How Insurance Companies Handle Minor Car Accidents in Texas

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- If you are in a minor crash, document everything at the scene and report the incident to your insurer within 24 to 72 hours to avoid delays or disputes.

- Texas drivers have options for getting repairs paid, including filing against the at-fault driver's liability insurance or using their own collision coverage.

- Even minor crashes can involve disputed fault, hidden damage, or delayed injuries, so understanding when to seek guidance can protect your rights.

What to Expect After a Fender Bender

You were backing out of a parking spot near the Galleria in Houston when another driver clipped your bumper. The damage looks minor. Both of you exchanged information and went your separate ways. Now your phone is buzzing with calls from insurance adjusters, and you’re wondering what happens next.

Minor car accidents happen every day across Texas. The good news is that most fender benders resolve without major complications. The key is understanding how the insurance process works so you can protect yourself from unnecessary delays, disputes, or surprises.

What to Do Right After a Minor Crash in Texas

The first hour after a collision is more important than most people realize. What you do (and don’t do) at the scene can shape how smoothly your claim proceeds. The Texas Department of Insurance provides helpful guidance on these initial steps.

Start with safety: check that everyone is okay. Then focus on documentation:

- Exchange names, phone numbers, insurance information, and license plate numbers with the other driver

- Take photos of all vehicles involved, including damage close-ups and wide shots showing vehicle positions (do this before moving any vehicles out of the way)

- Photograph the surrounding area: street signs, traffic signals, weather conditions, and any visible skid marks

- Get contact information from any witnesses

Within the next 24 to 72 hours, notify your insurance company about the crash. Get at least one repair estimate. If you feel any pain or stiffness, even minor symptoms, see a doctor and document the visit.

How Insurance Claims Work After a Minor Accident

Once you report the crash, an adjuster is assigned to investigate. They’ll review your statement, the other driver’s statement, photos, and any police report. They’ll also inspect vehicle damage, either in person or through photos.

The adjuster then makes a liability determination. This is their conclusion about who was at fault and to what degree.

Common Mistakes That Complicate “Simple” Claims

While a low-speed accident may seem like a simple matter, it’s important to remember that insurance companies are in the business of minimizing payouts as much as possible. Minor accidents are no exception.

Avoid admitting fault at the scene. Stick to observable facts when speaking with the other driver or police. Saying “I’m sorry” or guessing about what happened can be used against you later.

Don’t agree to “handle it privately” without documenting everything first. Cash agreements often fall apart when the other driver changes their mind or hidden damage appears.

Even if you feel fine initially, don’t skip medical documentation if symptoms develop later. Whiplash and soft tissue injuries often don’t appear until hours or days after a low-speed collision.

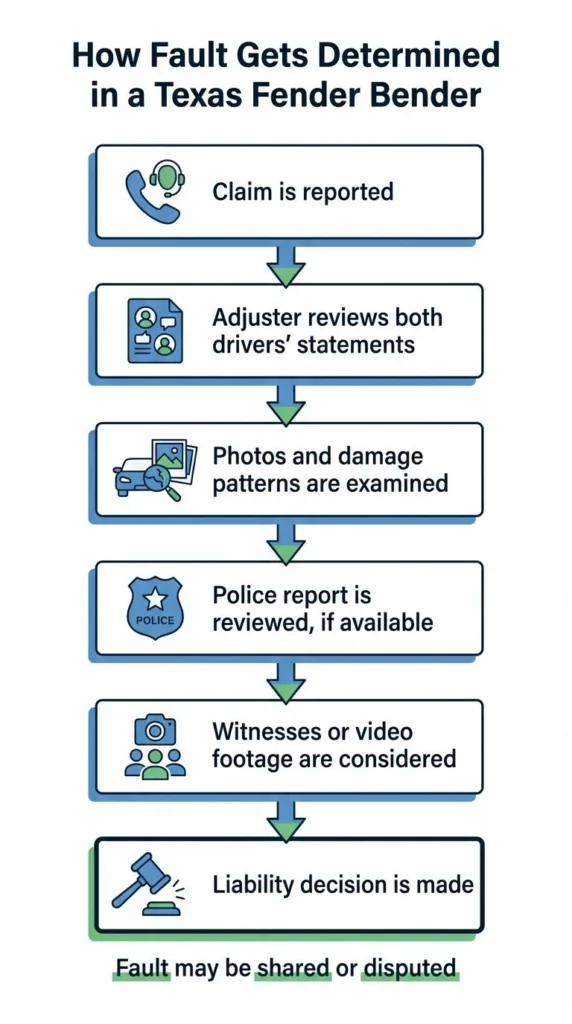

How Fault Gets Determined in Fender Benders

Ultimately, it’s these insurance adjusters who determine fault. They look at:

