Does Health Insurance Cover Motorcycle Accident Injuries in Texas?

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- Health insurance generally covers motorcycle crash injuries at the point of care in Texas.

- Texas caps health plan subrogation at half your recovery, but ERISA plans can ignore it.

- Riders 21 and older must carry health coverage for crash injuries to legally ride without a helmet in Texas.

You were riding home through Deep Ellum when a driver turned left across your lane and put you on the pavement. Now you are looking at an emergency room bill, a follow-up surgery, and weeks off work. The first question keeping you up at night is simple: will your health insurance actually pay for any of this?

Does Health Insurance Cover Motorcycle Injuries?

Yes. Health insurance generally covers motorcycle accident injuries in Texas, just as it covers any other medical need. Your plan pays for medically necessary treatment regardless of how you got hurt.

That coverage is the full scope of your care. Emergency treatment, hospital stays, surgery, rehabilitation, and follow-up visits tied to the crash all fall under a standard health plan.

At the moment you walk into the ER, the answer is almost always yes. The complications come later, after your treatment is paid and a settlement enters the picture.

Motorcycle injuries also tend to run more severe than other crash injuries, which means bigger bills and more reason to understand your coverage early. Texas roads see thousands of rider injuries every year, and there are distinct patterns to be aware of.

Motorcycle Exclusions in Health Insurance Policies

Some health plans contain exclusion language that tries to deny coverage for injuries you suffer while riding a motorcycle. Whether that exclusion holds up depends entirely on what kind of plan you have and which law governs it.

If you received a denial letter citing a motorcycle exclusion, do not treat it as the final word. The same exclusion can be unenforceable on one plan and fully valid on another.

Are Motorcycle Exclusions Enforceable Under Texas Law?

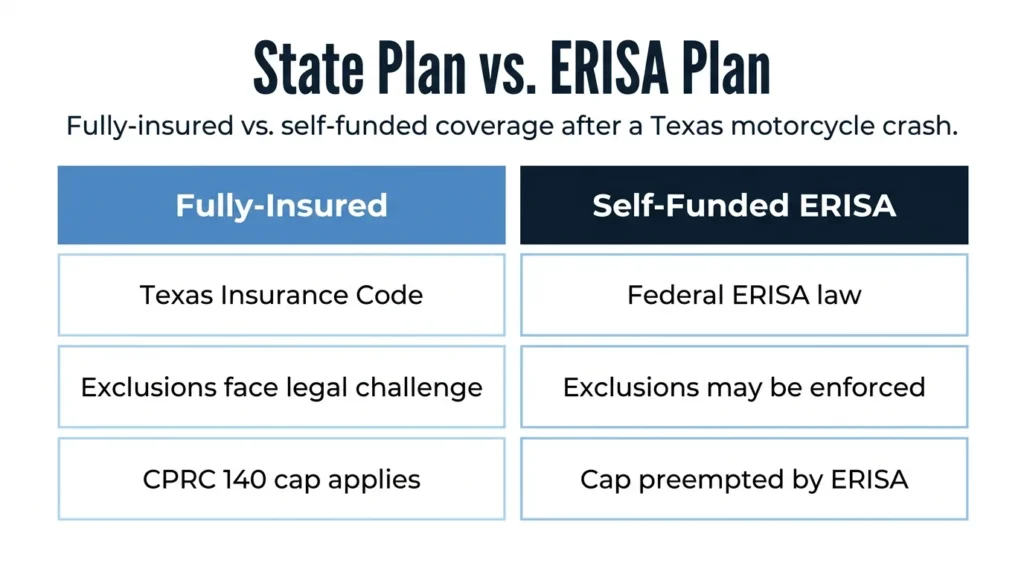

For state-regulated plans, Texas law and public policy create real obstacles to enforcing a blanket motorcycle exclusion. A fully-insured plan, the kind you buy on the individual market or get through many smaller Texas employers, has to follow state coverage rules.

The Texas Insurance Code’s Title 8 (Health Insurance and Other Health Coverages) establishes the coverage mandate framework that applies to state-regulated health benefit plans. A broad motorcycle exclusion can conflict with those coverage mandates, though which provisions apply depends on the specific plan type.

That conflict gives you room to push back. Before you accept a denial, review the exact policy language and have an attorney check whether the exclusion can be used on your plan.

ERISA Plans & Preemption

Here is where the answer can flip. If you get coverage through a self-funded employer plan, federal law called ERISA governs it instead of Texas insurance law. ERISA’s preemption clause stops Texas from regulating these plans the way it regulates fully-insured policies.

