Does UM/UIM Coverage Apply to Company Vehicle Accidents in Texas?

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- Texas insurers must offer UM/UIM on commercial fleet policies, but employers can reject it in writing.

- Your personal auto policy may cover a company vehicle crash, unless a regular-use exclusion applies.

- Workers' comp does not block UM/UIM claims since the claim is filed against the insurer, not the employer.

You were driving the company truck back to the yard along I-35E when a driver in the next lane drifted into you and kept going. The police found him later, but he had no license, no insurance, and no way to pay for the damage he caused. Now, your back hurts, your medical bills are piling up, and someone at the insurance office is telling you that the company’s policy doesn’t cover it.

How UM/UIM Law Applies to Company Vehicles in Texas

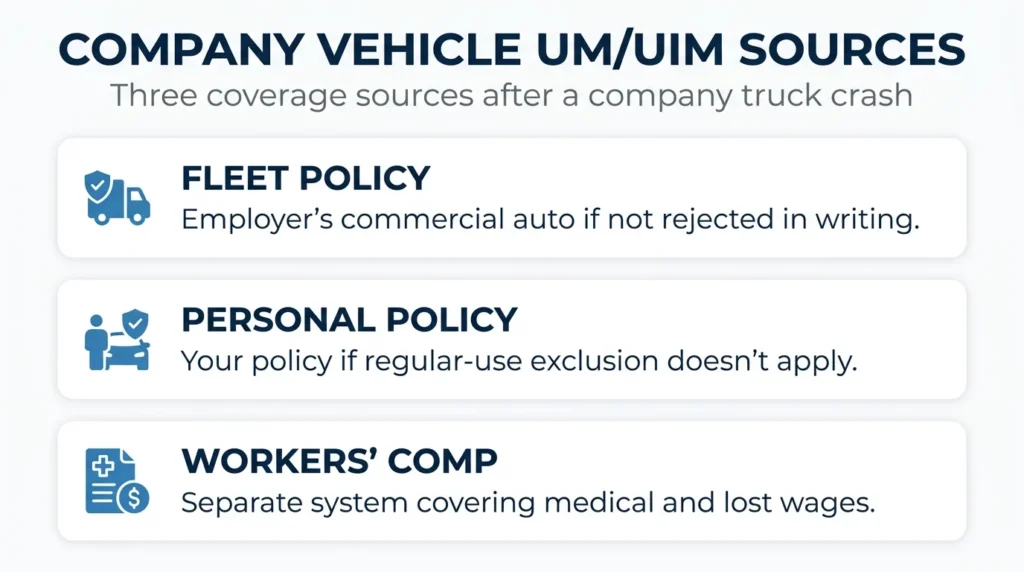

Texas requires every auto liability insurer to offer uninsured and underinsured motorist (UM/UIM) coverage on every policy issued in the state, including commercial fleet policies. That means an employer’s commercial auto insurer must offer UM/UIM when the policy is created.

If the employer accepts the coverage, employees who are riding in or driving a covered company vehicle can generally make a claim under this coverage. The legal foundation comes from Texas Insurance Code § 1952.101, which controls how UM/UIM is offered and rejected in Texas.

Commercial fleet policies follow the same rule as personal auto policies on this issue, but the structure of a commercial policy is different from a personal policy. The named insured is the company, not you. Who is covered is usually determined by the policy’s own language, and only the company has the right to reject coverage.

The difference between “your” coverage and “the company’s” coverage is where most disputes start. Knowing which policy applies is the first step to figuring out who will pay your bills.

