Bobtail Insurance for Truckers in Texas

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- Bobtail insurance covers you off dispatch when the carrier's primary policy stops responding.

- Bobtail and NTL obligations come from your lease, not from Texas or federal law.

- Liability-only bobtail policies often run $30 to $60 per month for owner-operators.

You just dropped a load near the Port of Houston and you are deadheading back toward I-10 with no trailer behind you. A car cuts in front of your tractor, you brake hard, and metal meets metal. Then it hits you. You are off dispatch right now, so whose insurance pays for this?

That single question decides whether you walk away covered or face a claim out of your own pocket.

What Bobtail Insurance Covers

Bobtail insurance is liability protection that applies when your tractor operates without a trailer and you are no longer under an active dispatch, but still tied to a motor carrier’s authority. It covers the exact gap most owner-operators never see coming.

When you are off dispatch, the motor carrier’s primary commercial auto policy does not apply. You are personally on the hook for any accident that happens in that window. Bobtail coverage steps in to fill it.

The term describes how the truck is moving. You are running the tractor without a trailer attached, often between a delivery drop-off and your next pickup, or heading back to the terminal empty.

What bobtail pays for has limits worth knowing before you sign anything. A bobtail policy typically provides bodily injury and property damage liability for harm you cause to others. It does not cover physical damage to your own truck. That protection requires a separate policy.

If you are not sure whether your carrier policy covers you once you drop the trailer, understanding the broader commercial trucking insurance framework helps.

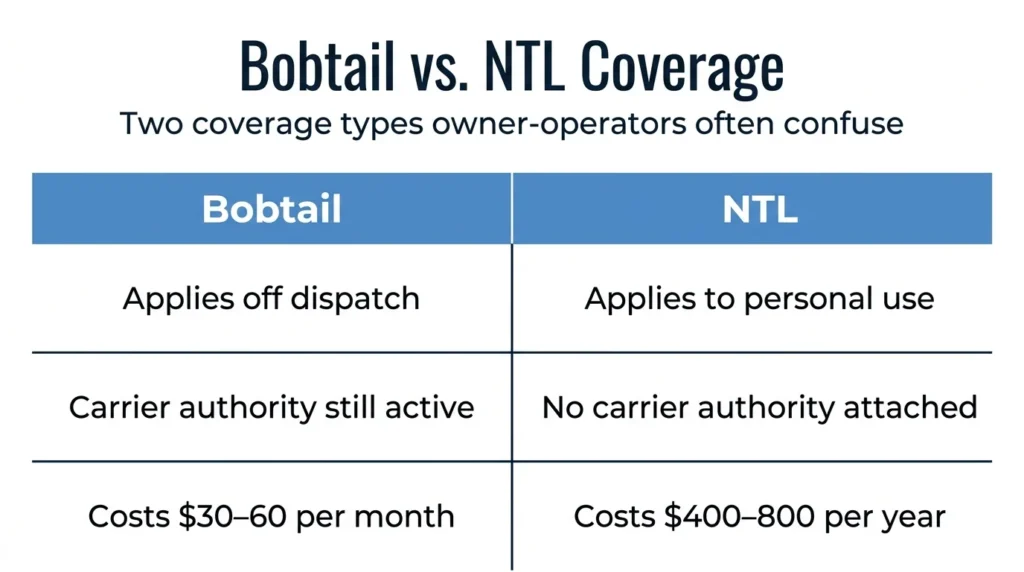

Bobtail vs. Non-Trucking Liability

Bobtail and non-trucking liability are the two coverage types owner-operators confuse most often when reviewing a lease. The difference comes down to one question: are you still tied to the carrier’s authority, or are you using the truck for yourself?

Bobtail Insurance

Bobtail coverage applies when you are off dispatch but still operating under the motor carrier’s authority. The carrier’s authority status is the trigger, not whether a trailer is attached.

This covers the gaps between active dispatches. You are running from a drop-off to your next pickup, heading back to the terminal, or pulling into a fuel stop between loads.