The practical result is harder to hear. An exclusion that Texas would block on a state-regulated plan can survive on a self-funded ERISA plan, and the state protections you might expect simply do not apply.

So your first move is to find out which kind of plan you have. Ask your employer or your benefits administrator whether the plan is self-funded or fully-insured before you assume Texas law protects you.Your plan type influences how your motorcycle settlement works.

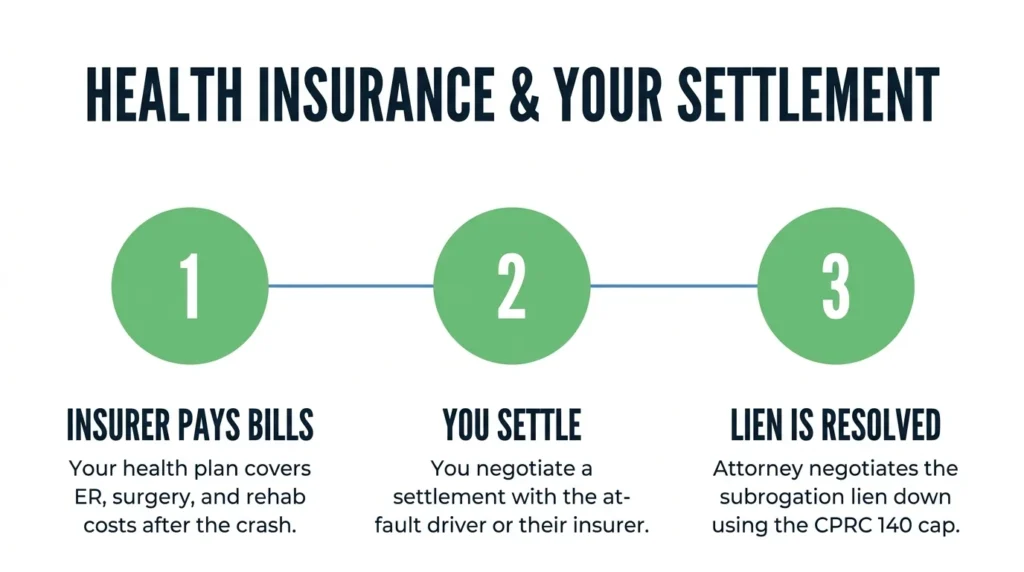

Health Insurance Subrogation & Your Settlement

Subrogation is your health insurer’s right to get paid back out of your injury settlement for the bills it covered. Most Texas health plans assert this right once you reach a settlement with the at-fault driver.

In plain terms, your insurer pays your medical bills now and then takes a slice of your settlement later. This is the same reimbursement principle that shapes auto insurance recovery, and the rules track closely with how auto subrogation works in Texas.

