Carry Insurance After a Commercial-Truck Crash

In most commercial-truck crashes, at least two and sometimes four or more insurance companies are involved. That’s why you, as a victim with a claim, need to understand who carries what coverage, which will determine the policy that should respond first.

The motor carrier (the trucking company that owns or operates the tractor-trailer) is required by federal law to maintain a minimum liability policy. Under 49 CFR, Part 387, the minimum depends on the cargo type:

- $750,000 for most freight

- $1 million for oil

- Up to $5 million for hazardous materials

This policy must include an MCS-90 endorsement, which is the mechanism that makes the carrier’s coverage primary.

Owner-operators who work under a motor carrier’s operating authority are typically covered by the carrier’s policy while under dispatch. When driving the vehicle outside of dispatch (say, for personal errands or between loads), many owner-operators carry their own non-trucking liability coverage (applies when driving for a nonwork-related trip) or bobtail insurance policy (applies when driving without a trailer). Whether that policy or the carrier’s policy applies depends on what the driver was doing at the time of the crash.

Freight brokers occupy a different position. Federal law does not require brokers to carry motor truck cargo liability, but some have contingent liability or general liability policies. Those policies typically activate only when the broker’s own conduct (for example, selecting a carrier with a known safety violation history) contributed to the wreck.

Shippers are rarely liable for the collision itself, but their coverage may be triggered if improperly loaded or unsecured cargo caused or contributed to the accident.

If you’re confused by the complexities of commercial truck insurance and want to know which policies to pursue after your accident, see commercial truck insurance requirements.

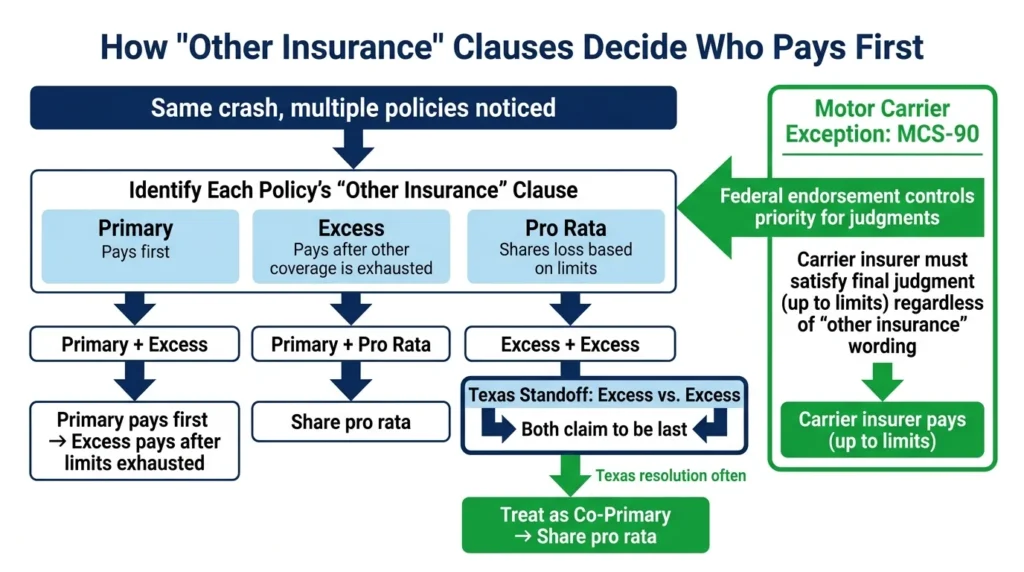

How “Other Insurance” Clauses Determine Who Pays First

There is a provision in liability insurance policies called the other insurance clause, which determines the priority order among insurers for covering the same loss. Nearly every commercial liability policy contains one, and its terms determine whether that policy is the first to respond, the last to respond, or one of several sharing financial responsibility equally for the loss.

There are three types of “other insurance” clauses.

- Primary clause: The policy pays first regardless of what other coverage exists.

- Excess clause: The policy pays only after all other applicable coverage has been fully exhausted.

