How Subrogation Works in Motorcycle Accident Claims in Texas

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- Texas CPRC Chapter 140 caps private health insurer liens at one-half of your gross recovery minus a proportional share of attorney fees and costs.

- ERISA self-funded employer plans preempt Texas law and have stronger reimbursement rights.

- Subrogation liens are often reduced 30 to 50 percent through negotiation by an attorney.

You finally settled the claim from the wreck on I-35 near downtown Austin, and the offer looked like enough to cover your lost wages and out-of-pocket costs. Then a letter arrived from your health insurer demanding tens of thousands back from your check.

The settlement you were counting on suddenly feels a lot smaller than it did yesterday.

What Is Subrogation in a Motorcycle Claim?

Subrogation is the legal mechanism that lets your health plan recover what it paid for your accident-related care once you collect from a third party. It is not a penalty. It is a contractual right written into most policies and benefit plans, and it attaches to your settlement before the money reaches you.

Here is how this lien works in practice: Your insurer pays the hospital and doctors during treatment.

When you settle with the at-fault driver’s insurance, your plan asserts a claim against those proceeds. You will hear two terms used almost interchangeably: subrogation and reimbursement.

Subrogation technically lets the plan step into your legal shoes, while reimbursement operates as a lien on the proceeds. For a Texas motorcycle claim, the financial effect on you is the same.

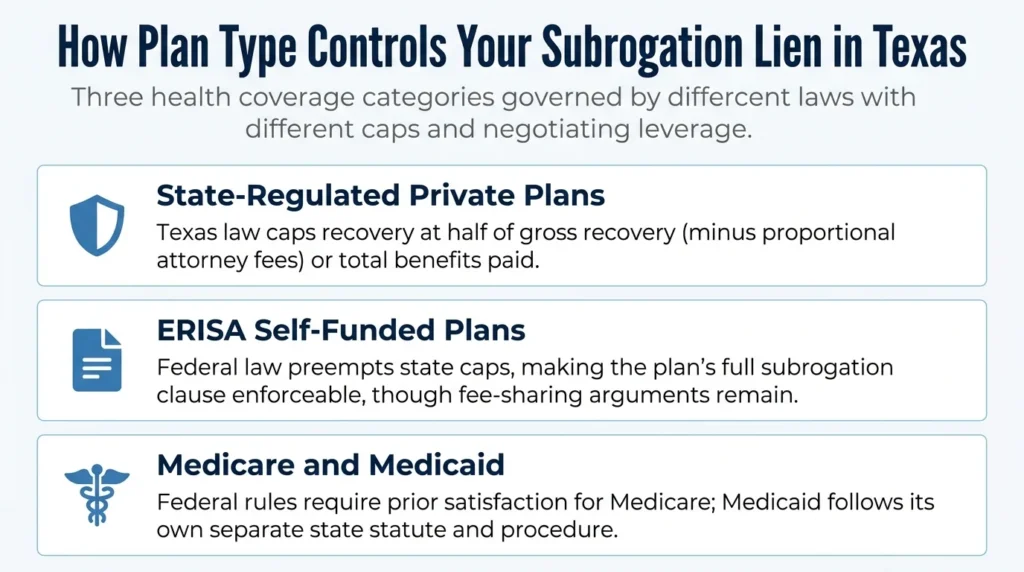

Three plan categories control how much room you have to push back: private health insurance, ERISA self-funded employer plans, and government programs like Medicare and Medicaid. The plan type drives everything.

Texas has a useful overview of how auto insurance subrogation rules work in similar contexts that mirrors much of the framework here.

Plan Type Determines Your Negotiating Leverage

Two riders with identical injuries and identical settlements can walk away with very different net checks based solely on what kind of health plan paid their bills. State-regulated private insurance comes with statutory caps and the “make whole” doctrine. ERISA self-funded employer plans answer to federal law and ignore those state protections. Knowing which one applies is step one.

Private Health Insurance Liens in Texas

Private health insurance bought on the individual market or through a fully-insured employer policy is governed by Texas state law. The Texas Civil Practice and Remedies Code (CPRC) Chapter 140 caps how much your plan can recover from your settlement. The cap is the lesser of one-half of your gross recovery minus a proportional share of attorney fees and costs, or the total benefits paid minus that same proportional fee share.

Run the numbers on a simple example. You settle for $100,000. Your attorney fees and costs come to $40,000, leaving $60,000 net. Your insurer paid $40,000 in medical bills and demands every dollar back.

Under Chapter 140, the cap is the lesser of half the net ($30,000) or the benefits paid net of attributable fees. The insurer cannot lawfully collect the full $40,000 it demanded.