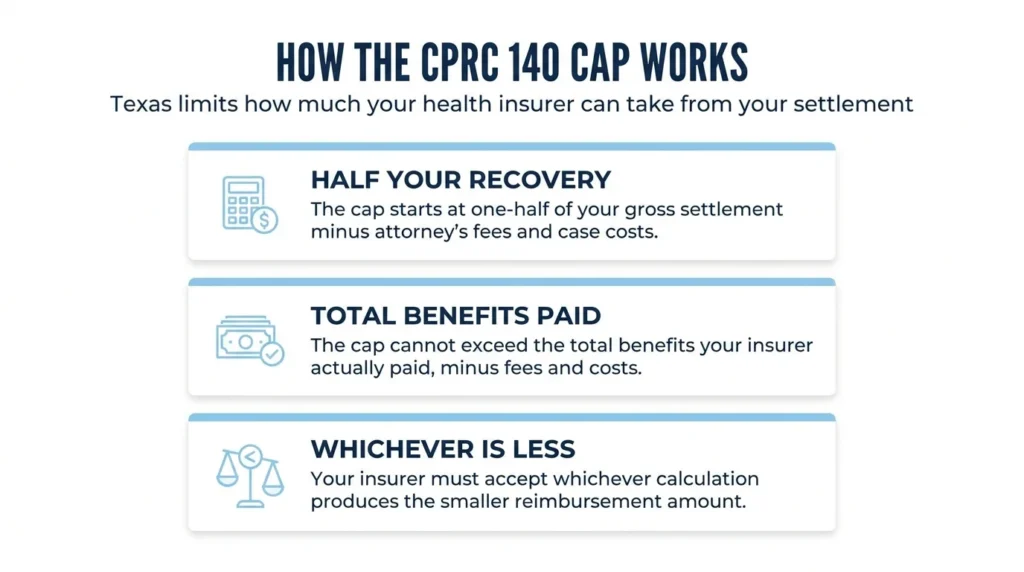

Texas puts a hard limit on how much a health plan can claw back. Under Texas Civil Practice and Remedies Code (CPRC) Chapter 140, a plan’s recovery is capped at the lesser of one-half of your gross recovery (minus attorney’s fees and case costs) or the total benefits it paid (also minus those fees and costs). When you have legal representation, the cap works in your favor twice: once to limit the insurer’s share, and again because attorney’s fees come off the top before the cap is calculated.

That cap is one of the strongest protections you have. It means a health plan cannot take so much that you walk away with almost nothing.

The cap has a major exception. A self-funded ERISA plan is not bound by CPRC Chapter 140 because ERISA’s preemption clause stops Texas from regulating these plans the way it regulates state-regulated policies. If your coverage runs through that kind of employer plan, you may face a demand for full-dollar reimbursement.

The Chapter 140 cap itself is the primary tool an attorney can use to push the lien down. Unlike some states, Texas does not allow a health plan to invoke full reimbursement rights when the cap applies. An attorney can use the cap formula to negotiate the lien to its floor, maximizing what you take home.

Texas Helmet Law & Health Insurance

Texas ties your health insurance directly to whether you can legally ride without a helmet. Under Texas Transportation Code §661.003, a rider 21 or older may ride without a helmet only if covered by a health insurance plan that provides benefits for medical expenses incurred as a result of a crash.

Texas removed a prior dollar minimum from this requirement, but the plan must still genuinely cover motorcycle accident injuries. A plan with a blanket motorcycle exclusion would not qualify.

If you ride under this exemption, confirm your plan actually covers motorcycle crash injuries. A plan with a motorcycle exclusion may not qualify, which leaves you with both a compliance problem and a hole in your coverage. The Texas Department of Insurance publishes guidance on motorcycle coverage that can help you check.

Going without a helmet can also affect your settlement. If you were not wearing one, Texas proportionate responsibility rules under Texas Civil Practice and Remedies Code (CPRC) Chapter 33 may shift some fault onto you. That can lower your total recovery, and the smaller your settlement, the smaller the pool your insurer’s lien comes out of.

These pieces stack on each other in ways that affect your bottom line. Helmet compliance, coverage, and fault allocation all feed into what you actually take home, which starts with who pays your medical bills after a crash.

Work with an Experienced Attorney

Angel Reyes & Associates has over 30 years of experience representing injured Texas riders, and we know how tangled health coverage gets after a crash. If your insurer is asserting a subrogation lien, sending a denial based on a motorcycle exclusion, or you are unsure how ERISA preemption affects you, we can help you work through both the legal and financial side.

Our team handles motorcycle accident claims across the state, and you can meet the attorneys who would handle your case. You pay no fee unless we win, and we cover case costs unless we recover for you. Reach out to schedule a free consultation.

Motorcycle Accident Health Insurance Coverage FAQs

What if my motorcycle crash was a solo accident with no other driver involved?

If there is no third-party settlement, your health insurer generally has no fund to attach a subrogation claim to, so it pays your bills without seeking reimbursement. Your coverage still applies at the point of care regardless of fault.

Does medical payments coverage on my motorcycle policy pay before my health insurance?

Yes. If your motorcycle policy includes MedPay, it typically pays first and can cover deductibles and copays your health plan would not otherwise pick up. Once MedPay limits are exhausted, your health insurance takes over as the primary payer.

Can a health insurer negotiate its lien before my case settles, or only after?

Lien negotiation can happen at any point during your case, including before a final settlement is reached. Starting those talks early can give you a clearer picture of your net recovery before you agree to a settlement amount.

Does the made-whole doctrine protect me if my plan is an ERISA self-funded plan?

For most self-funded ERISA plans, it does not. Federal courts, including the Fifth Circuit, have generally held that ERISA preempts the made-whole doctrine, meaning the plan can demand full reimbursement even if you have not recovered all of your losses.

How long do I have to file a motorcycle accident lawsuit in Texas?

Texas gives you two years from the date of the crash to file a personal injury lawsuit under Texas Civil Practice and Remedies Code Section 16.003. Missing that deadline typically bars you from recovering anything through the courts.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 55,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...