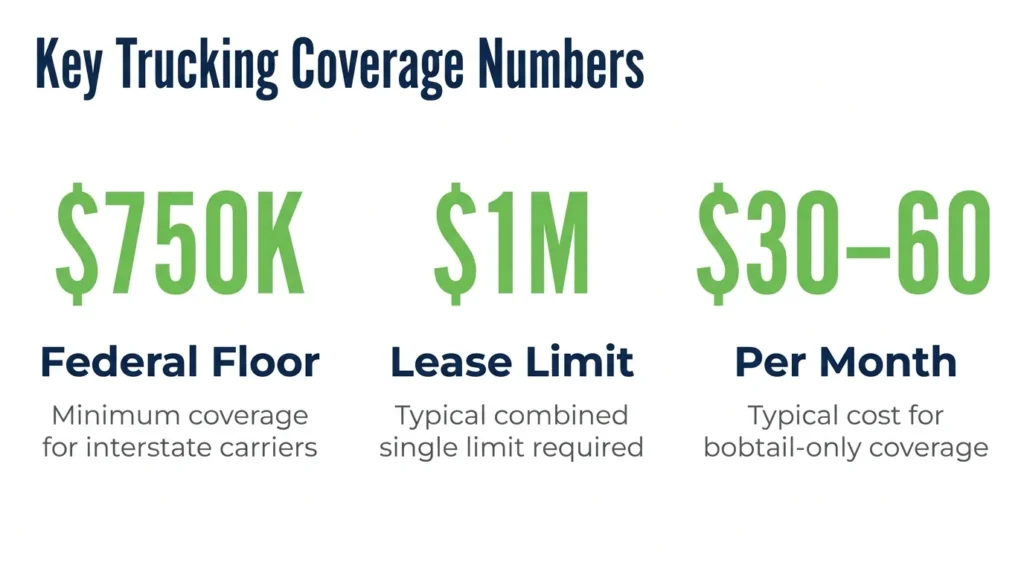

Most carrier leases set a $1,000,000 combined single limit as the required insurance amount. The lease defines what “under dispatch” means, not you. Some carriers use shell entities and layered authority structures that make those definitions harder to read.

Non-Trucking Liability

Non-trucking liability, or NTL, applies when you use the truck for fully personal purposes, completely off any dispatch and carrier authority. Your use of the vehicle is the trigger here, not the carrier’s authority.

This is the coverage for personal trips. You are running errands, driving the truck home for a personal weekend, or using it for yourself with or without a trailer attached.

Here is where drivers get caught. If you are hauling a personal trailer during personal use, a bobtail-only policy may leave that exposure uncovered. NTL is the right coverage for those situations, and the distinction shows up in many real truck accident cases.

Texas Trucking Insurance Requirements

No federal regulation and no Texas statute independently requires you to carry bobtail or NTL coverage. Both obligations come from your lease, not from the government. Understanding the legal backdrop shows you why.

At the federal level, FMCSA regulations set the minimum financial responsibility for interstate motor carriers. The general freight floor for property carriers is $750,000, set under 49 C.F.R. § 387.9. These thresholds apply to the carrier’s primary policy.

A separate coverage layer applies if you run intrastate. Texas Transportation Code Chapter 643 requires motor carriers operating within Texas to register with TxDMV and carry minimum liability insurance. Section 643.101 sets the amount, and § 643.103 requires proof of insurance filed and kept on record with TxDMV.

Neither of those coverage layers requires bobtail or NTL from you directly. Your carrier creates that obligation in the lease. The carrier shifts the off-dispatch exposure onto you and spells out the coverage type and limits you must carry, which connects directly to how truck accident liability gets assigned after a crash.

Bobtail Insurance Cost in Texas

Liability-only bobtail policies for owner-operators often run $30 to $60 per month, depending on driving record, garaging ZIP code, and coverage limits selected. NTL policies typically cost $400 to $800 per year per truck. Your actual rate depends on a handful of factors you can partly control.