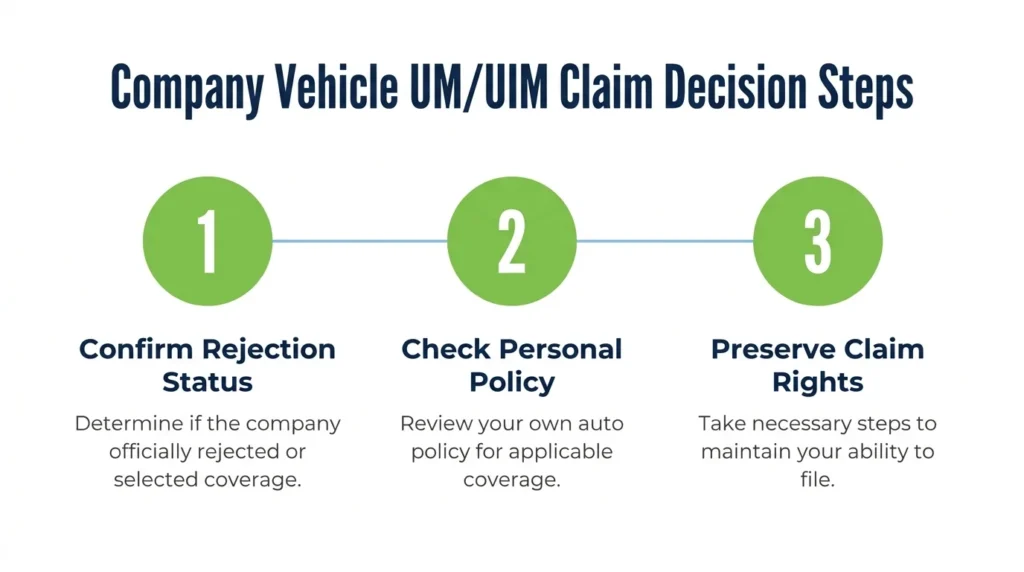

What Happens When Employers Reject UM/UIM on a Commercial Policy?

Employers can reject UM/UIM coverage on a commercial auto policy in writing. Once a valid written rejection is on file with the insurer, the policy carries no UM/UIM coverage at all, and an employee injured by an uninsured driver has no claim under that policy for those damages. Fleet administrators reject this coverage more often than individual drivers do (usually to cut premium costs).

The rejection has to be in writing by a named insured on the policy. On a commercial fleet policy, the named insured is typically the employer. A verbal agreement, an email exchange, or an implied waiver does not meet the legal requirement under § 1952.101. Insurers who claim a rejection exists must be able to produce the signed document proving it.

Most workers never find out that the coverage was rejected until after a crash. You file a claim, expect the commercial policy to cover it, and instead get a denial letter saying the coverage was waived years ago by someone in the company office.

If you suspect a rejection is the reason your claim is being denied, our guide to uninsured motorist accident claims will walk you through what Texas law actually requires insurers to provide and how to push back if coverage is denied.

Using Your Personal Policy After a Company Vehicle Crash

Your personal auto policy may help if the employer’s policy has rejected UM/UIM, but it depends on the policy language. Most personal auto policies cover injuries in non-owned vehicles (including a company vehicle), unless a business-use or regular-use exclusion applies. The exclusion language typically decides whether the claim will be covered or denied.

When Your Personal Policy May Apply

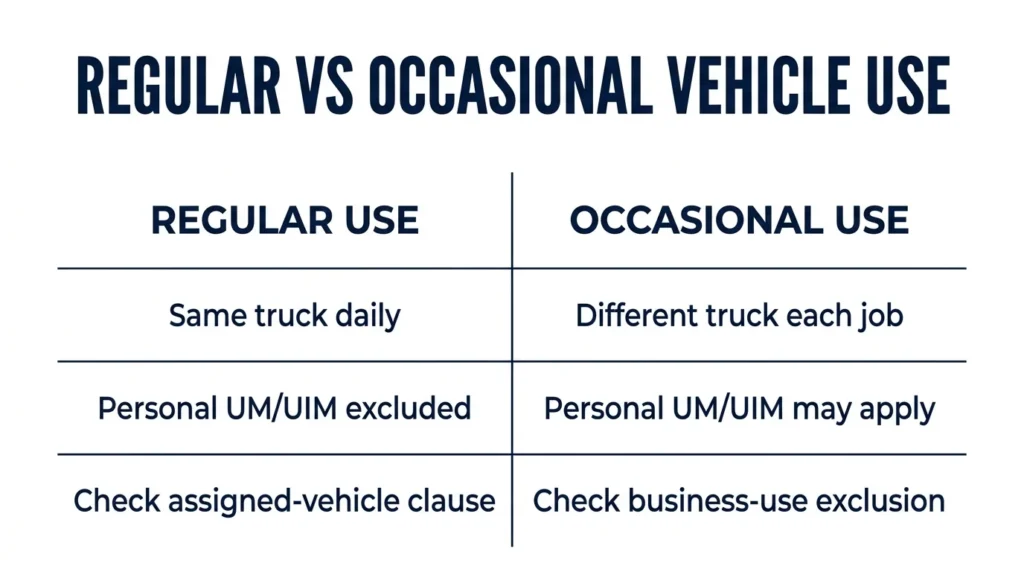

Many personal auto policies contain a “regular use” (or “furnished for regular use”) exclusion. The exclusion eliminates UM/UIM coverage for vehicles that are provided to you for everyday use (like an assigned company truck).

This exclusion does not always apply to vehicles that you only drive occasionally. Workers who drive the same company vehicle every day usually fall under this exclusion. Workers who drive a different truck from a shared lot on different days often do not fall under this exclusion. How you use the vehicle is more important than what the company calls the arrangement.