- Statements from both drivers

- The police report (if available)

- Photos showing damage location and severity

- Vehicle damage patterns (rear-end damage usually points to the trailing driver)

- Witness accounts

- Any available video footage

Common fender-bender scenarios like rear-end bumps or parking lot collisions each have typical fault patterns. But adjusters can still dispute liability if the evidence is unclear or stories conflict.

Recorded Statements & Document Requests

The other driver’s insurance may ask for a recorded statement. You’re generally not required to give one to the other driver’s insurer, though your own policy may require cooperation with your insurer.

If you do give a statement, stick to facts you know. Don’t speculate or guess. Keep answers brief and accurate.

Be cautious about signing broad medical authorizations. It’s reasonable for an insurer to request records related to crash injuries. It’s less reasonable for them to request your entire medical history. If requests feel overly broad, you can ask questions or seek guidance.

Do You Need a Police Report to File a Claim?

Many minor accident claims proceed without a police report. In some cases, especially for incidents occurring on private property and with no injuries involved, law enforcement may not even send an officer out.

Texas law doesn’t require you to call police for every fender bender, though Texas Transportation Code Chapter 550 outlines certain reporting duties.

However, a police report becomes more valuable when:

- The other driver’s story differs significantly from yours

- Someone leaves the scene

- You suspect the other driver was intoxicated

- Injuries develop later

Without a report, your photos and documentation become even more critical for supporting your version of events.

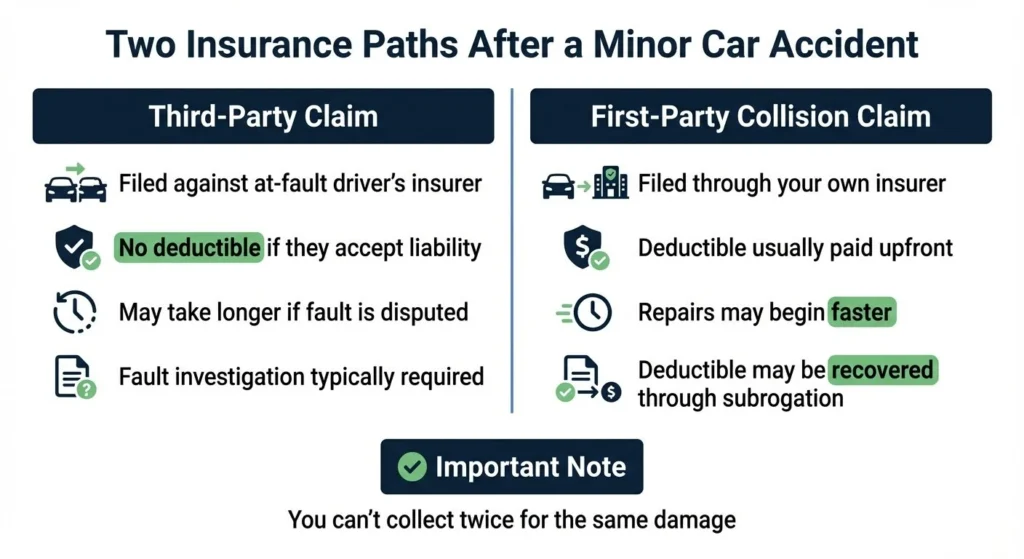

Two Paths to Getting Your Car Fixed

You generally have two options for having your car fixed after an accident:

Third-party claim: Filing a claim against the other driver’s insurance is the most direct way to have your car fixed when the incident is their fault. The upside is you don’t have to pay your deductible. The downside is that you’re waiting on their insurer’s investigation, which can take longer if fault is disputed.