Also under Chapter 140, the statutory make-whole doctrine does not apply — the insurer can recover its capped share even if the settlement does not fully compensate you for all losses. However, the cap formula itself limits the compensation, and an attorney can use the gap between the insurer’s demand and the statutory restriction as a negotiating opportunity.

Both protections only apply to state-regulated plans. ERISA self-funded plans prevent them.

ERISA Self-Funded Employer Plan Liens

ERISA-governed self-funded plans operate under federal law and ignore Texas’s Chapter 140 caps. The plan document controls, and if it includes a subrogation clause, federal courts enforce it under 29 U.S.C. § 1132’s equitable relief provision.

A quick way to tell if your plan is ERISA self-funded: your coverage comes through your employer, the employer is mid-to-large, and they self-insure rather than buying a commercial policy. Your Summary Plan Description (SPD) will spell out the subrogation or reimbursement section. Look for the words “self-funded” or “self-insured.”

The negotiating room is narrower with ERISA plans, but it is not zero. Some plans accept reduced recovery when the settlement is too small to make the claimant whole, especially when an attorney builds an argument from the plan’s own language. The common fund doctrine, which requires the plan to share in the legal fees that produced the compensation, is also a recognized basis for reduction.

A closer look at how motorcycle accident settlements work in Texas shows how these reductions factor into a final net number.

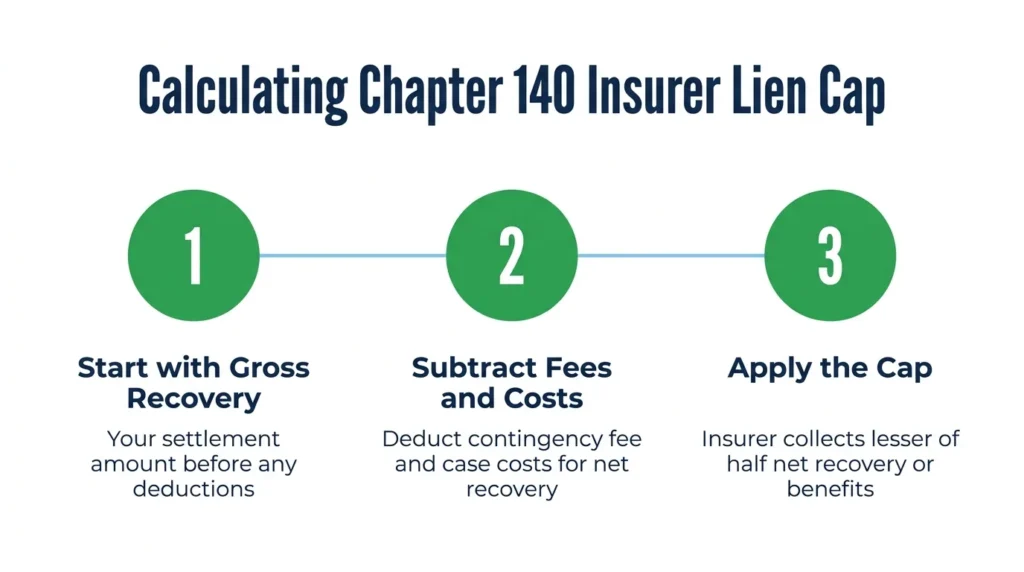

How Texas CP Chapter 140 Caps Private Plan Recovery

The Chapter 140 formula is mechanical once you know the steps. Start with gross compensation. Subtract attorney fees and costs to get the net recovery. The plan’s cap is the lesser of one-half of that net figure or the total benefits paid, minus a share of the fees and costs attributable to obtaining them.

Try a motorcycle-specific example. Say you suffer a tibia fracture and need emergency surgery. Bills total $80,000, all paid by your private health insurer. You settle at the $250,000 policy limit.

Your contingency fee is 33% ($82,500), and costs run $7,500, leaving a net recovery of $160,000. Half of that net is $80,000. Your insurer’s benefits paid, reduced by attributable fees and costs, lands around $53,000. The cap is the lesser figure: $53,000, not the $80,000 the insurer demanded out of the gate.

That formula creates leverage. Many insurers open negotiations with demands that exceed what Chapter 140 permits, counting on claimants who do not know the cap exists. Texas Civil Practice and Remedies Code Chapter 140 itself sets the procedural framework governing how state-regulated health benefit plans must calculate and assert reimbursement claims, to the extent ERISA does not preempt them.

If you are still sorting out who is on the hook for treatment costs in the first place, review who pays medical bills after a Texas accident.

Negotiating a Subrogation Lien on Your Settlement

Lien negotiation is a standard part of closing a personal injury case, not an add-on. An experienced attorney handles it as part of finalizing your settlement. The goal is simple: maximize the check you actually keep.

