Umbrella & Excess Coverage in Texas Trucking Accidents: What Victims Need to Know

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- Excess policies follow the primary policy form and activate when the primary limit is exhausted; umbrella policies are broader but have their own self-insured retention.

- Carriers are not required to disclose umbrella or excess coverage voluntarily; finding it requires formal legal tools.

- The FMCSA SAFER database and MCS-90 filing show only the primary policy -- they do not identify additional coverage.

When a serious truck accident on I-35W near Fort Worth produces damages that approach or exceed the carrier’s primary policy limit, many victims assume the inquiry ends there. It does not. Many trucking companies carry umbrella or excess liability policies that sit above the primary coverage and activate when the primary limit is exhausted. Those layers often go unidentified because carriers have no obligation to disclose them voluntarily.

When the Primary Policy Is Not Enough

Federal law sets the floor, not the ceiling. Under 49 CFR Part 387, commercial motor carriers operating in interstate commerce must carry a minimum of $750,000 in primary liability coverage for general freight, rising to $1,000,000 or $5,000,000 for carriers hauling hazardous materials.

In practice, many large carriers carry substantially more because major shippers require higher limits as a condition of their hauling contracts. A national carrier that pulls loads for a large retailer may be contractually required to maintain $5 million, $10 million, or more in total coverage capacity. The FMCSA minimum tells you the floor; it tells you nothing about the actual ceiling.

When a catastrophic crash produces traumatic brain injuries, spinal damage, or a fatality, the damages can reach or exceed even the higher federal minimums quickly. In those cases, the coverage investigation cannot stop at the primary policy. For a broader look at commercial truck insurance structures, see Texas commercial truck insurance requirements.

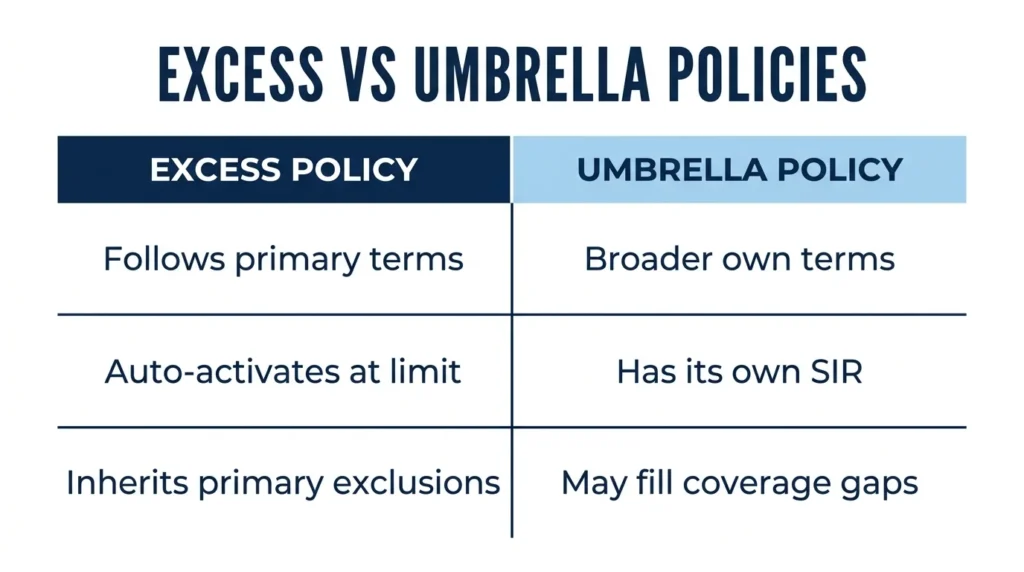

Excess vs. Umbrella: What the Difference Means to Your Claim

Two distinct policy types sit above the primary layer.

Excess liability insurance follows the form of the primary policy. It has the same coverage terms, the same exclusions, and the same conditions as the primary. It activates automatically once the primary limit is exhausted. There is no gap between primary exhaustion and excess activation — one picks up where the other leaves off.