First-party collision claim: You can also use your own collision coverage. You’ll pay your deductible upfront, but repairs often start faster. If your insurer later recovers money from the at-fault driver’s insurance through subrogation, you may get your deductible back.

Some people open both claims early to keep options open. This isn’t “double-dipping.” You can only collect once for the same damage.

Timelines, Delays & Keeping Your Claim Moving

Report the crash to your insurer as soon as reasonably possible. Late notice can give insurers grounds to question or deny claims.

Once an insurer accepts a claim, Texas regulations set expectations for payment timing. But “prompt pay” rules have specific conditions. If your claim is delayed without clear explanation, the TDI can help you understand your options.

To keep things moving:

- Keep a claim diary noting every call, email, and document you send or receive

- Confirm important conversations in writing

- Send documents in organized batches rather than piecemeal

- Follow up if you don’t hear back within the timeframe the adjuster promised

Property Damage Settlements: Repairs, Estimates & Surprises

For property damage, the insurer typically sends an adjuster or asks you to get estimates. Initial estimates often don’t catch everything. You generally have the right to choose your own repair shop. Some insurers have “preferred” shops, but you’re not required to use them.

Supplements are common. Once a body shop starts work, they may find hidden damage. When this happens, the shop submits a supplement request, and the insurer reviews it. This is normal, not a red flag.

Watch for situations where “minor” damage turns out to be more serious:

- Modern vehicles have sensors and safety systems that can be damaged in low-speed impacts

- Frame or alignment issues may not be visible

- If repair costs approach a certain percentage of your vehicle’s value, the insurer may declare it a total loss

Medical Bills After a “Minor” Crash

Low-speed collisions can still cause injuries. Whiplash, back strain, and soft tissue injuries don’t always show up immediately.

If you experience any symptoms, see a doctor and keep records of:

- Appointment dates and providers

- Symptoms and how they affect daily activities

- Out-of-pocket costs (copays, prescriptions, medical equipment)

- Any work missed due to injury

PIP or MedPay can help cover initial medical costs while fault is being determined. This can be especially helpful for covering deductibles or copays.

Be cautious if an adjuster pushes for a quick settlement before you’ve finished treatment or fully understand your injuries. Once you sign a release, you typically can’t reopen the claim if problems develop later.

When to Consider Getting Legal Help

Most fender benders resolve without needing an attorney. But some situations benefit from professional guidance:

- If fault is disputed and the other driver’s story contradicts yours

- If you’ve developed injuries that require ongoing treatment

- If the insurer denies your claim or offers significantly less than your documented damages

- If you’re being pressured to settle quickly or sign documents you don’t fully understand

- If the “minor” crash is affecting your ability to work

A consultation can help you understand your options without committing to anything. At Angel Reyes & Associates, we offer free consultations and work on contingency, meaning no fee unless we win. With over 30 years of experience helping Texas drivers, we can review your situation and help you decide the best path forward.

If you’re unsure whether your claim needs attention, reach out to us for a no-pressure conversation.

Minor Accident FAQs

Can I get a rental car after a minor accident in Texas?

If the other driver caused the crash, their insurer should cover a rental car for you. If fault is still being investigated you may need rental reimbursement coverage on your own policy to get one sooner.

Do I have to pay my deductible if the other driver was at fault for a Texas fender bender?

That depends. If you wait for the investigation to conclude first, then the other driver’s insurance should cover everything. But if you file with your own collision coverage first, you’ll usually pay the deductible up front, and your insurer will try to recover it for you through subrogation.

Will a minor accident claim raise my insurance rates in Texas?

Not automatically. The Texas Department of Insurance says insurers can’t raise your premium just for filing a claim, but a paid claim or accident history can still affect your rates.

Will my own insurance pay for diminished value after a minor crash in Texas?

Usually not if the vehicle is fully repaired under your own policy. A first-party insurer does not have to pay diminished value when the car has been completely repaired to its pre-damage condition.

What if the driver who hit me in a parking lot has no insurance or leaves the scene?

Your uninsured/underinsured motorist coverage may help with the damage, and TDI says that coverage can also apply to hit-and-run accidents when the other driver leaves before you can get insurance information.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 70,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...