Is Texas a No-Fault State for Motorcycle Accidents?

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- Texas is an at-fault state; you pursue the other driver's liability insurance, not your own, after a crash.

- A motorcyclist found more than 50% at fault in Texas recovers nothing under the comparative fault rule.

- UM/UIM coverage is critical in Texas because minimum liability limits rarely cover serious motorcycle injuries.

You were hit on I-35 near Round Rock and are trying to figure out whose insurance pays for what. You’ve heard the term “no-fault” and aren’t sure if it applies. It does not. Texas is an at-fault state, and that distinction changes everything about how your motorcycle accident claim works.

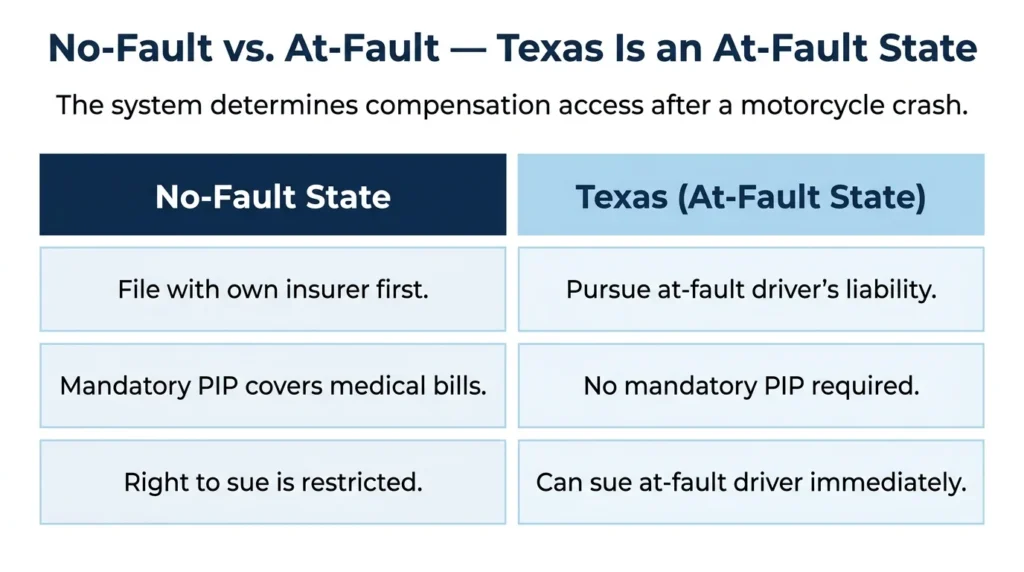

Texas Is an “At-Fault” State, Not a “No-Fault” State

No-fault insurance does not apply in Texas. Texas operates under an at-fault liability system: the driver who caused the crash is responsible for the resulting damages. If another driver hit you, you file a claim with their liability insurance — not your own — for your medical costs, lost income, and other losses.

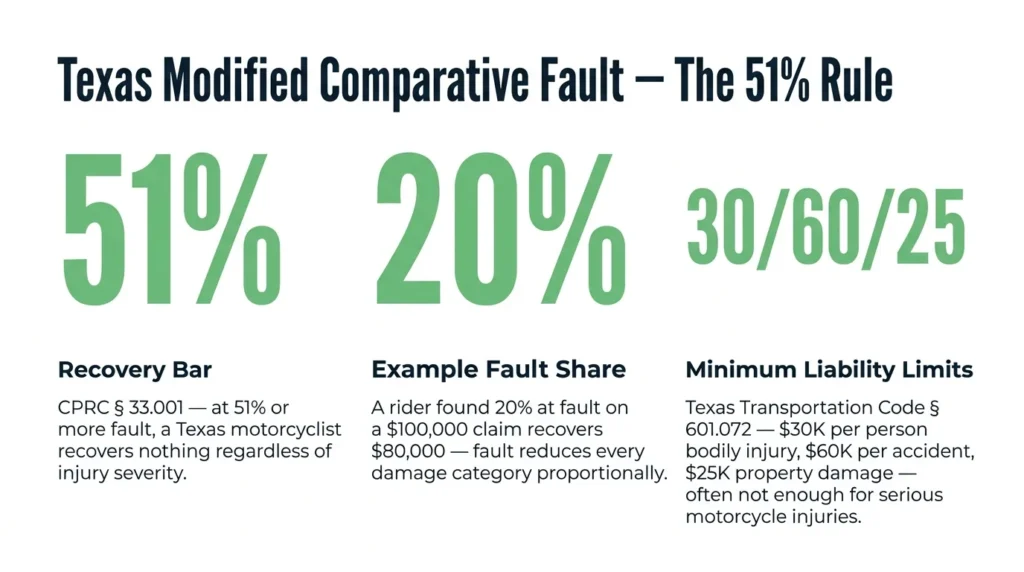

Under the Texas Motor Vehicle Safety Responsibility Act, all Texas drivers must carry minimum liability insurance: $30,000 per person for bodily injury, $60,000 per accident for bodily injury, and $25,000 for property damage. For a motorcyclist with serious injuries, those minimum limits are frequently not enough to cover the full loss.

