How Motorcycle Accident Settlement Negotiations Work

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- A demand letter opens negotiations by stating your damages and proving the other driver's fault.

- Texas gives you two years from the motorcycle crash to file a personal injury lawsuit.

- A rider found 51% or more at fault recovers nothing under Texas comparative negligence law.

You were riding home through Deep Ellum one evening when a driver turned left across your lane and clipped your front wheel near Commerce Street. The crash was not your fault, and the police report says as much.

Now the bills are stacking up, you are missing work, and the other driver’s insurer keeps sending you offers that would not cover your first surgery. How does this back-and-forth actually end?

Starting Negotiations with a Demand Letter

Settlement negotiations formally begin when you send the insurer a demand letter. This document states your claimed damages, lays out the evidence proving the other driver caused the crash, and names the dollar amount you want.

The demand letter sets the tone for everything that follows. A weak letter invites a low offer. A detailed one signals that you came prepared.

A strong demand letter rests on the records that prove what happened to you and what it cost. Gather these before you send it.

- Medical records and bills: Every diagnosis, treatment note, and invoice tied to your injuries

- Lost wage documentation: Pay stubs, employer letters, or tax records showing the income you missed

- Crash scene and injury photos: Images of the wreck, your bike, the road, and your physical injuries

- The police report: The official account of how the collision happened and who was at fault

- A clear liability narrative: A written summary connecting the evidence to the other driver’s fault

You will usually set the demand above your lowest acceptable number. That leaves room to negotiate down while still landing where you need to be. The letter should also point to the Texas law and the specific facts that justify the figure you are asking for.

Timing is just as important as content. Most riders send the demand after treatment ends or after they reach maximum medical improvement, the point where a doctor says recovery has plateaued. Sending too early risks leaving future medical costs out of your number.

If you want the broader picture of how these claims resolve, our overview of how motorcycle accident settlements work in Texas walks through the full arc. For the mechanics of the letter itself, our breakdown of what a demand letter does covers the structure in detail.

Insurer Response Timelines & Tactics

Texas law gives motorcycle riders leverage when an insurer drags its feet. Under the Texas Insurance Code Chapter 541, insurers are prohibited from failing to make a good-faith attempt to settle a claim when fault is reasonably clear.

If you carry uninsured/underinsured motorist, PIP, or MedPay coverage and are making a claim under your own policy, Chapter 542 also imposes strict deadlines:

- Your insurer must acknowledge your claim within 15 days

- They must accept or deny it within 15 business days of receiving all documentation (extendable to 45 days with written notice)

- They must pay an accepted claim within 5 business days

Violations of those first-party deadlines trigger 18% annual interest plus attorney fees. For the third-party liability claim against the at-fault driver’s insurer, Chapter 541’s unfair-practices prohibition remains your primary statutory lever, along with your right to sue if the insurer acts in bad faith.

Adjusters still have a playbook, and motorcycle riders see the sharpest version of it. The insurer’s job is to close your claim for as little as possible. That is how the business works.

Expect an early lowball offer timed to your financial stress. Expect requests for a recorded statement that can be used against you later. Expect the adjuster to lean on old assumptions about riders to argue you share the blame.

The first answer is almost always a denial or a thin offer. That is the opening move in the counter-offer cycle, not the insurer’s last word. If your first offer feels unfair, it can help to understand your rights before you respond.

Counter-Offer Cycles & What Moves an Insurer

The counter-offer cycle is the back-and-forth where you answer the insurer’s offer with documentation or argument supporting a higher number. Multiple rounds are normal. Each exchange should narrow the gap between you.

Certain things genuinely move an adjuster to raise an offer. Clear, uncontested liability pushes the number up. So does strong medical proof of your injuries and visible evidence of economic harm like lost wages or long-term care costs. Attorney involvement signals you are ready to litigate, which the insurer factors in.

The insurer’s main tool for cutting your offer is fault. Under the Texas Civil Practice and Remedies Code (CPRC) Chapter 33, a rider found 51% or more at fault recovers nothing. Below that line, your recovery drops by your share of the blame.

This fault-sharing rule is why insurers fight so hard to pin part of the crash on you. If they can argue you were 30% responsible, they cut nearly a third off what they owe. Our explanation of the Texas 51% comparative negligence rule shows exactly how that math works against you.

Motorcycle cases draw heavier fault arguments than most. Insurers reach for rider speed, gear choices, lane position, or claims that you were hard to see. Countering each one with evidence protects the offer on the table.

Before you say yes to any number, understand what you give up by accepting. Straightforward cases may settle in weeks. Disputed liability or serious injuries can stretch the cycle across months before a workable number appears.

