How Insurance Companies Estimate Car Repair Costs

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- Texas law lets you choose any licensed repair shop, no matter what the insurer recommends.

- Adjuster estimates come from software that creates estimates before the car is disassembled, and it often misses hidden collision damage.

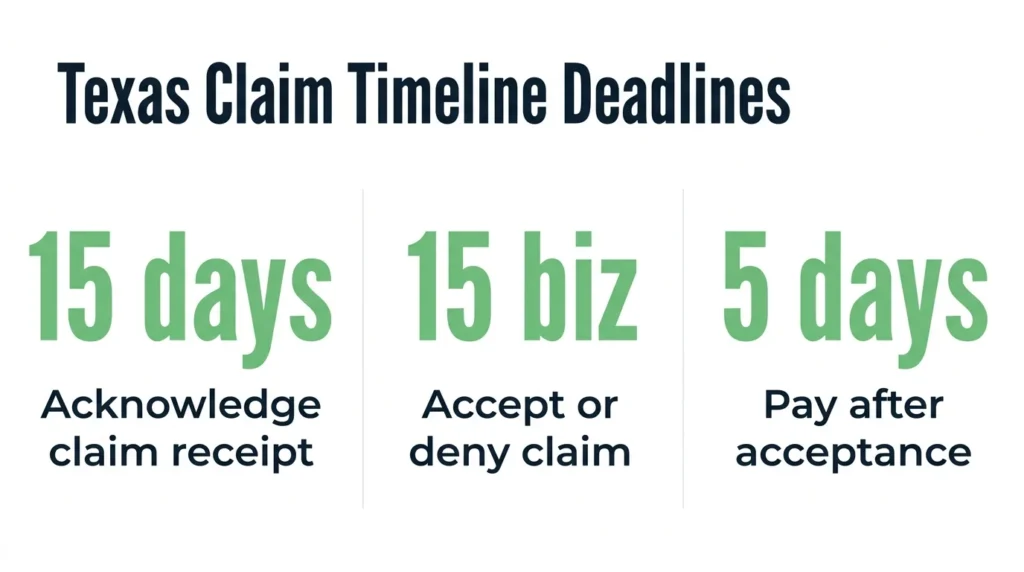

- Insurers must acknowledge a claim within 15 days of receipt and pay within 5 business days of accepting the claim.

You were rear-ended on I-35 near Round Rock on your way to work, and your bumper is barely hanging on. The other driver’s insurer called fast, sent you to a shop on their list, and emailed an estimate that feels hundreds of dollars lower than the repairs will actually cost. Now, you’re wondering whether you have to use their shop and accept their estimate.

How Insurers Produce a Repair Estimate

An insurance repair estimate is a software-generated cost estimate, not a thorough inspection. Adjusters use programs like CCC ONE or Mitchell, which pull regional labor rates and parts prices from a database. This initial cost estimate is only the insurer’s starting point for negotiations. It does not reflect what a certified technician may find once the vehicle is taken apart.

Adjusters produce these estimates in different ways:

- Some will review photos remotely.

- Some will meet you at a drive-in inspection site.

- Some will send a field appraiser to look at the car in person.

Each method carries a different risk of missing damage hidden behind a panel or under the bumper cover.

The pricing inside the software often does not reflect real-world shop rates. It may not account for diagnostic scans, structural calibration, or corrosion protection, all of which modern repairs require. That difference is how most disputes start.

The estimate is the starting figure, not the limit. If a body shop finds more damage while they are taking the car apart, the shop can request additional money through a supplemental claim. The Texas insurance claim investigation process explains how adjusters build their initial estimate.

Preferred Body Shop Networks & How They Work

A direct repair program is a contract between an insurer and a body shop. The shop agrees to use the insurer’s labor rates, parts sources, and repair procedures. In exchange, the insurer feeds the shop a steady stream of repair claims. This efficiency benefits the insurer’s bottom line, but not necessarily the quality of your repairs.

Direct repair program shops often use aftermarket or recycled parts when insurer pricing will not support original equipment manufacturer parts. Original equipment manufacturer parts come from your vehicle’s original maker, and they match factory specifications. Aftermarket parts are made by third parties and may differ in fit, finish, and crash performance. For newer vehicles, you can push back and ask for original equipment manufacturer parts.

Insurers push claimants toward in-network shops via estimate paperwork, adjuster suggestions, and warranty offers. This pressure can feel like a rule, even though it is only a recommendation. In the TDI Commissioner’s Bulletin B-0026-11, the Texas Department of Insurance warns insurers not to pressure claimants into choosing specific shops.