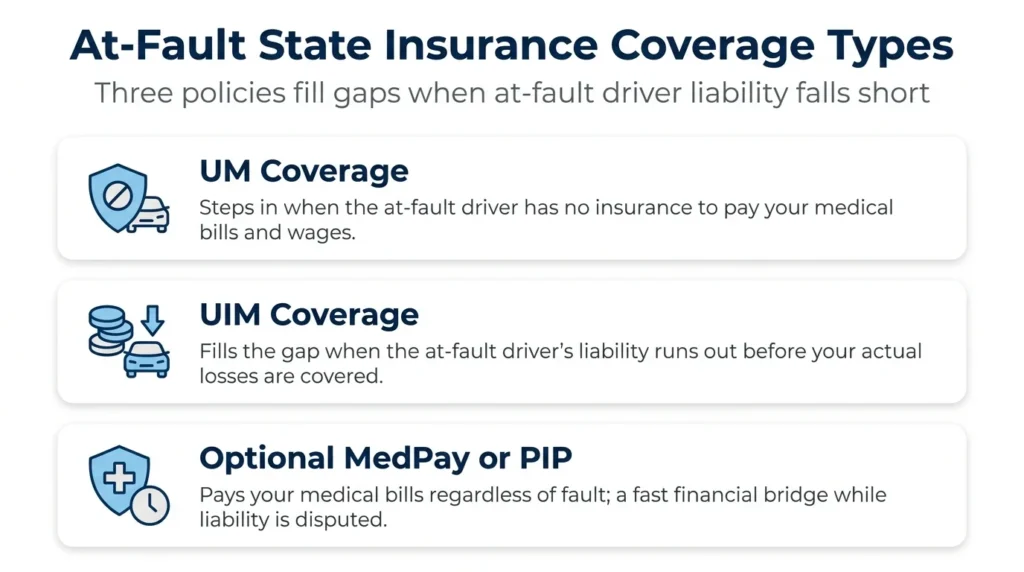

Your own insurance comes into play only if the at-fault driver has no insurance, or has insufficient coverage to pay your full damages. That is where uninsured and underinsured motorist coverage can fill the gap.

How Texas Differs from No-Fault States

In states with no-fault insurance systems, each driver carries personal injury protection (PIP) and files with their own insurer first after a crash, regardless of who caused it. The ability to sue the other driver is restricted in those states until injuries reach a defined severity threshold.

Texas does not require PIP coverage. As a rider in Texas, you can purchase optional PIP or medical payments coverage, but it’s not part of a standard motorcycle policy unless you specifically add it. Most Texas riders don’t have it unless they asked for it.

In a no-fault state, a rider who is partly at fault can still collect from their own PIP without first proving what the other driver did wrong. In Texas, establishing the other driver’s fault is the foundation of your entire claim. Without it, there is no recovery from their insurer.

Texas’s Modified Comparative Fault Rule

Texas uses a modified comparative fault system governed by Texas Civil Practice and Remedies Code Chapter 33. Your compensation is reduced by your percentage of fault. If you are found 20% at fault for a crash, you recover 80% of your damages.

The critical threshold is 51%. If you’re found more than 50% at fault in Texas, you recover nothing.

That threshold matters because insurance adjusters routinely assign motorcyclists a higher share of fault than the evidence supports. It’s a common negotiating posture, and it directly threatens your ability to recover. How you document, present, and challenge fault at the negotiation or litigation stage directly affects whether you collect anything at all.

Understanding how Texas motorcycle accident settlements work before you accept an offer can help you recognize whether the fault percentage being assigned to you reflects what actually happened.

When the At-Fault Driver Is Uninsured or Underinsured

Texas roads include a significant number of uninsured drivers. When the driver who hit you has no coverage, your own uninsured motorist (UM) coverage becomes the primary source of compensation if you purchased it.

Texas insurers are required to offer UM and UIM coverage, but you can choose to reject it in writing. Many riders do not realize they turned it down until they need it. UM coverage steps in when the at-fault driver has no insurance. Underinsured motorist (UIM) coverage fills the gap when the at-fault driver’s limits are too low to cover the full loss.

Given that motorcycle injuries are often severe and the at-fault driver’s minimum policy ($30,000 per person) may not come close to covering medical costs, carrying UM/UIM coverage is one of the most practical protections available to you.

Work with an Attorney on Your Claim

The at-fault system puts the burden on you to prove what the other driver did wrong and to fight a fault percentage that insurers frequently inflate. That is not a process that goes better without representation after a motorcycle accident.

Angel Reyes & Associates has spent more than 30 years representing motorcycle accident victims across Texas. We have recovered more than $1 billion for our clients, and have helped those who have been injured recover the compensation they are entitled to while holding insurers accountable.

We offer free initial consultations and take cases on a no-fee-unless-you-win basis. Contact us to talk through your claim.

Past results do not guarantee future outcomes.

Motorcycle Accident Fault FAQs

What happens if the at-fault driver only has minimum insurance?

Texas minimum liability limits are $30,000 per person for bodily injury. Serious motorcycle injuries frequently exceed that amount. If the at-fault driver’s coverage cannot pay your full damages, your own underinsured motorist (UIM) coverage can fill the gap — up to your UIM policy limit. If you rejected UIM coverage when you purchased your policy, you may have limited options beyond suing the driver directly.

Can I collect from my own insurance after a motorcycle crash in Texas?

In most cases, you can’t collect from your standard liability policy. Your own coverage becomes relevant when the at-fault driver has no insurance (UM coverage) or insufficient coverage (UIM coverage). Optional PIP or medical payments coverage will also pay for injuries regardless of fault if you added it to your policy. Standard Texas motorcycle policies do not include PIP automatically.

How long do I have to file a Texas motorcycle accident lawsuit?

The standard personal injury statute of limitations in Texas is two years from the date of the crash. Claims against a government entity, such as a claim over a defect on a road maintained by a city or county, carry shorter deadlines and require formal notice before the lawsuit can be filed. Missing the deadline almost always ends your right to sue.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 55,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...