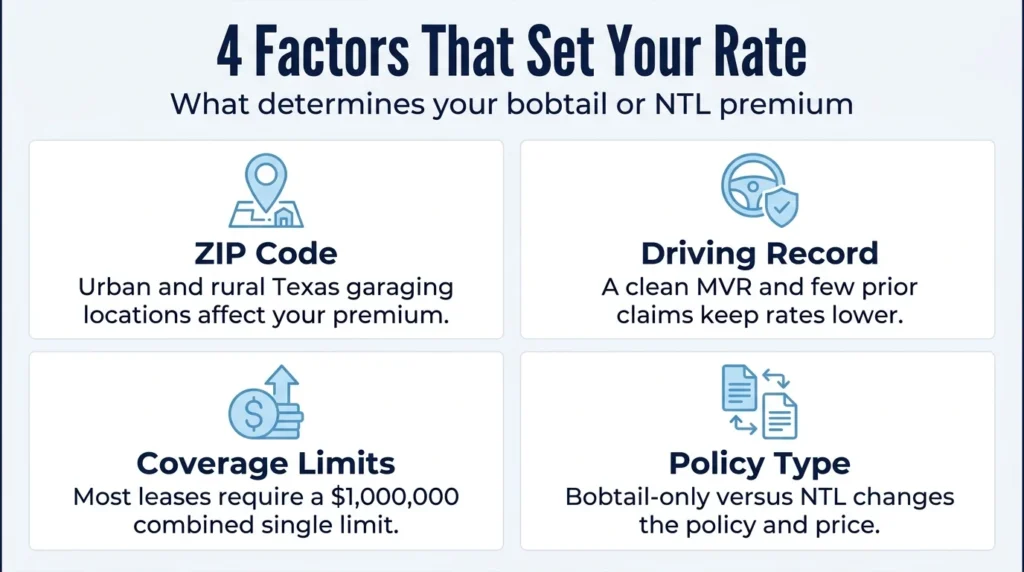

Four things determine what you pay for bobtail or NTL coverage.

- Garaging ZIP code: Urban and rural Texas rates differ, and where you keep the truck affects your premium.

- Motor vehicle record and claims history: A clean MVR and few prior claims keep your rate lower.

- Coverage limits selected: Most leases require a $1,000,000 combined single limit, which sets your baseline.

- Bobtail-only versus NTL: Which one your lease requires changes the policy and the price.

The cheapest policy is not always the best option. One that denies claims over an ambiguous dispatch definition costs you far more after a wreck than the few dollars it saved each month.

Before you buy, read how the policy defines “under dispatch” and check that it matches your lease language word for word. If a claim does get denied after an accident, you may have options beyond fighting the insurer alone, starting with filing a commercial vehicle insurance claim.

Discuss Your Case With an Experienced Attorney

A coverage gap or a denied bobtail claim can leave you facing a serious accident with no insurer standing behind you. That is the moment to have someone who knows how carriers and insurers shift liability onto drivers.

Angel Reyes & Associates has spent over 30 years helping injured Texans and truckers work through accidents, coverage disputes, and underinsured drivers. We have recovered more than $1 billion for clients, and we work on a no fee unless we win basis, so there is no upfront cost to you.

Your first consultation is free.

If an accident left you fighting a denied claim or an underinsured driver, reach out to us for a free consultation. You can learn more about our team and track record, and how we handle Dallas truck accident claims.

Past results do not guarantee future outcomes.

Bobtail Insurance FAQs

Does bobtail insurance cover physical damage to my tractor?

No. Bobtail insurance is a liability policy, so it pays for injuries and property damage you cause to others. Damage to your own truck requires a separate physical damage policy.

Does bobtail insurance cover cargo I am carrying?

No. Bobtail coverage does not extend to cargo. Cargo loss or damage is covered by a separate motor truck cargo policy, which is a distinct line of insurance from bobtail or non-trucking liability.

What personal liability do I face if I cause an accident while off dispatch with no coverage?

Without bobtail or non-trucking liability in force, you are personally responsible for the other party’s bodily injury and property damage claims. A judgment against you can attach to your personal assets, including savings and future earnings.

Can a bobtail claim be denied even if I have a policy in force?

Yes. Insurers can deny claims when their policy’s definition of “under dispatch” or “personal use” does not match the circumstances of the accident. If your policy language and your lease agreement define dispatch differently, that gap is often what triggers a denial.

Does my bobtail coverage apply if I am off dispatch while driving outside Texas?

Most bobtail policies are not limited to a single state and will apply wherever the covered vehicle is operating at the time of the accident, but the actual coverage territory depends on your specific policy language. Review your declarations page to confirm your policy does not contain a geographic restriction.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 55,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...