- Pro rata clause: When two policies are both primary, the insurers divide the loss in proportion to their respective policy limits.

If you’ve been in a crash with a commercial truck, you’re likely to experience delays with your claim if there are two insurance policies involved that both contain excess clauses. Why? Each insurer will read its policy and conclude that the other carrier’s policy is the first payer. Texas courts typically resolve this standoff by treating both policies as co-primary and applying pro rata sharing so that each carrier pays a proportional share based on its policy limits.

For motor carriers, federal law determines the outcome of the other-insurance-clause dispute. The MCS-90 endorsement required by 49 CFR, Part 387, obligates the carrier’s insurer to pay any final judgment against the motor carrier up to policy limits, regardless of what the policy’s “other insurance” clause says.

Why Coverage Disputes Delay Payment to Victims

If multiple insurers receive notice of your claim, each adjuster focuses not on investigating your injuries but on determining whether their company can shift primary exposure to another carrier. That lengthy process entails insurers sending reservation-of-rights letters, cross-carrier correspondence, and coverage position letters.

You, as the injured party, are not part of this fight among insurers. Thus, you aren’t obligated to wait for the carriers to resolve coverage priority before pursuing compensation. And yet, if you are handling your claim alone, you likely will, because none of the adjusters has an incentive to explain to you that you can pursue damages from all carriers simultaneously.

Each insurer is angling for the best position. The motor carrier’s insurer wants to prove that the driver was an independent contractor, not an employee. The owner-operator’s insurer wants to prove that the driver was under dispatch and therefore covered by the carrier’s policy. The freight broker’s insurer wants to prove that the broker did nothing negligent.

You should understand the timeline of a Texas truck accident claim and the tactics insurers use before you directly engage with any adjuster. Knowing how trucking companies and insurers delay and deny claims in Texas will change how you approach early communications with each relevant party.

What Texas Law Requires During a Multi-Insurer Claim

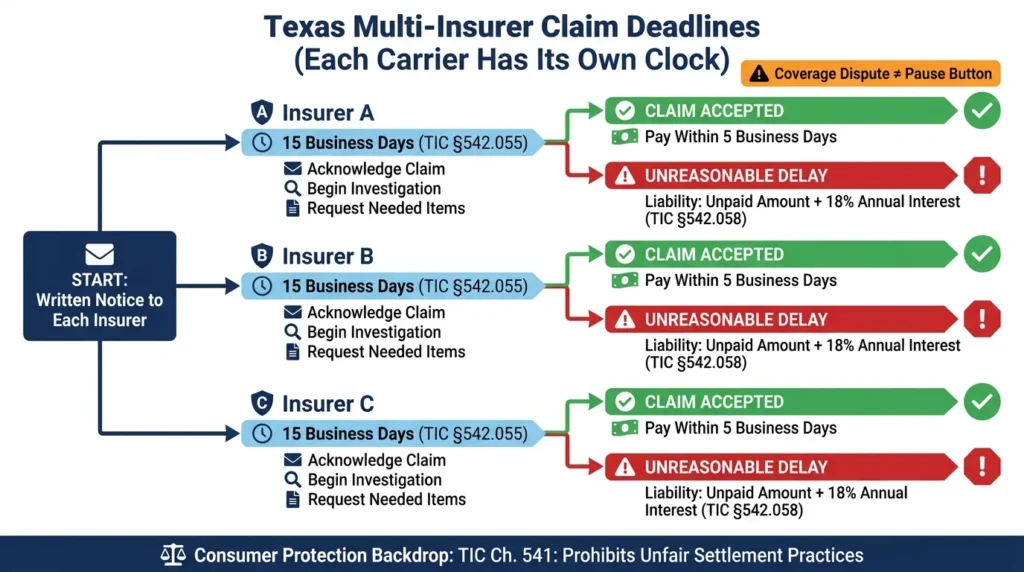

One thing you can be assured of is that an inter-carrier coverage dispute does not let any insurer off the hook under Texas law. Each carrier has its own statutory deadlines.

