How UM/UIM Coverage Applies in Hit & Run Accidents

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- Texas treats an unidentified hit and run driver as uninsured, so UM coverage on your policy applies.

- Texas Insurance Code § 1952.104 requires physical contact with the fleeing vehicle to trigger UM coverage.

- Personal injury claims face a two-year deadline, but UM contract claims against your insurer have a four-year deadline.

You were heading home from work on I-35 when another driver clipped your rear quarter panel and kept going. By the time you pulled over, the car was just a pair of taillights disappearing into traffic. The police took your report, but there is no plate, no name, and no insurance company to call.

How UM Coverage Applies After a Hit & Run Accident

When the at-fault driver flees and cannot be identified, Texas law treats them as an uninsured motorist. That means uninsured motorist (UM) coverage on your own policy pays for your injuries and damages. In this case, you cannot rely on underinsured motorist (UIM) coverage because there is no identified driver to be underinsured.

UM coverage pays for bodily injuries and sometimes property damage when the at-fault driver cannot be found or has no insurance. The Texas Insurance Code § 1952.101 requires every auto insurer in Texas to offer UM/UIM coverage in every liability policy. You must reject it in writing, so most Texas drivers have this coverage without knowing it. If you are not sure whether you have UM coverage, check your declarations page or call your insurer.

The Texas Department of Insurance auto coverage glossary explains each coverage type in plain terms. UM coverage usually matches your liability limits and applies to anyone in your household who is covered by the policy.

Physical Contact Requirement Explained

Texas requires that the unidentified vehicle must have made physical contact with you or your vehicle for UM coverage to apply in a hit and run. This is the single most important rule for these claims. If there was no contact, then there is no automatic UM coverage. The rule is explained in Texas Insurance Code § 1952.104, and insurers follow it closely.

Direct Contact vs. Indirect Contact

Direct contact is the surest route to coverage. If a fleeing car strikes your vehicle, then the physical evidence (such as paint transfer, dents, and debris) should support your claim.

Indirect contact is also recognized in Texas case law but requires careful documentation. A common example is a chain collision. In this scenario, a fleeing driver forces another car into your lane, and that second car strikes you. Texas courts have allowed UM claims in this scenario, but you must have evidence that shows the unidentified vehicle caused the contact.

Phantom Vehicle Claims

A phantom vehicle claim arises when the fleeing driver never touches your car at all. For example, if a driver cuts you off, you swerve to avoid a crash, and you hit a barrier. These claims are much harder to prove because § 1952.104 was written with contact in mind.

Without physical contact, you typically need independent witnesses who saw the unidentified vehicle and can corroborate its role in the crash. The Office of Public Insurance Counsel’s hit and run guidance underscores how often these claims are denied without supporting testimony. Document the scene thoroughly and collect witness contact information before anyone leaves.

For more options when the other driver has no coverage, see what to do after a crash with an uninsured driver.

Filing a UM Claim After a Hit & Run in Texas

A UM claim moves faster when you take care of the first steps correctly. The insurer will look for a police report number, proof of where the vehicles made contact, and timely notice of the crash.

Each step below supports the others. Skipping any one of them will only give the insurer a reason to push back against your claim.

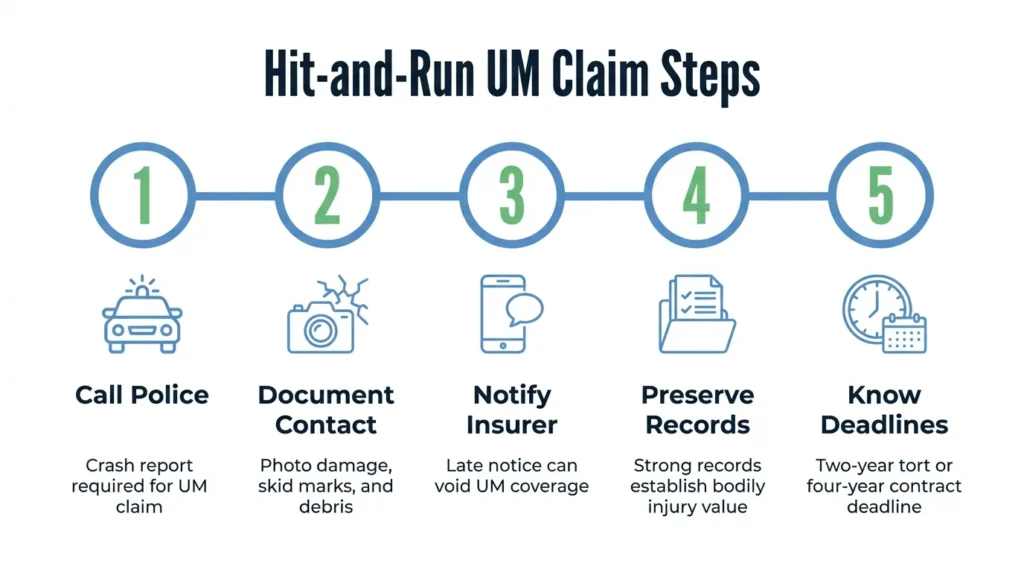

Step 1: Call the police at the scene. Texas Transportation Code § 550.021 requires you to stop, remain at the scene, and offer help after a crash involving injury or death. If the crash caused only vehicle damage, § 550.022 states that you must stop and exchange information. If the other driver flees the scene, you still must report the crash. A police report number is required for nearly every UM claim.

Step 2: Document everything. Take photos of the vehicle damage, the road, skid marks, and any debris. These images establish proof of physical contact, which the insurer will review.

Step 3: Notify your own insurer promptly. Most Texas auto policies require timely notice as a condition of your coverage. Delayed notice is one of the most common reasons insurers deny UM claims.