Umbrella liability insurance is structurally different. It is broader in scope and may cover scenarios that the primary policy excludes. It can also “drop down” to fill coverage gaps when the primary policy does not apply to a particular claim. The tradeoff is that umbrella policies carry their own self-insured retention (SIR), a threshold the carrier must pay out of pocket before the umbrella insurer gets involved.

That SIR matters to victims. When a carrier’s umbrella contains a $500,000 SIR, the carrier is effectively self-insuring that layer. No independent insurer is managing or negotiating that portion of the claim — the carrier’s own team is. Knowing whether a SIR applies identifies who is actually at the negotiating table.

For more on how trucking insurers manage and contest claims, see how trucking companies and insurers delay and deny claims in Texas.

Why You May Not Know the Coverage Exists

The FMCSA SAFER database shows the carrier’s primary insurance filing. It does not show umbrella or excess policies. The MCS-90 endorsement references the primary policy only. Texas DMV filings for intrastate carriers cover primary coverage minimums. None of these public sources identify additional layers.

Carriers are not required to disclose their full coverage picture voluntarily. In many cases, neither the carrier nor the primary insurer will mention that additional coverage exists unless directly asked, and the question must be asked formally.

The tools that surface these additional layers are legal tools. A preservation letter sent immediately after the crash creates an obligation to retain all insurance-related documents. A direct insurance coverage demand letter sent to the carrier requests disclosure of all applicable policies. Formal discovery in litigation compels production of all policies, declarations pages, and coverage limits. The failure to disclose policies that exist can carry legal consequences.

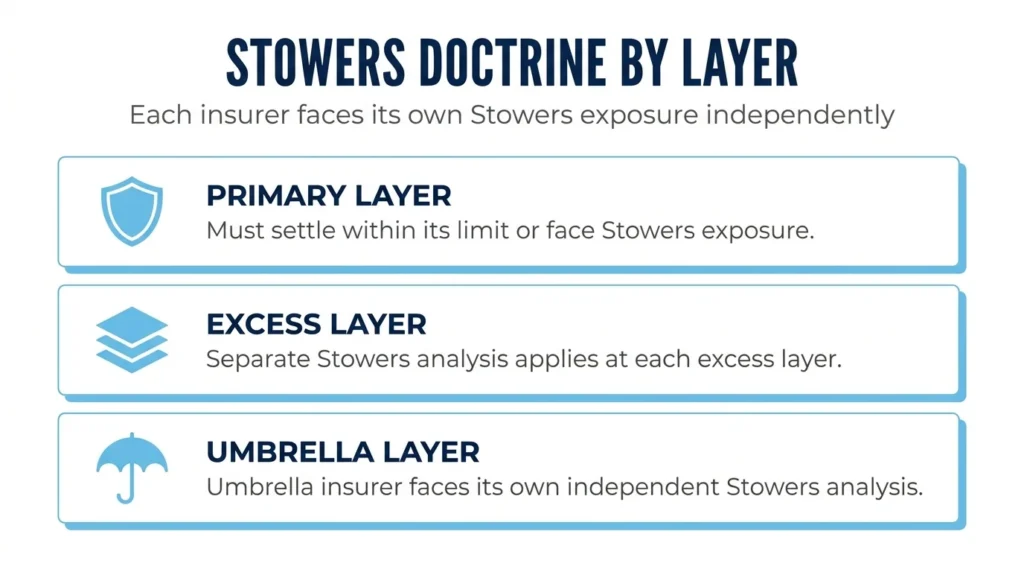

The Stowers Doctrine and Each Policy Layer

Texas’s Stowers doctrine gives injured parties a significant strategic tool. Under Stowers, a liability insurer that unreasonably refuses to settle a reasonable demand within its policy limits becomes exposed to the full amount of any verdict that exceeds those limits. That exposure falls on the insurer, not just the carrier.