Under Texas Insurance Code § 542.055, each insurer must acknowledge receipt of the claim, begin its investigation, and request all items needed to evaluate the claim within 15 business days. This deadline applies to every carrier separately. If three insurers receive written notice on the same day, all three are running on their own 15-business-day investigation clock.

An insurer that accepts your claim must pay you within five business days. If the payment is unreasonably delayed, the carrier becomes liable for the unpaid amount plus 18 percent annual interest, as laid out in Texas Insurance Code § 542.058.

You are also protected under Texas Insurance Code Chapter 541, which prohibits unfair claim settlement practices, including misrepresenting policy provisions and using a multi-carrier coverage dispute as a pretext to delay payment without just cause.

How to Protect Your Claim When Multiple Policies Apply

If you find out that multiple insurance carriers are involved with your claim, you should take these steps to protect your legal position.

Send written notice of your claim to every carrier whose coverage may apply. Do not rely on one insurer to notify the others. Written notice to a carrier starts its independent 15-business-day investigation deadline under TIC § 542.055. If a carrier never received written notice, it is not obligated to investigate your claim by a certain date.

Do not give a recorded statement to any insurer without an attorney present. Every adjuster has a different coverage interest, and your recorded statement could be used to benefit one carrier’s position at the expense of another’s—or at the expense of your claim. Each insurer will request a statement early in the process, but you don’t have to provide one before consulting a lawyer.

Preserve all reservation-of-rights letters you receive. Each letter identifies the specific coverage provisions the insurer is disputing. Those disputes define the battlefield of the inter-carrier dispute. Your attorney can use these letters to hold each insurer to its investigation deadlines and coverage obligations.

Document and preserve physical evidence from the crash as early as possible, including electronic logging device data, black box information, maintenance records, and cargo loading documents.

Understanding why insurers in Texas delay payment and the specific tactics they use in commercial vehicle cases can help you recognize when a delay is strategic.

Talk to an Attorney About Your Case

When multiple insurers are working to minimize their exposure, a victim handling the claim alone is at a big disadvantage. Angel Reyes & Associates has handled Texas commercial vehicle accident claims for over 30 years. Our case results demonstrate how we have successfully fought insurers on behalf of our clients. We work on contingency, so we receive no fee unless we win your case. Contact us for a free consultation.

Past results do not guarantee future outcomes.

Crashes Involving Multiple Commercial Policies FAQs

Can I collect from more than one commercial policy after a truck crash?

In most cases, you cannot recover the same damages from multiple policies, since insurance is designed to make you whole, not to produce double recovery. You can, however, pursue multiple carriers simultaneously. If the primary policy limits are exhausted before your damages are fully covered, an excess or umbrella policy may then pay out the remaining amount.

Does a freight broker's insurance cover victims of a truck crash the broker arranged?

A freight broker’s contingent liability policy typically covers the broker’s own negligent conduct (for example, selecting a carrier it knew had a pattern of safety violations). It does not replace the motor carrier’s primary liability coverage. Whether the broker’s policy responds at all depends on what role the broker’s actions played in causing or contributing to the crash.

What should I do if I receive reservation-of-rights letters from multiple insurers?

A reservation-of-rights letter means the insurer is investigating while preserving the right to deny coverage later. Receiving these letters from multiple carriers simultaneously means each carrier is attempting to minimize its own financial exposure. You should not respond to these letters without legal representation. Each letter identifies the specific provisions in dispute, and your attorney can use that information to track investigation deadlines and hold each insurer accountable to its legal obligations.

About the Authors

Alex Ivanov

Writer

Alex Ivanov is a personal injury attorney at Angel Reyes & Associates, focused on car, truck, and motorcycle accident cases. Licensed in Texas and multiple federal districts, Alex brings international legal experience and a global education to his practice. He earned his LL.M. from Texas A&M University School of Law after graduating from Belarussian State University in 2016. Alex is fluent in Russian, English, Ukrainian, and Belarussian, and is recognized by multiple national trial lawyer associations for his results and leadership under 40.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...