Step 4: Preserve medical records. UM bodily injury coverage pays for medical bills, lost wages, and pain and suffering. Strong medical records prove the value of your claim.

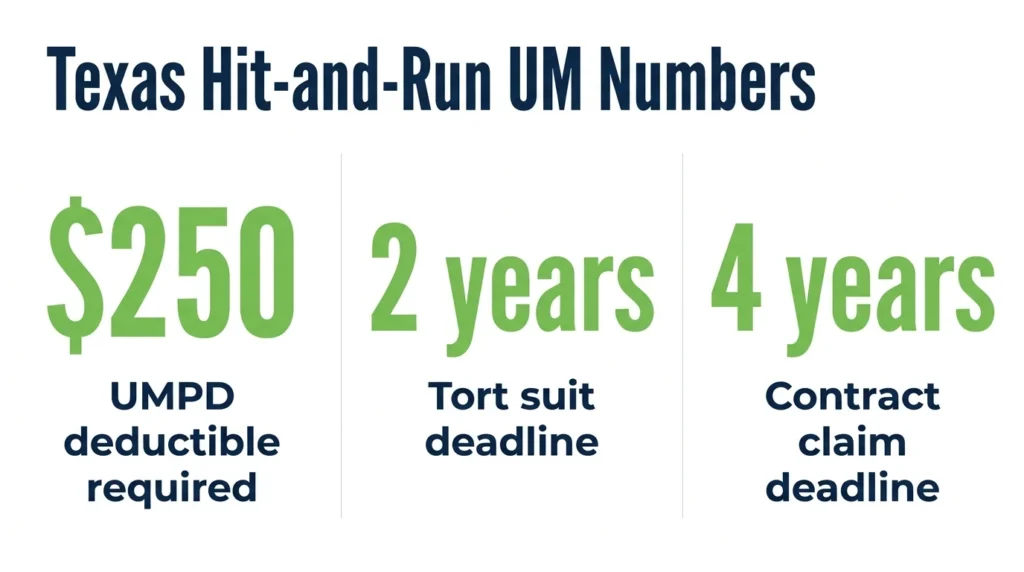

Step 5: Know your property damage rules. Uninsured motorist property damage carries a $250 deductible under Texas law. If you also carry collision coverage, that may be a faster way to get your vehicle repaired.

Personal injury protection (PIP) is worth looking into, too. PIP pays your medical bills regardless of who is at fault, and it does not require proof of physical contact. It can be a financial bridge while your UM claim is being processed. If you are not sure whether your policy includes UM or PIP, a Texas car accident attorney can review your declarations page with you.

If you were riding as a passenger, see how claims work for passengers in car accidents.

What To Do If Your Insurer Resists or Denies the Claim

A UM claim is made against your own insurer. The insurer steps into the shoes of the unidentified driver, which means it has a financial reason to dispute liability, challenge the contact requirement, and downplay your injuries. This is normal, and it is part of why these claims often benefit from legal help.

Texas bad faith insurance law applies when an insurer unreasonably delays or denies a valid UM claim. The bottom line is your insurer is required to handle your claim fairly.

Two different deadlines will apply to your case:

- The two-year deadline under Texas Civil Practice and Remedies Code (CPRC) § 16.003 applies to personal injury claims related to the crash.

- A breach-of-contract suit against your UM carrier generally has a four-year deadline under Texas contract law, but this deadline depends on when the insurer violated the policy.

The interaction between these two deadlines depends on the facts of the case, but waiting is risky, regardless of which legal strategy applies.

If the fleeing driver is later found, your claim can change. If the driver has some insurance but not enough, the claim may move from UM to UIM territory, depending on the driver’s coverage limits. Tell your insurer right away if the driver is identified.

Get Legal Help with Your Hit & Run UM Claim

Hit and run cases are harder to prove than most car accident claims because the at-fault driver is gone, and your own insurer may challenge the claim.

Angel Reyes & Associates has handled Texas UM and hit-and-run cases for decades, with more than $1 billion recovered for clients. We work on contingency, which means you pay no fee unless we win, and we offer free consultations. You can read about our firm and experience or contact us today to talk through your claim.

Past results do not guarantee future outcomes.

FAQs

Does filing a UM claim after a hit and run affect my insurance rates in Texas?

Filing a UM claim for a hit and run generally does not count against you as an at-fault accident under Texas law, but your insurer may still review your overall claims history when it is time to renew your policy. Checking your policy language and asking your insurer directly before filing can help you understand how it treats no-fault claims.

Can a passenger in my car make a UM claim after a hit and run in Texas?

Yes. Passengers injured in a hit and run may be covered under the vehicle owner’s UM policy, and they may also have access to UM coverage through their own auto policy (if they have one). Coverage depends on the policy language, so each passenger should check with their own insurer, as well.

Does Texas require a witness to support a hit and run UM claim?

No, Texas law does not require a witness in every case, but insurers are more likely to dispute a claim in which physical evidence is limited. A corroborating witness becomes especially important when damage is minor or physical contact is difficult to document from photos alone.

What if the hit and run happened in a parking lot, instead of a public road?

UM coverage under a Texas auto policy typically applies to crashes in parking lots, as well as public roads, because the coverage applies to the vehicle and its occupants, rather than the location. You should still file a police report if possible, since most insurers require one as part of the UM claims process.

Can I use UM coverage if I was on a motorcycle when the other driver fled?

Yes, Texas UM/UIM coverage requirements also apply to motorcycle policies, but not all insurers include UM coverage automatically on a motorcycle policy. You should check your declarations page to confirm whether UM was included or waived when you purchased the policy.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 70,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...