If your personal policy’s UM/UIM coverage does apply, you can file a claim against your own insurer for any damages that the at-fault driver cannot pay. For most workers in this position, a personal claim ends up being the difference between recovering something and recovering nothing. Our overview of car accident claims explains how personal policy coverage interacts with at-fault driver liability.

Regular Use vs. Occasional Use

Texas courts have drawn the line between “regular use” and “occasional use” based on the facts of each case. How frequently the driver uses the vehicle and whether it’s assigned only to them are the most important factors. A worker who is assigned a specific company truck that they drive every day will be treated as a “regular user.” A worker who drives different vehicles for specific jobs will be treated as an “occasional user.”

If you fall outside the regular-use exclusion, your personal UM/UIM coverage can stack on top of any other available coverage, which can dramatically increase your total recovery.

Read your personal policy’s non-owned vehicle and business-use provisions before assuming coverage does not exist. The exact wording in the policy will determine whether coverage applies.

Can You File Workers’ Comp & UM/UIM After a Company Vehicle Crash?

Workers’ compensation and UM/UIM coverage are separate systems, and one does not block you from using the other. If your employer has to workers’ comp, the Texas Labor Code § 408.001 generally restricts you from suing the employer directly for your injuries, but that rule does not stop you from filing a claim under a UM/UIM policy, because the claim is made against the insurer, not the employer.

Workers’ comp pays for medical care and a portion of lost wages (generally 70% of average weekly wages for most injured workers), but only after a waiting period and only up to legal limits. It does not pay for pain and suffering or the full loss of long-term income you may incur. UM/UIM coverage is built to cover these costs, which is why it makes sense to pursue both at once.

Employers who don’t offer workers’ comp are called “nonsubscribers.” If you work for a nonsubscriber and get hurt in a company vehicle crash, the rule that limits lawsuits against employers does not apply. You may be able to sue the employer directly for your injuries, in addition to UM/UIM claims, which can dramatically increase what you recover.

The value of these stacked claims depends on the severity of your injuries, the policies that apply, and how the employer’s insurer handles the dispute. Our breakdown of settlement values in company vehicle accident cases covers how these claims are typically valued, and we explore similar issues in rear-end commercial truck accident settlements, as well.

Talk to an Attorney About Your Company Vehicle Accident in Texas

Company vehicle crash claims involve commercial policies, personal policies, workers’ compensation, and sometimes direct lawsuits against an employer for your injuries. Sorting through which coverage applies requires a professional who has handled these disputes before.

Angel Reyes & Associates has more than 30 years of experience representing injured Texans. We have recovered more than $1 billion for clients across auto, commercial vehicle, and insurance dispute cases.

We work on contingency, meaning you pay no fee unless we win, and consultations are always free. If your employer’s insurer is telling you they offer no UM/UIM coverage, or you’re stuck between a workers’ comp claim and a denied insurance claim, contact us today to talk through your options at no cost to you.

Past results do not guarantee future outcomes.

UM/UIM Company Vehicle Accident FAQs

Is an employer required to notify employees that UM/UIM coverage was rejected on the company's commercial auto policy?

No, Texas law does not require employers to notify employees when they reject UM/UIM coverage on a commercial fleet policy. Workers have no automatic right to receive a copy of the rejection form or any written notice about the missing coverage.

Does Texas set a deadline for filing a UM/UIM claim after a company vehicle crash?

Yes, Texas has a two-year deadline for most personal injury claims, and UM/UIM claims generally follow the same window. Missing that deadline can permanently restrict you from recovering anything, regardless of how strong your claim is.

Can a passenger in a company vehicle file a UM/UIM claim, or does the coverage only protect the driver?

UM/UIM coverage typically protects all occupants of the covered vehicle, not just the driver. A passenger injured in a company vehicle crash by an uninsured driver can generally file a claim under the same commercial policy, as long as the coverage was not rejected.

If the at-fault driver had some insurance but not enough to cover my medical bills, does UIM coverage still apply?

Yes. Underinsured motorist coverage applies when the at-fault driver’s insurance is not enough to fully compensate your losses. You can claim the difference between what their policy pays and your total damages (up to your UIM policy limits).

Will a company vehicle crash affect my personal auto insurance rates even if I was not at fault?

It depends. Filing a UM/UIM claim under your personal policy can sometimes trigger a rate review, depending on your insurer and your policy terms. Texas law does not stop insurers from considering a not-at-fault claim when calculating your premiums, but some insurers choose not to raise your rates in that situation.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 70,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...