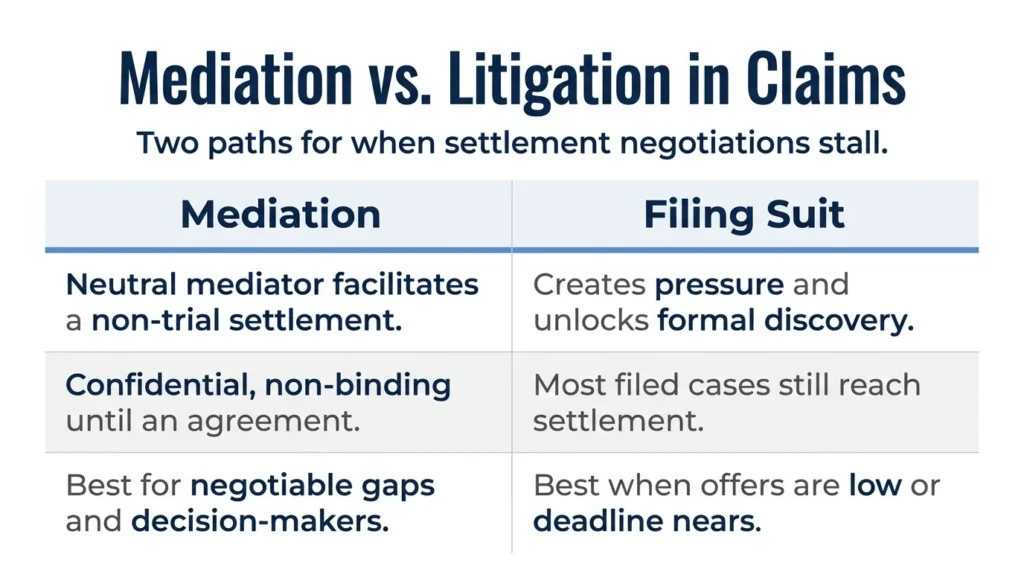

When Mediation or Litigation Is the Stronger Path

When direct negotiations stall, you have two main ways to escalate. Mediation brings in a neutral third party to broker a deal. Filing suit applies litigation pressure and opens the door to discovery.

Mediation in Texas Motorcycle Cases

Mediation is a process where a neutral third party helps both sides find a settlement. It is sometimes voluntary and sometimes ordered by the court. Many Texas courts order mediation before trial in injury cases, and some counties make it routine through local rules and standing orders. Chapter 154 of the Texas Civil Practice and Remedies Code authorizes courts to refer pending disputes to mediation on their own motion or a party’s request.

You typically reach mediation after direct talks stall, either before a lawsuit or after filing but before trial. The session stays confidential. Nothing binds you unless both sides sign an agreement.

Each side presents its position, and the mediator shuttles between rooms to find a range everyone can live with. A written settlement agreement signed by both parties and their counsel at the close of mediation is binding and enforceable as a contract under Texas law. Mediation often pulls the insurer’s actual decision-makers into the room, and that frequently produces offers an adjuster never would.

Filing Suit as a Negotiating Signal

Filing a lawsuit does not mean your case is headed to trial. Most filed cases still settle. What filing does is create pressure and unlock discovery, which often surfaces evidence that strengthens your position.

Several signals point toward filing as the better move. The insurer’s final offer sits far below your documented damages. It keeps pressing fault arguments the evidence does not support. Prompt payment deadlines have slipped without a real explanation, or the filing deadline is closing in.

That filing deadline is fixed. The Texas Civil Practice and Remedies Code section 16.003 gives you two years from the crash to file a personal injury suit. Miss it, and your right to recover is gone for good, which makes watching the calendar part of every negotiation strategy.

Discovery is where filing earns its keep. It can pull adjuster notes, internal valuation records, and communications that show how the insurer landed on its offer. That paper trail often hands you leverage you did not have before. If talks have stalled or your deadline is near, it helps to understand what litigation actually involves and how motorcycle claims move through the process.

Work with an Accident Attorney

Angel Reyes & Associates has stood with injured Texas riders for more than 30 years, and we know how insurers approach motorcycle claims. We work on contingency, so you pay no fee unless we win, and your first consultation is free.

We have more than $1 billion recovered for clients across Texas. If you are facing a lowball offer, stalled talks, or a deadline closing in, reach out for a free consultation.

Past results do not guarantee future outcomes.

Settlement Negotiation FAQs

How long does a motorcycle accident settlement typically take in Texas?

Simple cases with clear fault and minor injuries can settle in a few months, while cases involving serious injuries, disputed liability, or litigation often take one to two years or longer to resolve.

Does signing a settlement release end your right to seek more money later?

Yes. When you accept a settlement, you sign a release that permanently closes your claim, even if your injuries turn out to be worse than expected. That is why waiting until you have reached maximum medical improvement before accepting a number is so important.

Is a motorcycle accident settlement considered taxable income?

Compensation for physical injuries and related medical bills is generally not taxable under federal law, but punitive damages and any interest included in the settlement are taxable. Texas has no state income tax, so only the federal rules apply here.

What happens to your claim if the at-fault driver had no insurance?

If you carry uninsured or underinsured motorist coverage on your own motorcycle policy, you can file a claim with your own insurer and negotiate a settlement through that coverage. Without that coverage, your options narrow to pursuing a lawsuit directly against the uninsured driver, who may not have assets to pay a judgment.

Can you file a separate bad-faith lawsuit if the insurer knowingly violated Texas insurance law?

Under Texas Insurance Code Chapter 541, a claimant who proves the insurer knowingly committed an unfair practice can recover up to three times their actual damages, plus attorney fees. This remedy is separate from the Chapter 542 interest penalties and applies only when the violation was knowing, not merely negligent.

About the Authors

Alex Ivanov

Writer

Alex Ivanov is a personal injury attorney at Angel Reyes & Associates, focused on car, truck, and motorcycle accident cases. Licensed in Texas and multiple federal districts, Alex brings international legal experience and a global education to his practice. He earned his LL.M. from Texas A&M University School of Law after graduating from Belarussian State University in 2016. Alex is fluent in Russian, English, Ukrainian, and Belarussian, and is recognized by multiple national trial lawyer associations for his results and leadership under 40.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Kyle Nicolas

Reviewer

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...