The doctrine applies independently to each coverage layer. The primary insurer faces its own Stowers obligation within its limit. The excess insurer faces a separate Stowers obligation within its layer. The umbrella insurer faces its own analysis at its level.

This creates structured leverage when presenting settlement demands. A demand calibrated at or within the primary limit puts the primary insurer on notice of its Stowers exposure. If the primary settles and damages remain outstanding, a subsequent demand within the excess layer puts that insurer under the same pressure. Each insurer must decide whether refusing to settle is worth the risk of exposure beyond its limit.

Talk to an Attorney About Your Case

Identifying umbrella and excess coverage above the primary policy limit is not something that happens automatically. It requires knowing what to ask for, when to ask for it, and how to use the legal tools available. In cases involving catastrophic injuries, this investigation can be the difference between a partial recovery and a full one.

Angel Reyes & Associates has handled truck accident cases across Texas for over 30 years. The firm has recovered more than $1 billion for clients and offers free consultations with no fee unless your case is resolved in your favor. If your damages may exceed the carrier’s primary policy limit, contact the firm to discuss what additional coverage may be available.

You can also review how the overall claims process works at our firm’s guide to how truck accident claims work in Texas.

Past results do not guarantee future outcomes.

Frequently Asked Questions

How do I find out if a trucking company has umbrella or excess coverage?

There is no public database that lists umbrella or excess policies for trucking companies. The FMCSA SAFER database shows primary liability filings, not additional layers. The most effective approaches are sending a direct insurance coverage demand letter to the carrier requesting disclosure of all applicable policies, obtaining the information through formal discovery in litigation, or investigating the carrier’s shipper contracts, which often specify required coverage minimums and can reveal the carrier’s typical coverage structure.

Can an excess or umbrella insurer deny my claim even if the primary insurer settles?

Yes. Each policy layer operates under its own terms. If the primary insurer settles your claim at its full limit, the excess or umbrella layer only activates if your total damages exceed the primary limit. If a coverage dispute arises at the excess layer, the excess insurer may raise its own defense. Excess policies follow the primary form, which means they generally inherit the primary’s exclusions.

What is a self-insured retention in a trucking umbrella policy, and how does it affect me?

A self-insured retention (SIR) is the amount the carrier must pay out of its own funds before the umbrella policy activates. If the SIR is $500,000, the carrier is responsible for the first $500,000 of any claim that falls into the umbrella layer. During that SIR period, the carrier (not an independent insurer) is controlling the investigation and negotiation. This can affect how quickly the claim is handled and who is making decisions about settlement.

Is umbrella or excess coverage required for Texas trucking companies?

No. Federal law under 49 CFR Part 387 requires only minimum primary liability coverage. Umbrella and excess policies are voluntary. However, large shippers routinely require carriers to maintain total coverage well above federal minimums as a condition of their hauling contracts, which in practice means many large carriers do carry significant additional layers even though no law requires it.

What happens if a trucking company has no umbrella or excess coverage and the primary limit is not enough to cover my damages?

If the primary policy is exhausted and there are no additional coverage layers, you may still have options. You can pursue a direct judgment against the trucking company for any amount above the insurance recovery, which depends on the carrier’s assets. Other liable parties may carry their own policies. Your own uninsured or underinsured motorist coverage may apply if the carrier’s total coverage is insufficient. An attorney can identify all available recovery paths.

About the Authors

Alex Ivanov

Writer

Alex Ivanov is a personal injury attorney at Angel Reyes & Associates, focused on car, truck, and motorcycle accident cases. Licensed in Texas and multiple federal districts, Alex brings international legal experience and a global education to his practice. He earned his LL.M. from Texas A&M University School of Law after graduating from Belarussian State University in 2016. Alex is fluent in Russian, English, Ukrainian, and Belarussian, and is recognized by multiple national trial lawyer associations for his results and leadership under 40.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...