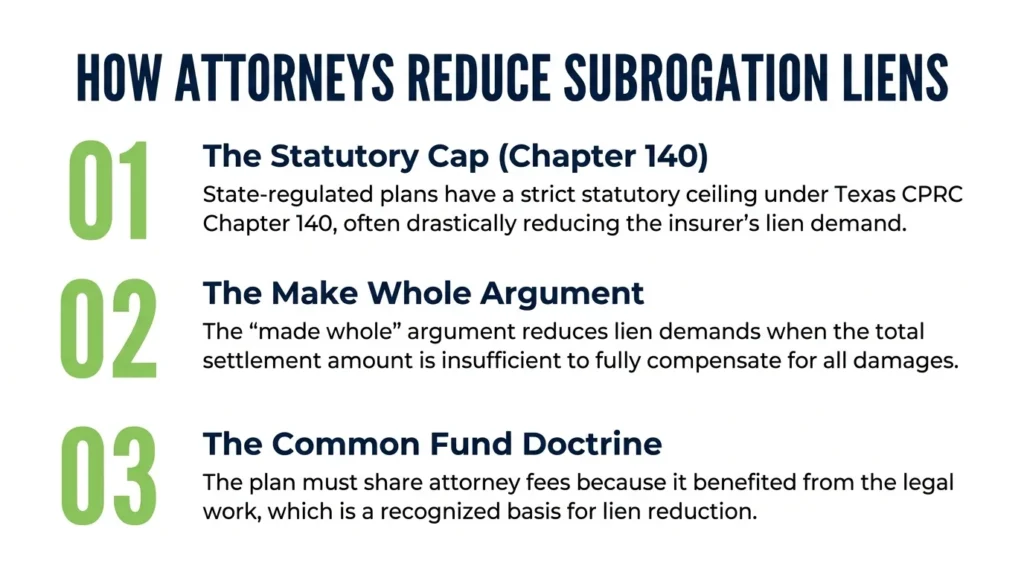

Three negotiation levers do most of the work:

- The statutory cap under Chapter 140 for state-regulated plans

- The make whole argument when the settlement does not cover all damages

- The common fund doctrine, which requires the plan to share the attorney fees that generated the recovery

Realistic outcomes? Liens are frequently reduced by 30 to 50 percent through negotiation. The reductions can increase when damages clearly exceed available policy limits and the make whole doctrine is squarely in play.

An attorney’s experience with how fees and lien resolution interact often determines how much of the settlement you keep, which is part of why understanding how attorney fees work in Texas injury cases is important before you sign anything.

Medicare and Medicaid liens are a separate track. Medicare’s Secondary Payer rules include federal recovery rights, and the Centers for Medicare and Medicaid Services must be notified and satisfied before distribution. Medicaid subrogation in Texas runs under state statute and requires its own handling.

One warning. Failing to resolve subrogation liens before distributing settlement proceeds can expose you and your attorney to direct recovery actions by the plan, or the extracting of assets. This plan can come after the money even after you spend it. Lien resolution is not optional.

Talk to an Experienced Attorney

Subrogation can shrink a settlement fast, and the gap between what your plan demands and what it can legally collect is often substantial. Angel Reyes & Associates has decades of experience representing injured riders across Texas and has recovered more than $1 billion recovered for clients in personal injury cases.

We work on contingency, which means no fee unless we win, and we handle lien negotiation as part of full-service motorcycle accident representation. Contact us today to talk through your case and what your net recovery could actually look like.

Past results do not guarantee future outcomes.

Motorcycle Accident Subrogation FAQs

Can a health insurer place a subrogation lien on a minor's motorcycle accident settlement in Texas?

Yes, but Texas courts scrutinize these liens more closely when the recovery belongs to a minor, and a court must approve the settlement before proceeds are distributed. The guardian or attorney is responsible for making sure any lien resolution serves the minor’s best interests before the judge signs off.

Does Texas law give a workers' compensation carrier subrogation rights if I was injured while riding a motorcycle for work?

Yes. Under Texas Labor Code Section 417.001, a workers’ compensation carrier that paid benefits for a work-related motorcycle accident has a subrogation right against any third-party recovery you obtain. The carrier’s lien is calculated differently from a health insurance lien and is governed by the Labor Code rather than CPRC Chapter 140.

What happens to a subrogation lien if the at-fault driver had no insurance or too little coverage to fully pay my damages?

The answer depends on your plan type. For state-regulated private health plans, a severely limited recovery strengthens any negotiation because the insurer’s demand may consume most of what you received. ERISA plans are less flexible, but some administrators still accept a reduced amount when the documented shortfall is clear and the attorney presents the math in writing.

If I reject a settlement offer and go to trial, does the subrogation lien stay in place?

Yes. The lien does not disappear simply because the case goes to trial. If you win a jury verdict, the plan will assert its reimbursement claim against the judgment proceeds using the same rules that would have applied to a settlement.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 70,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...