Texas Claimant Rights When Choosing a Repair Shop

In Texas, you get to choose the repair shop. The Texas Insurance Code § 1952.301 restricts insurers from directly or indirectly limiting coverage by specifying the parts or repair shop you must use. An insurer can recommend a shop, but it cannot require one as a condition of paying your claim.

Two related sections back this up:

- Texas Insurance Code § 1952.302 prohibits insurers and adjusters from stating or implying, either in speech or in writing, that you must use a specific shop.

- Texas Insurance Code § 1952.305 requires the insurer to give you written notice of your right to choose the shop and the parts that you want when you present your vehicle for a damage claim.

It’s critical to get this written notice. If the insurer never gives it to you, the omission is a violation on its own, regardless of whether pressure was applied to choose their parts and their shop.

Insurers sometimes pay lower reimbursement rates for non-preferred shops to punish you for choosing an independent shop. However, this counts as an indirect coverage limit and violates both § 1952.301 and the unfair settlement practice rules in Texas Insurance Code § 541.060.

If an insurer pressures you to use a specific shop, you can push back in writing. Review the property damage claims process after a car accident to see your full options.

Why Estimates Differ & When to File a Supplemental Claim

Adjuster estimates are built before the car is disassembled at the shop. Body shop estimates are built during disassembly. This difference is the single biggest reason the two estimates diverge. Hidden structural damage, bent brackets, and corrosion can only become visible after a technician pulls the bumper, fender, and/or quarter panel apart.

Several common repair costs are often missing from the adjuster’s initial estimate, including:

- Diagnostic scans (required after most modern collision repairs to reset airbag and ADAS sensors)

- Paint blending on adjacent panels

- Wheel alignment after a hard impact

A supplemental claim is a formal request for more repair money if the original estimate was too low. The body shop documents the newly found damage with photos and parts invoices. The shop sends the supplement to the adjuster, who reviews it and approves or pushes back.

Texas Insurance Codes § 542.055, § 542.056, and § 542.057 set the deadlines that the insurer must meet. The carrier must acknowledge the claim within 15 days of receipt. It must accept or deny the claim within 15 business days of receiving all required items. It must pay within five business days of acceptance. These deadlines apply to supplemental claims, too.

When the shop and the insurer cannot agree on the costs, your policy may include an appraisal clause. In this case, each side picks a licensed appraiser, and the two appraisers select a neutral umpire. The umpire resolves the disagreement, and the result must be accepted by both sides.

Understanding how car accident claims work in Texas can help you spot when an insurer’s timeline is slipping past the deadline.

When to Talk to an Attorney After a Texas Car Accident

When insurers give you a low repair estimate, try to steer you towards a specific shop, or stall your supplemental claim, you can end up paying out of pocket for damage that was never your fault. You do not have to handle that fight alone. Angel Reyes & Associates has over 30 years of experience handling Texas car accident claims, with more than $1 billion recovered for clients.

We work on contingency, which means you pay no fee unless we win, and consultations are always free. You can read more about our firm before you decide. When you’re ready, contact us today to talk through your repair estimate and your options.

Past results do not guarantee future outcomes.

Insurance Company Car Repair Estimate FAQs

Can I get my own independent appraisal before accepting an insurance repair estimate?

Yes, you can hire an independent appraiser to assess your vehicle before agreeing to any settlement figure. Their written findings can serve as documentation if you need to dispute the insurer’s estimate.

Does Texas require a body shop to be licensed before it can repair my vehicle?

Yes, Texas requires auto body shops to hold a license issued by the Texas Department of Motor Vehicles under the Texas Occupations Code. Choosing an unlicensed shop could affect both your repair quality and your ability to seek recourse if the work is substandard.

Will my car's value drop after a collision even if it is fully repaired?

Yes, Texas courts recognize diminished value as recoverable damages. Diminished value is the reduction in a vehicle’s market value even after repairs are completed. You may be able to claim that loss from the at-fault driver’s insurer in addition to your repair costs.

What happens if the insurer declares my car a total loss instead of approving repairs?

When repair costs approach or exceed a threshold percentage of the vehicle’s actual cash value, the insurer may declare the vehicle a total loss and offer a cash settlement instead of paying for repairs. In Texas, you have the right to dispute the insurer’s valuation of your vehicle if you believe the offered amount is too low.

Are rental car costs covered while my vehicle is being repaired after a collision?

It depends on whether you carry rental reimbursement on your own policy or the at-fault driver’s liability policy extends to loss-of-use costs. Texas law allows claimants to seek loss-of-use damages from an at-fault party, but the amount and duration are limited.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 70,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...